Memphis Rental Property #23

Last updated: 2026

NOTE: All figures and statements in this article were accurate as of the time of initial publication in 2022. Check out the Annual Updates section at the bottom of the post to see how the property has performed since then.

In December 2022, I closed on four (!) new properties in Memphis. This was directly on the heels of Property #20, which closed a month prior. This house, Property #23, is the third of those December closings, and the last property (out of four) that was part of the 1031 exchange I did when I sold my last remaining NYC rental condo this past summer. In a future blog post, I’ll look at the 1031 exchange in total, and discuss both the process and the financials & associated tax savings.

This one is very similar to Property #21 in many respects. It’s a 3 bed/1 bath house that I acquired through a turnkey provider. It’s in the Raleigh area, which is one of my favorite rental neighborhoods in Memphis, and the same zip code as my first Memphis property.

I acquired this with a conventional mortgage — but sadly, that will be my last such loan. I’ve officially come to the end of my “golden tickets”, which means that I’ll have to get a bit more creative with all future loans. Probably I’ll just rely on nonconforming/asset-based loans, which have no limit but generally have less favorable rates and terms than conventional mortgages do. (For a longer discussion on financing strategies and why conventional loans are the best first option for rental investors, check out my article 8 Ways to Finance Rental Properties.)

Ok, let’s get into the details of this deal!

Property #23: The Deal

This house was bought from a turnkey provider, so it was sold directly through that provider’s sales channel. It’s a very typical home for this B/B- neighborhood: a 3 bed/1 bath house containing 1080 square feet, with brick construction and a carport, originally built in 1964.

Because this was a turnkey property, I knew that everything would be newly rehabbed: new roof, new mechanicals (HVAC, furnace, and water heater), new or refreshed kitchen & bathroom, new flooring and paint, etc. Even as an experienced investor, I appreciate the ease & simplicity of buying turnkey properties, especially when I already know and trust the provider based on previous purchases. In fact, I worked directly with this turnkey provider during the 1031 exchange, to make it easier to find and close on multiple properties in the prescribed timeframe without any surprises or headaches.

The original purchase price was $135,000, with an expected rent of $1250. However, when the turnkey provider lowered the rent expectation to $1175, I asked for a reduction in the purchase price, and we agreed on $129,900. This isn’t the juiciest price-to-rent ratio, falling well short of the “1% rule”, but that’s typical for turnkey properties where you pay a premium to have all the work done for you ahead of time.

Inside, the house looks very much like my previous turnkey properties (Property #17 and Property #21 are examples). Take a look:

I closed on the property without delays, using the last of my funds from my 1031 exchange for the down payment. But that’s when we rant into some problems finding a tenant.

The property wasn’t getting a lot of bites at $1175, so we were forced to lower the asking price to $1095, which meant my ROI numbers took a hit. Even then, it sat vacant for quite a while as my PM searched for a qualified resident. Ultimately my PM agreed to fund a “first month free” sweetener, and that finally did the trick. The new tenant moved in about two months after I closed on the house.

I’m still not sure why it was difficult to rent this house — normally, turnkey properties fly off the shelves because tenants are attracted to the newly rehabbed home and the bright clean finishes. Was it just bad timing coinciding with a wintertime lull in the rental market? Was it something specific about the home that tenants didn’t like? I truly don’t know, but I accept that there is a bit of randomness and luck to this; the only other previous time I’ve had trouble renting a house, that same house rented very easily (at a higher price) a few years later. I hope that will be the case with this one too.

Since there was no due diligence or rehab on this property, let’s jump right into the numbers.

Property #23: The Financials

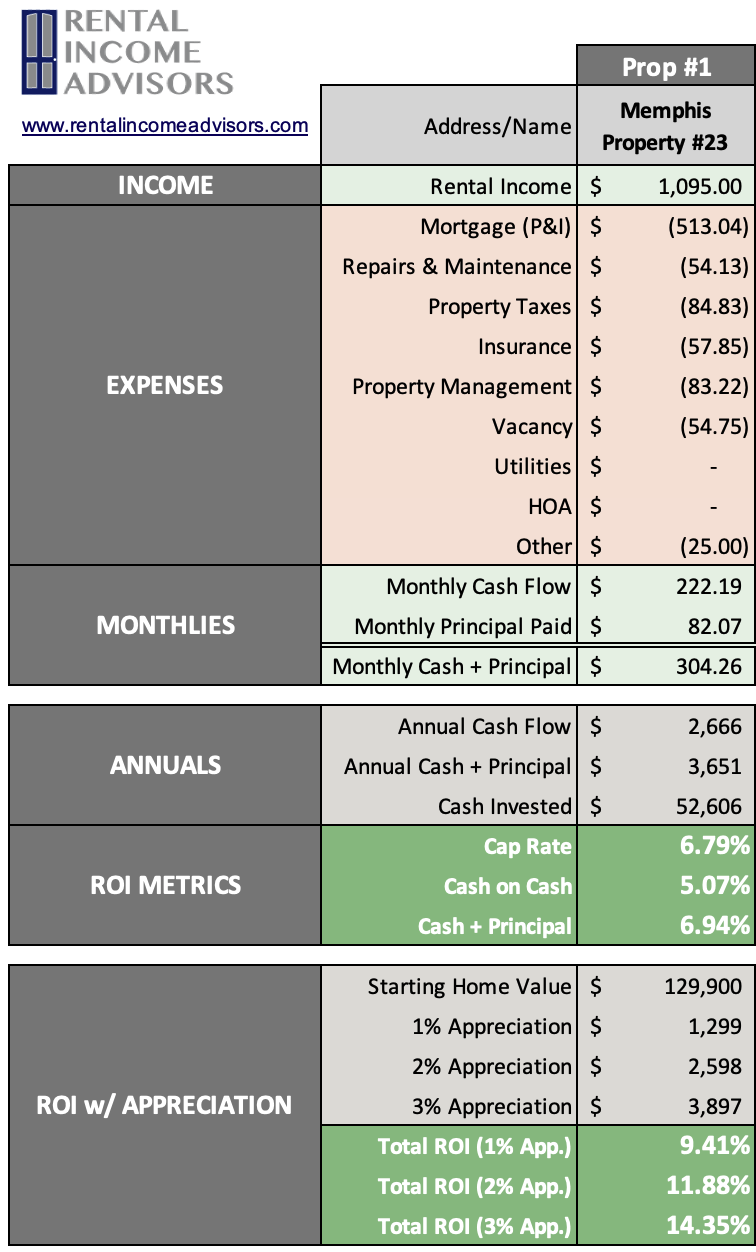

I financed 70% of this purchase with a conventional loan at 6.125%. (I used a slightly larger down payment here than normal because of the specific financials around the 1031 exchange.) So my down payment was $38,970, and I incurred $7,141 in closing costs including buying down the interest rate a bit with points. I used the RIA Property Analyzer to run the final numbers on this property – here are the key metrics that the analyzer calculated for me:

Purchase Price: $129,900

Monthly Rent: $1,095

Monthly Cash Flow: $222

Cap Rate: 6.79%

Cash on Cash Returns: 5.07%

Total Returns w/ 2% Appreciation: 11.88%

(Want to use this calculator yourself? You can!)

OR

While I still like this property and neighborhood a lot, I’m a bit disappointed in the final numbers, and in how long it took to find a tenant. These are likely short-term pain points, though — I’m hopeful that the property will nonetheless become a solid cash flow investment over time. As with all my Property Spotlights, I’ll update the annual numbers each year at the bottom of this post, so we can track the results over time.

Using the multi-year model in the RIA Property Analyzer, we can visualize some of the main long-term trends (assuming an inflation rate of 2%):

Cash flow increases over time. This is because rent and expenses are expected to rise with inflation, but one major expense (my mortgage) is fixed.

Cash Flow Year 1: $2,666

Cash Flow Year 10: $4,388

Cash Flow Year 25: $8,034

Mortgage paydown accelerates over time. This is because of the way banks amortize loans – each month, a little bit more of your fixed payment is principal, and a little bit less is interest.

Mortgage Paydown Year 1: $1,013

Mortgage Paydown Year 10: $1,755

Mortgage Paydown Year 25: $4,389

Total returns on cash increases over time. This is a consequence of the first two points – I will make greater total returns over time on the same initial investment of cash.

Total Returns on Cash Year 1: 11.9%

Total Returns on Cash Year 10: 17.6%

Total Returns on Cash Year 25: 31.6%

Overall, I’m satisfied with this purchase. And it does look and feel a lot like Property #21, in that neither of there were a “home run” when it comes to cash flow or ROI numbers, but both of them are solid homes is strong rental neighborhoods that are likely to be slow & steady winners over the long term.

This house adds another $200+/month in average cash flow — not a HUGE number, but it nonetheless meets the goal of my 1031 exchange: to get out of my NYC condos (that actually lost a few hundred per month on average), and trade them in for properties that have positive cash flow. Mission accomplished here — in fact, across all four of my 1031 exchange purchases, I should now generate over $1,200/month in net cash flow, which will grow to nearly $1,500/month once I’m able to stabilize Property #22 at market rent.

Property #23: The Deal Sheet

Finally, to sum up Property #23 and its financials, here’s the full “deal sheet”:

Looking for YOUR Next Property?

If you need help finding, analyzing, and purchasing YOUR next property — or your first one! — schedule a free initial consultation with me. I’ve helped dozens of private coaching clients invest with confidence and build cash-flowing rental portfolios of their own.

Annual Updates

For all Property Spotlights, I come back at the end of each year to provide a brief narrative of what happened at the property that year. I also update my annual and cumulative figures for the property, including cash flow, equity growth, and occupancy.

2023

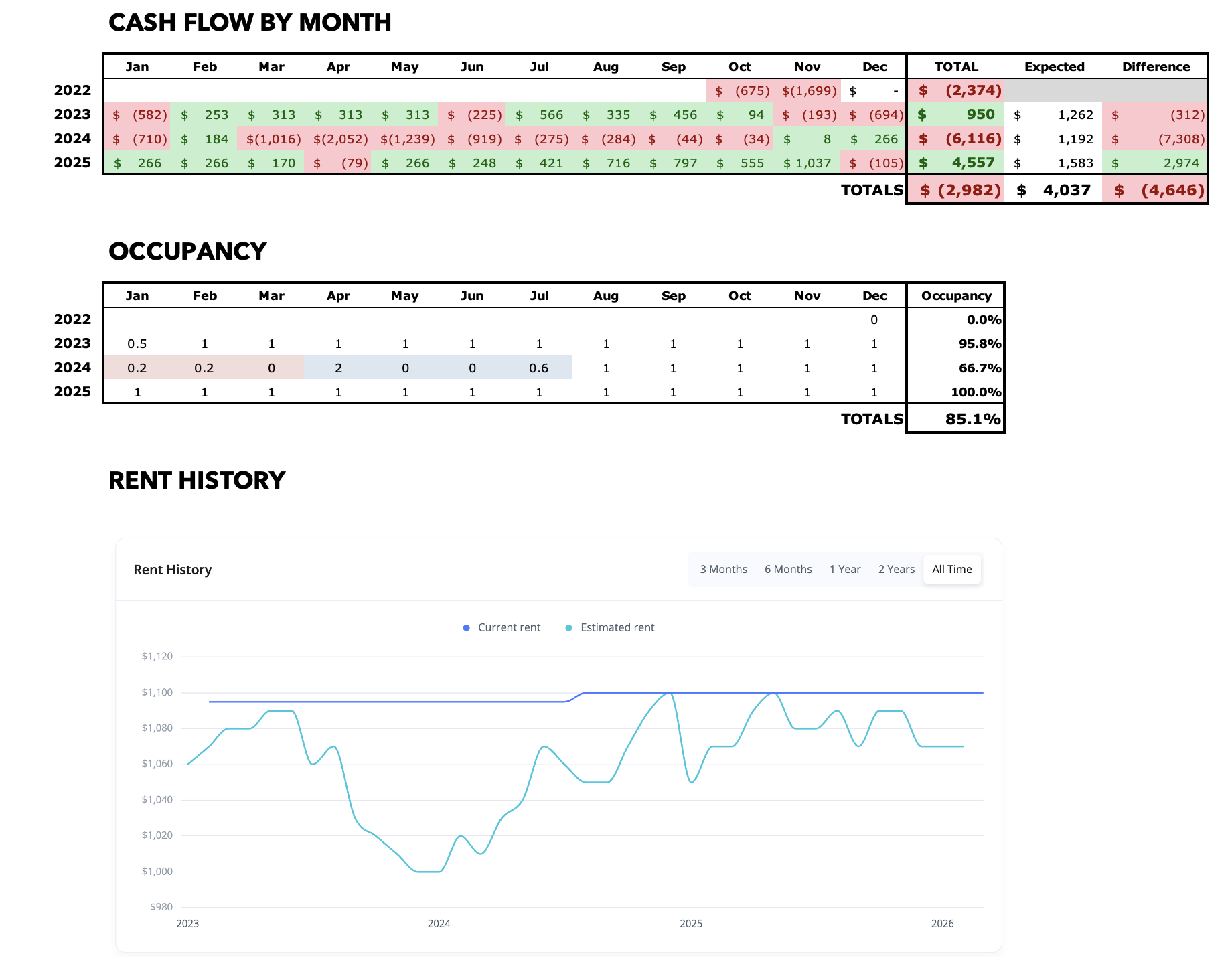

After a bit of a rocky start getting the property rented, things stayed wobbly all year long. First, I had a series of maintenance issues with the heating and cooling systems, something I shouldn’t have to deal with in a turnkey property. My PM covered some of the costs of those repairs, but I recently discovered that the furnace appears to be 15 years old, when it was supposed to be new. Still working on a resolution to that.

Meanwhile, the tenant my PM placed struggled to pay the rent from the get-go. They were consistently late, and made small partial payments throughout the month — signs of someone struggling to make ends meet. Finally, in December, the situation reached a point where we had to start the eviction process. So we’ll see how that shakes out. This is a situation where I may ask for further accommodations from my PM, because they have failed so far at nearly every step of the process with this turnkey.

Also, the value of the property (at least according to Zillow) fell significantly this year — but that seems to just be an anomaly.

Despite all that, I still managed a small positive cash flow. But with an eviction on the horizon, 2024 may be a down year.

2024

The dark clouds on the horizon at the end of 2023 produced a lot of rain in 2024. In the end, the tenant was evicted, and a new tenant was not placed until July. For a second time, it wasn’t the easiest property to rent, and the rent we achieved ($1,100/mo.) was the same as before.

The turn scope wasn’t large, thankfully. But even since then, I’ve had more maintenance costs than I would hope for a turnkey property, including three different electrical issues this fall amounting to about $1K in cost. Given all the problems, I did ask my PM for an accommodation, but only received a very small one.

The Zestimate did not recover, so it’s looking like (even with the $5K reduction I got in the original deal), I may have overpaid for this house. In the long run, though, this should become less and less important as my gains accrue over time. This one is not a banger so far, though, obviously.

2025

This property finally achieved a measure of stability this year. My tenant pays the rent on time, and is the middle of their 2-year lease, so I was fully occupied for the year.

I had just $800 in routine maintenance costs. And as a bonus, I received back-rent from my evicted tenant in the form of successful collections, the first time I’ve ever experienced that in my investing career. That boosted my cash flow ~$2,500 from what it would have otherwise been, somewhat offsetting my losses from 2024 and allowing me to cash flow over $4,500 for the year.

Still, my total cash flow here since I bought the house in 2022 is negative, as is equity growth. This will be one where I’ll have to make my returns in the out years, because the cash flow potential isn’t great here right now even if things go smoothly. Still, it’s a solid house that I intend to hold.

About the Author

Hi, I’m Eric! I used cash-flowing rental properties to leave my corporate career at age 39. I started Rental Income Advisors in 2020 to help other people achieve their own goals through real estate investing.

My blog focuses on learning & education for new investors, and I make numerous tools & resources available for free, including my industry-leading Rental Property Analyzer.

I also now serve as a coach to dozens of private clients starting their own journeys investing in rental properties, and have helped my clients buy millions of dollars (and counting) in real estate. To chat with me about coaching, schedule a free initial consultation.