Memphis Rental Property #14

Last updated: 2026

NOTE: This article was published in 2026, but I bought the house seven years before in 2019. In the Annual Updates at the bottom, you can see how the property has performed over the years.

Say hello to Property #14 in my Memphis rental portfolio! In case you missed it: this was one of the 14 I houses I purchased very quickly from May to September of 2019 — my opening acquisition sprint after I left my “first career” in retail, sold my NYC condo to become a renter, and used the proceeds to start building a portfolio that would generate real cash.

Originally built in 1977, this 4-bed, 2.5-bath house is one of the largest in my portfolio at 2,255 square feet. It’s in a great B neighborhood in the 38141 zip code, and I got a very solid deal on the house at the point of purchase. But like Property #6, the size of the house has in some ways defined my experience with it so far, and illustrates the risks of larger homes as rental properties.

Alright, let’s take a closer look at this house and deal!

Property #14: The Deal

This was another publicly-listed house that I found on MLS/Zillow. Despite all the attention devoted to creative deal-sourcing, the boring, straight-forward approach to deal sourcing is really all you need as a long-term buy and hold investor.

The house was listed at $119,900, and had a long-term tenant in place paying $1,230/month. My initial offer of $115K was accepted, but the deal required a LOT of back-and-forth to get to the finish line — more on that below.

Here are some additional facts about this particular house:

4-beds, 2.5 bath

In the 38141 zip code, solid B neighborhood

Built in 1977

2,255 square feet of interior space on two levels

Central air

Home occupied and in mediocre condition

Driveway with built-in garage

Property #14: Due Diligence

There were many twists and turns during due diligence on this deal, and it took over three months from contract to closing.

I learned from the seller that the roof and HVAC were only 2 years old — but that was the end of the good news. The inspection revealed that the house was in pretty poor condition and would require a significant rehab once the tenant eventually vacated. There were also some concerning callout about the electrical systems.

But most troublingly, it showed that the tenant was a hoarder. This wasn’t the truly awful kind of stuff you see on the Hoarders TV show, but it was still very bad, and I was quite concerned about the damage to the property from the hoarding, the amount of work that would be required to actually empty the house if/when the tenant vacated, and the potential costs associated with having to evict a tenant from a hoarder house.

But the seller was very keen to get the deal done, for obvious reasons. So I took a tough negotiating stance that resulted in the seller making $6K of electrical repairs, while also reducing the price to $105K. The numbers were good enough that I felt comfortable taking the risk on the house, with the understanding that it would likely turn into a significant appreciation and cash flow play once I got the house fixed up.

These are some photos pulled from the appraisal report at the time I bought the house — not a stunner at the time, obviously!

Property #14: The Financials

At this stage of my investing journey, I had used up all my “golden tickets” so I no longer had access to conventional mortgages. I moved on to the next-best option, which were nonconforming rental loans — now usually called DSCR loans. It was still a 30-year fixed rate loan, but rates and terms were not quite as attractive, so my interest rate on this loan was 6.35%. I put down a 25% down payment.

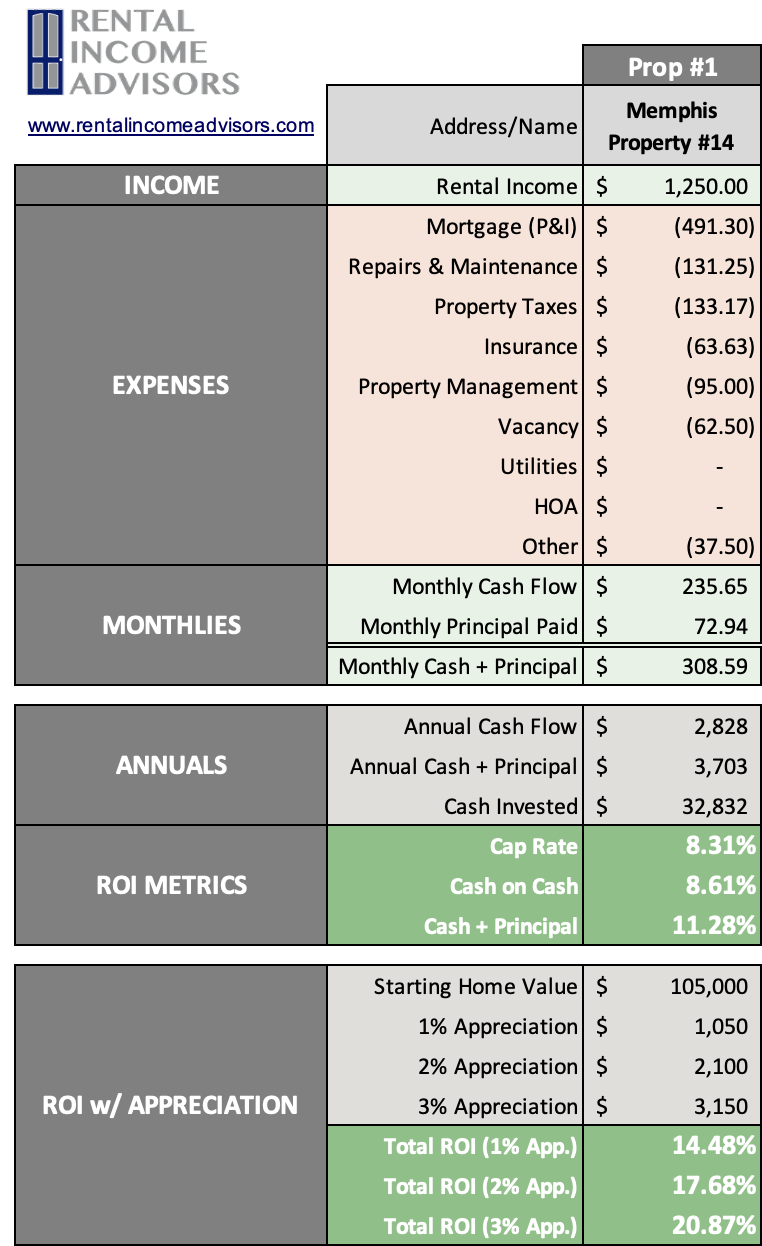

As I mentioned earlier, the inherited tenant was paying $1,250. Using the RIA Property Analyzer, I’ve modeled the original figures from this deal, so you can see what it would have looked like at the time:

Purchase Price: $105,000

Monthly Rent: $1,250

Monthly Cash Flow: $235

Cap Rate: 8.3%

Cash on Cash Returns: 8.6%

Total ROI 2% Appreciation: 17.7%

(Want to use this calculator? It’s free!)

OR

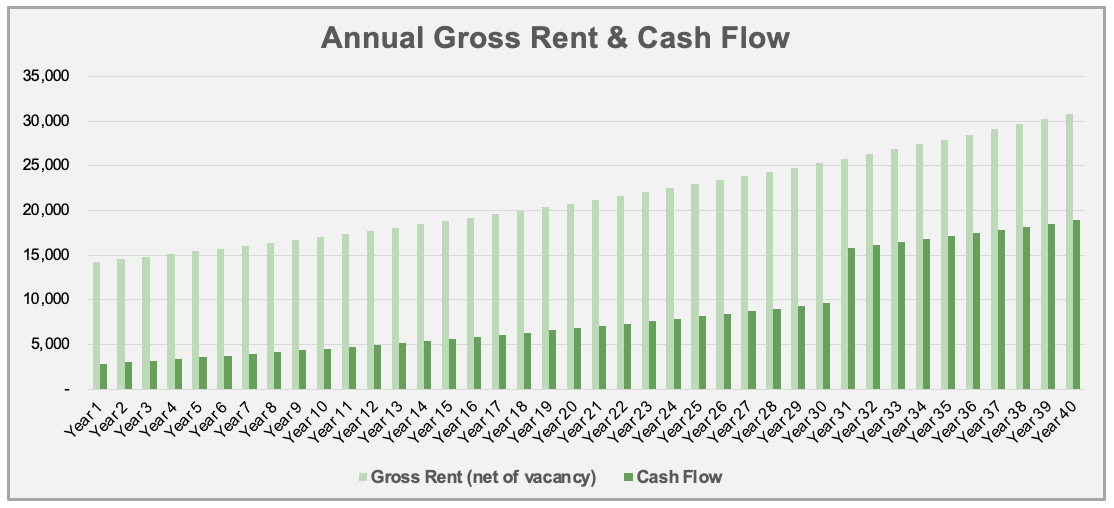

Using the multi-year model in the RIA Property Analyzer, we can visualize some of the main long-term trends assuming a long-term inflation rate of 2%:

Cash flow increases over time. This is mostly because rent and expenses are expected to rise with inflation, but one major expense (my mortgage) is fixed.

Cash Flow Year 1: $2,828

Cash Flow Year 10: $4,530

Cash Flow Year 25: $8,136

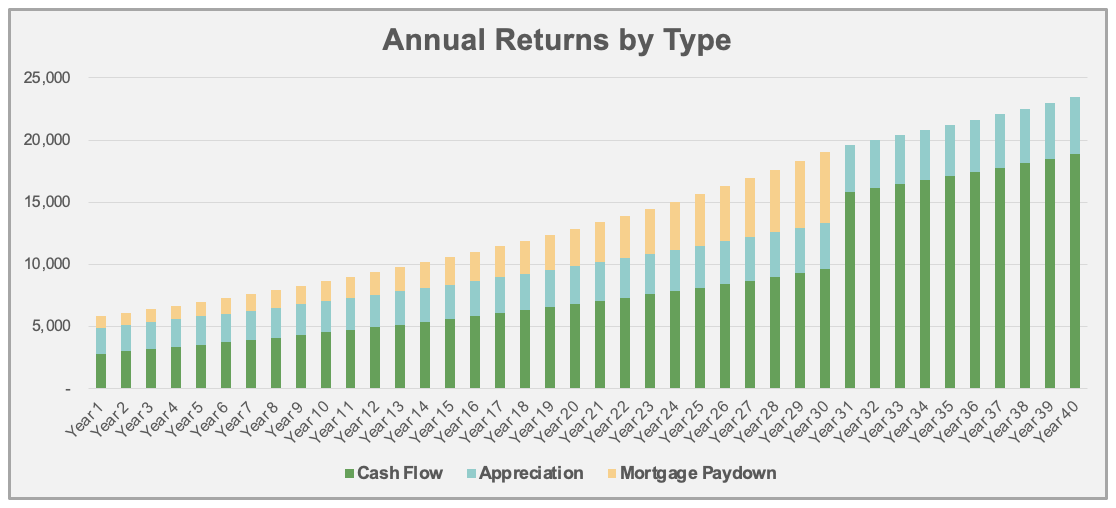

Mortgage paydown accelerates over time. This is because of the way banks amortize loans – each month, a little bit more of your fixed payment is principal, and a little bit less is interest.

Mortgage Paydown Year 1: $901

Mortgage Paydown Year 10: $1,597

Mortgage Paydown Year 25: $4,145

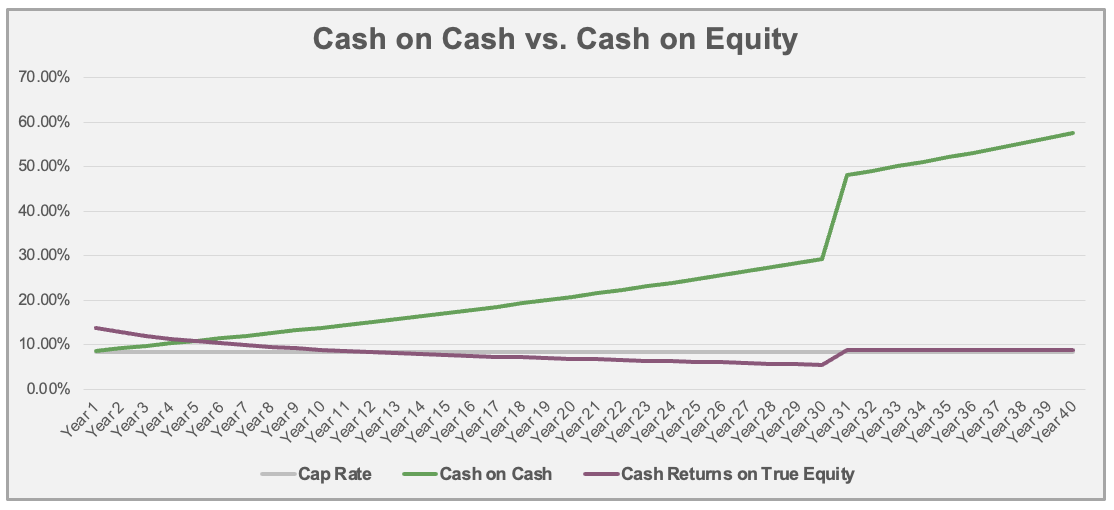

Total returns on cash increases over time. This is a consequence of the first two graphs – I will make greater total returns over time on the same initial investment of cash.

Total Returns on Cash Year 1: 17.8%

Total Returns on Cash Year 10: 26.3%

Total Returns on Cash Year 25: 47.7%

This house was pretty unusual for me. First of all, it was in pretty bad condition, with a questionable tenant in place. Also, it was overly large. Putting those things together, I was taking a bit more risk with this acquisition, and taking on future liabilities. Check out the Annual Updates below to get a sense of how that gamble has turned out so far.

Property #14: The Deal Sheet

Finally, to sum up Property #14 and its financials, here’s the full “deal sheet”:

Looking for YOUR Next Property?

If you need help finding, analyzing, and purchasing YOUR next property — or your first one! — schedule a free initial consultation with me. I’ve helped over 120 private coaching clients invest with confidence and build cash-flowing rental portfolios of their own.

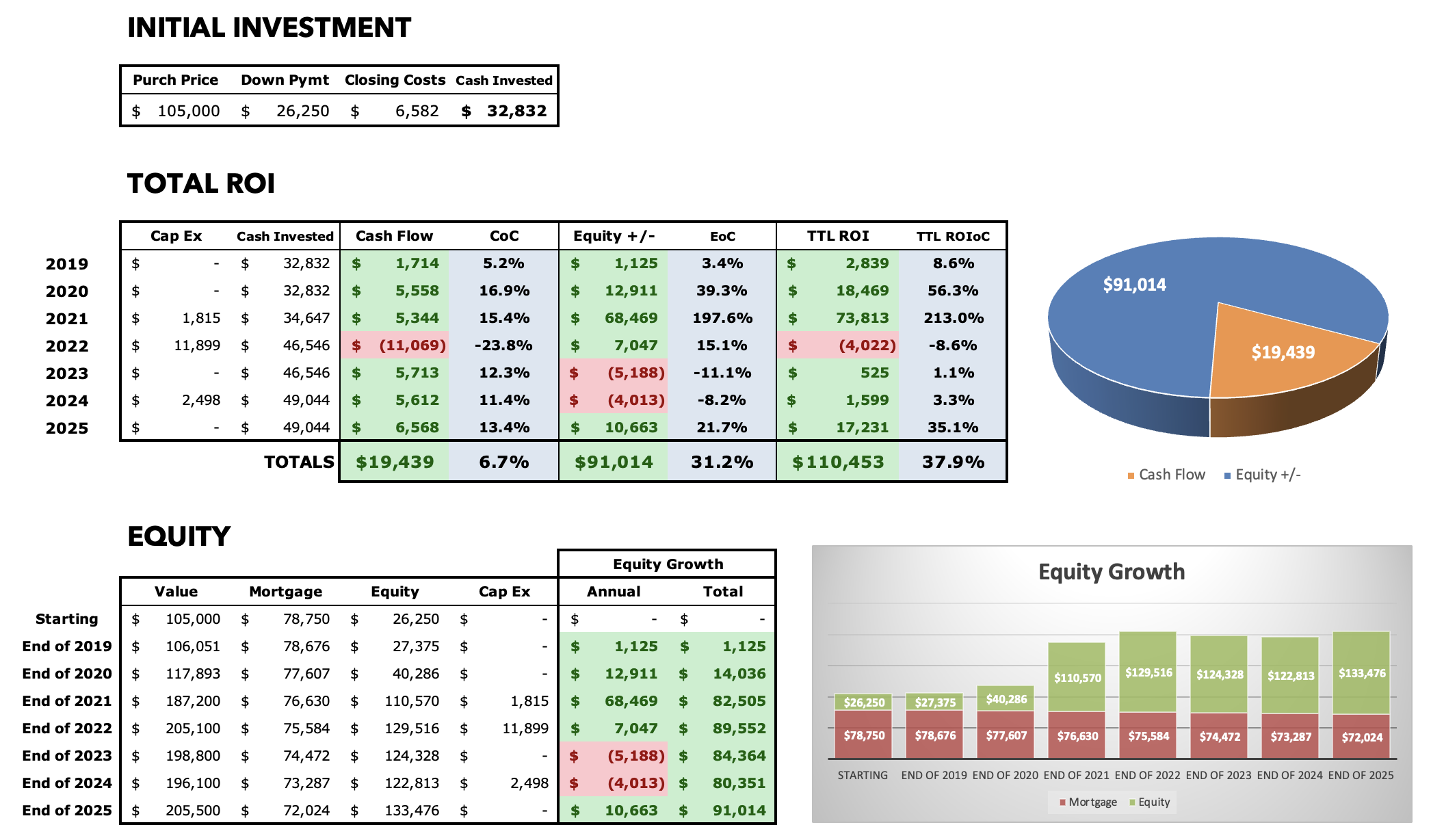

Annual Updates

For all Property Spotlights, I come back at the end of each year to provide a brief narrative of what happened at the property that year. I also update my annual and cumulative figures for the property, including cash flow, equity growth, and occupancy.

2019

Everything went smoothly after closing in September, and I managed a positive cash flow of $1.7K for the year (not always easy in the Year 1.)

2020

Two HVAC visits in May and June totaled ~$600, but there were no other maintenance costs for the year. When it came time for lease renewal, I made the choice to keep the tenant on a $1,275 month-to-month arrangement to allow myself more flexibility given the concerns about their hoarding. Cash flow for the year was over $5.5K.

2021

Maintenance costs were again quite low, under $500 for the year. I did have $1.8K in CapEx to replace the furnace. The tenant remained in place at $1,275 on a month-to-month lease. Cash flow for the year was similar to 2020, coming in at $5.3K.

This was also the year that most of this house’s pandemic-era price gains registered, jumping from a valuation of $117K to $187K.

2022

The tenant submitted notice that they would vacate at the end of May, so the time had come to get this house up to standard. As expected, it was costly to do so: over $8K in pure expense for interior paint and various cosmetic upgrades, and another $8K for CapEx items (mostly new LVP flooring throughout much of the home, which was previously carpeted). The house was nicely transformed, and we were able to rent it pretty quickly at the much higher rate of $1.695/mo. The new tenant moved in at the end of August.

The new tenants, though, were quite particular about things. They called in to my PM constantly with minor issues, some of which they should have been able to fix/handle on their own. This caused maintenance expenses to pile up a bit after they moved in, and I also had a $2K roof repair and a full HVAC replacement ($3.7K of additional CapEx).

Needless to say, it was a sea of red ink for the year, with negative cash flow of $11K. The good news is that I’ll have much more rent coming in going forward — and home values ticked up again.

2023

The tenant indicated mid-year that they would vacate when their lease was up, citing rent costs. I hated the idea of a 1-year tenancy after such a big turn the previous year, so I asked my PM to see if there was any way to get the tenants to stay. Ultimately, they signed a renewal at $1,550 per month, or $150/mo. less than they were previously paying. They were tough negotiators, and wanted more, but I finally told them they could take the $1,550 offer or vacate, and they took it. Though this means a reduction in the property’s income, it’s still a much better outcome for me than a vacancy — and hopefully better for the tenant at the same time vs. having to move.

Meanwhile, maintenance costs were over $3K for the year, including the removal of the tree in the front yard which had been damaged by a storm. Cash flow for the year was $5.7K.

2024

We decided to offer the tenant another year with no increase to the rent, so they renewed again at $1,550. The tenant has fallen into a pattern of paying late every single month, but they pay it pretty reliably around the 15th of the month. But this means that they pay a 10% late fee every month, which negates the value of the rent deal I gave them in 2023.

Maintenance was $2.4K for the year, including a small roof repair. I also spend $2.5K of CapEx to completely replace the garage door and motor. Cash flow as similar to the previous year, coming in at $5.6K. Home prices have been stable for the last few years.

2025

Come September, the tenant renewed for another year, but this time with an increase to $1,600/mo. (Still $100 below their original rent in 2022.) They still pay late every single month.

Maintenance costs were $2.1K, most of which was from another (unrelated) roof repair. It seems likely the a full roof replacement will be needed at this house pretty soon. Cash flow set a record at $6.5K.

About the Author

Hi, I’m Eric! I used cash-flowing rental properties to leave my corporate career at age 39. I started Rental Income Advisors in 2020 to help other people achieve their own goals through real estate investing.

My blog focuses on learning & education for new investors, and I make numerous tools & resources available for free, including my industry-leading Rental Property Analyzer.

I have also served as a coach to over 100 private clients starting their own journeys investing in rental properties, and have helped my clients buy millions of dollars (and counting) in real estate. To chat with me about coaching, schedule a free initial consultation.

Property #14 in my Memphis rental portfolio is an large 4/2.5 in a solid B neighborhood. I got a great deal on it, but it was a mess, so it’s been a journey to get it cleaned up over the years.