Memphis Rental Property #13

Last updated: 2026

NOTE: This article was published in 2026, but I acquired this property back in 2019. At the bottom of the article, the Annual Updates section provides details on how the property has fared since then.

Let’s take a look at lucky Property #13! In case you missed it: this was one of the 14 I houses I purchased very quickly from May to September of 2019 — my opening acquisition sprint after I left my “first career” in retail, sold my NYC condo to become a renter, and used the proceeds to start building a portfolio that would generate real cash.

This is another of my nicer homes, and sits on the southeast side of town close to the Mississippi border in the desirable Ragan Farms area. It’s also a relatively new home, built in 1995.

The other notable perk of this property is that it sits in an unincorporated pocket, which means that it is exempt from city taxes (only county taxes are applicable.) This makes the cash flow/financials a bit better on this house than they would otherwise be.

Alright, let’s take a closer look at this house and deal!

Property #13: The Deal

I sourced this house the boring, easy way: it was publicly listed on MLS. While other deal-sourcing methods get a lot of attention (i.e. driving for dollars, postcard campaigns, off-market properties, seller financing, and more), it’s worth remembering that the vast majority of properties are bought and sold the traditional way — just like this one was.

The house was vacant at the time of purchase. It had been listed at $129,900, and my initial offer was $120,000. The seller countered back at $124,900, which I accepted.

Here are some additional facts about this particular house:

3-beds, 2 full bath

In the 38141 zip code, solid B neighborhood

Built in 1995

1,179 square feet of interior space

Central air

LVP/tile floors throughout

Driveway, no covered parking

Expansive backyard

Property #13: Due Diligence

Reviewing the history of this deal, this is another house where I never performed a full licensed home inspection. This is sort of shocking, since today I would ALWAYS get that inspection.

In lieu of that, I did get a rehab inspection from my property manager at the time, which called out the need for full interior paint. It also indicated that the HVAC systems were old, and likely near end of life. As a result of these findings, I requested a seller credit of $2K to help defray these likely costs. Unfortunately, the seller refused to budge, and I made the decision to proceed with the deal anyway. But the warning signs were there, and they would manifest pretty quickly (as you can see in the Annual Updates section below.)

Then, the appraisal came in low at $115,000, which meant that my lender would only provide a loan based on that valuation (meaning I’d have to bring more cash to the deal to cover the difference.) Once again, though, the seller dug in, and was unwilling to reduce the contract price — I even offered to meet them in the middle at $120,000, which they refused.

In hindsight, I probably should have walked from the deal at that point. The property had been listed 5 months, and the seller likely would have come back to the table if I walked. But I was in a hurry to get my money deployed and get the portfolio built, so I decided to move forward. I ended up getting an 80% LTV loan of $92,000, when meant my initial cash in the deal was $32,900.

I don’t have good photos of the house from the time of purchase, but here are a few following a more recent turn, just to give an idea:

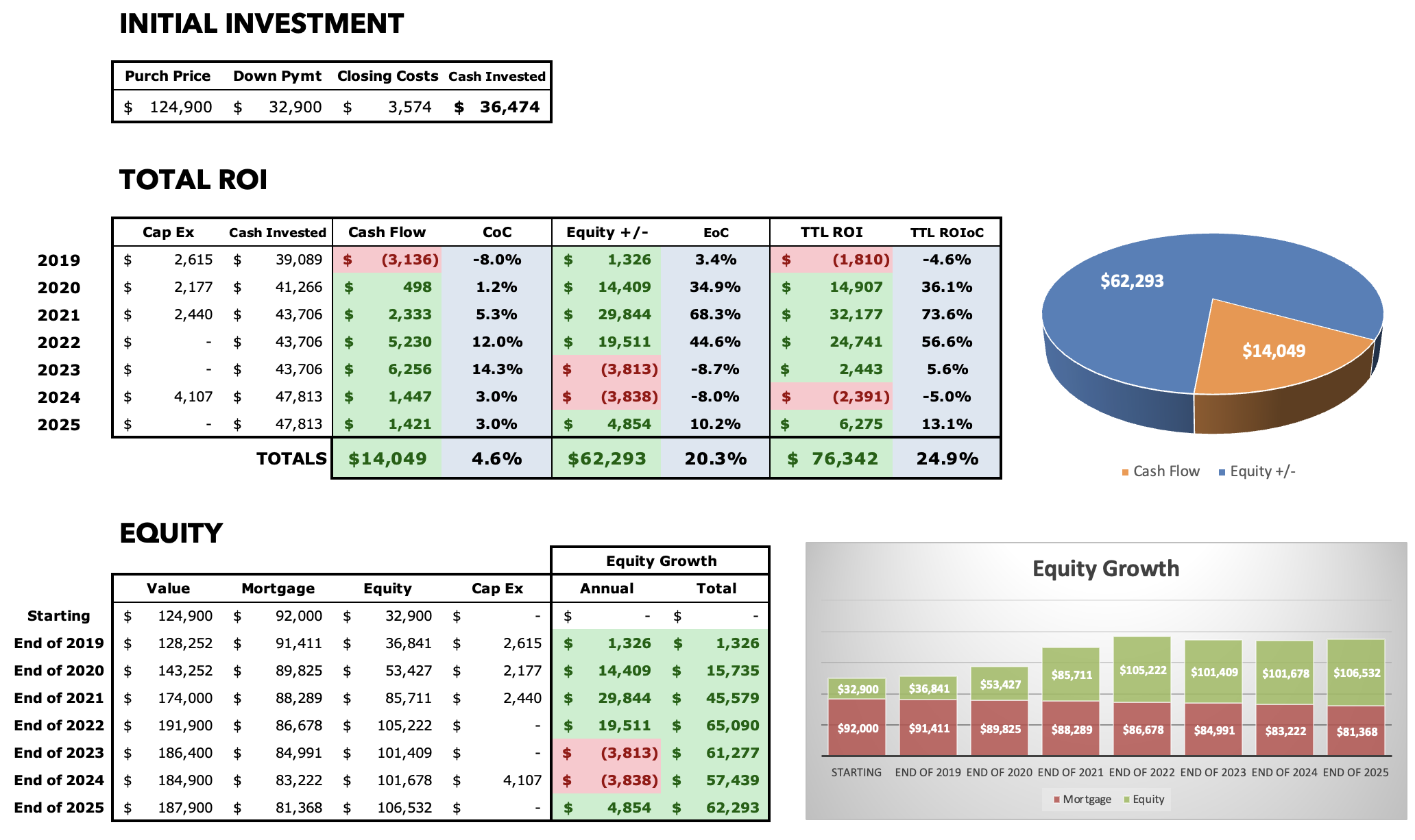

Property #13: The Financials

I secured a conventional 30-year fixed rate loan at 4.70%, with a 20% down payment. Note that in the figures below, I use a 25% down payment — because of the extra cash I had to bring to the deal above the appraisal price, my functional down payment was ~25%.

Like many of my other loans, this mortgage is actually in my spouse’s name alone, a strategy you can use as a married couple to expand your access to conventional financing (max of 20 loans vs. the normal 10).

The house was vacant, and I expected to get $1,100 in rent for it.

As I mentioned at the top, this house sits in an “unincorporated” area of town, which means that no city taxes are due (not to Memphis, nor any of the other incorporated places surrounding Memphis, such as Bartlett, Germantown, and others.) This gives a slight boost to the cash flow numbers on the house.

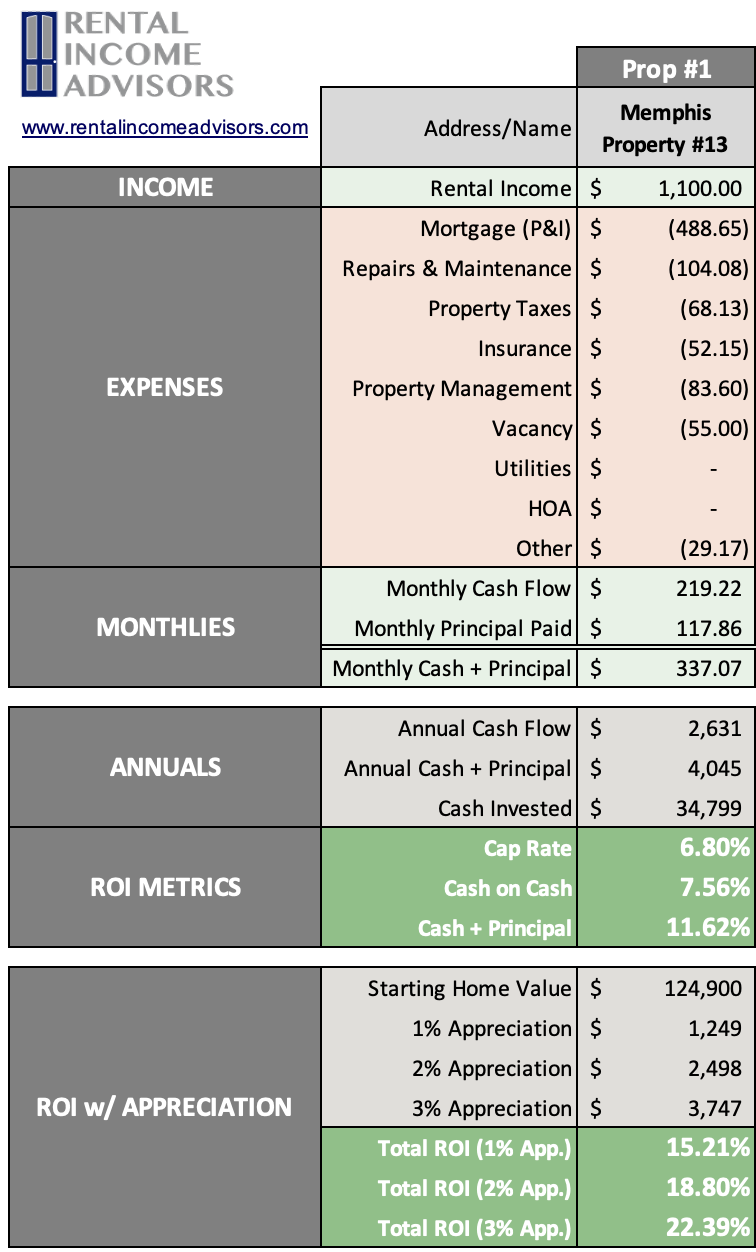

I used the RIA Property Analyzer to input the original figures from this deal, so you can see what it would have looked like at the time:

Purchase Price: $124,900

Monthly Rent: $1,100 (projected)

Monthly Cash Flow: $219

Cap Rate: 6.8%

Cash on Cash Returns: 7.6%

Total ROI 2% Appreciation: 18.8%

(Want to use this calculator? It’s free!)

OR

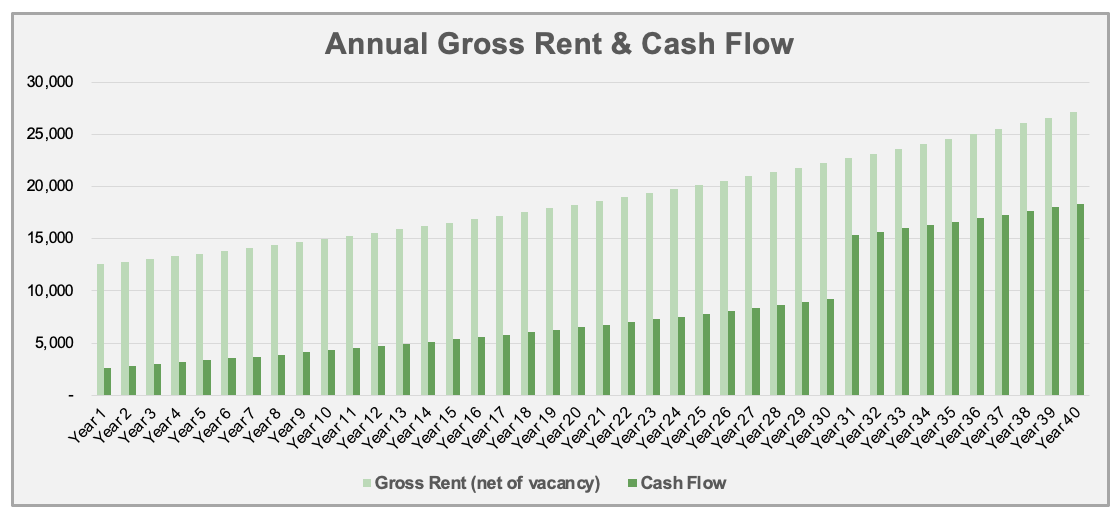

Using the multi-year model in the RIA Property Analyzer, we can visualize some of the main long-term trends assuming a long-term inflation rate of 2%:

Cash flow increases over time. This is mostly because rent and expenses are expected to rise with inflation, but one major expense (my mortgage) is fixed.

Cash Flow Year 1: $2,631

Cash Flow Year 10: $4,288

Cash Flow Year 25: $7,799

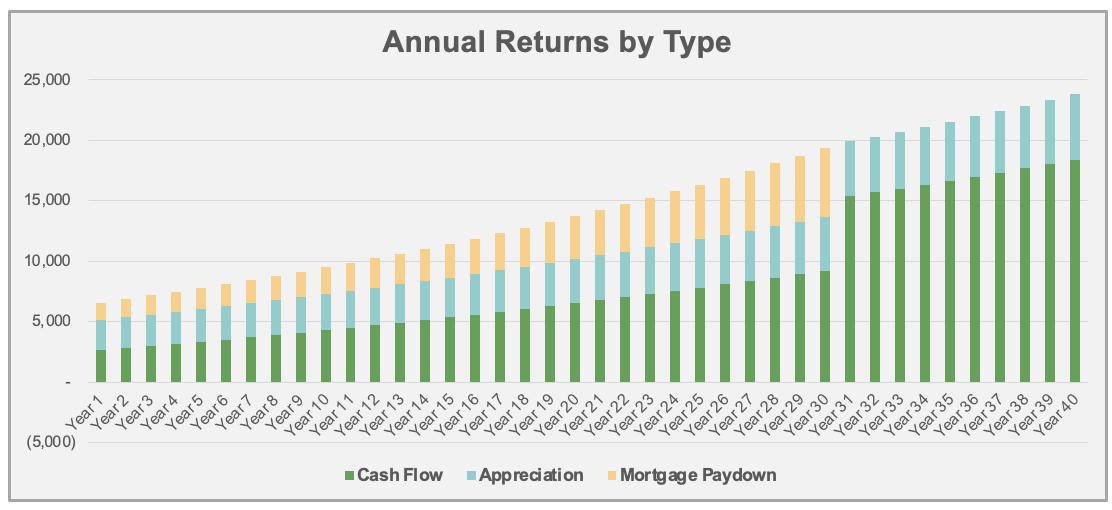

Mortgage paydown accelerates over time. This is because of the way banks amortize loans – each month, a little bit more of your fixed payment is principal, and a little bit less is interest.

Mortgage Paydown Year 1: $1,445

Mortgage Paydown Year 10: $2,215

Mortgage Paydown Year 25: $4,510

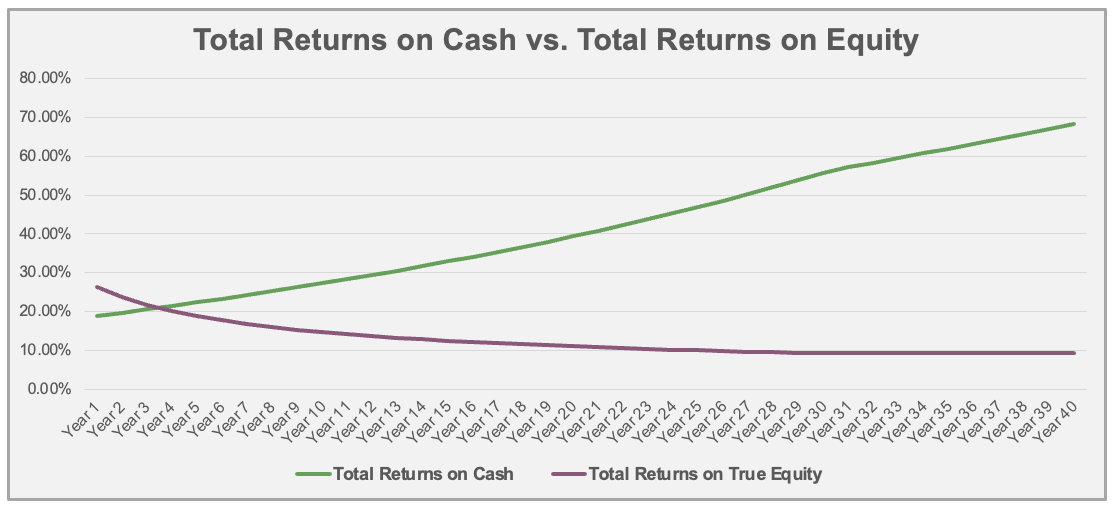

Total returns on cash increases over time. This is a consequence of the first two graphs – I will make greater total returns over time on the same initial investment of cash.

Total Returns on Cash Year 1: 18.9%

Total Returns on Cash Year 10: 27.3%

Total Returns on Cash Year 25: 46.9%

Overall, this is a great property, but I probably didn’t get as good a deal on it as I should have. Some of the major cost centers (HVAC, furnace) were aged, and the appraised value came in low, but I didn’t get any concessions for any of that. And I did end up paying for those things in the first few years. Still, things have turned out fine, and will continue to improve over time.

This is the beauty of long-term buy and hold investing: you don’t have to get it perfect at the closing table because the long-term “wind at your back” will overcome a lot of initial mistakes.

Property #13: The Deal Sheet

Finally, to sum up Property #13 and its financials, here’s the full “deal sheet”:

Looking for YOUR Next Property?

If you need help finding, analyzing, and purchasing YOUR next property — or your first one! — schedule a free initial consultation with me. I’ve helped over 120 private coaching clients invest with confidence and build cash-flowing rental portfolios of their own.

Annual Updates

For all Property Spotlights, I come back at the end of each year to provide a brief narrative of what happened at the property that year. I also update my annual and cumulative figures for the property, including cash flow, equity growth, and occupancy.

2019

Things were not smooth out of the gate. The first problem was that I had trouble renting the house at the expected rate of $1,100/mo., and ultimately had to drop the price. It eventually rented for $995 on a 2-year lease, but it took several months of vacancy to do so, and my cash flow figures don’t look nearly so nice at this reduced rent.

Then, the initial warning signs on the aged HVAC system led to several repairs, and ultimately a full $2.6K replacement less than 6 months after I closed.

Even without considering the CapEx, my cash flow was quite negative for the year. Tough start, but Year 1’s are rarely great.

2020

It was a quiet year until the tenant broke their lease and turned in the keys in December due to unspecific personal issues. As part of the turn work, I took the opportunity to install some new LVP flooring ($2K of CapEx), and spent several thousand on other minor touch-ups. This time, I had no trouble re-renting the property — it went quickly for $1,195/mo. even though it was listed in Dec/Jan, probably the worst time to have a vacancy. Hard to account for the difference experiences in renting the house twice in two years — just luck of the draw I guess, or the shifting of the economy during the pandemic.

Despite the turn expenses, I managed to eke out a small positive cash flow this year, and things look healthier going forward thanks to the higher rent achieved.

2021

The tenant moved in in February, and paid rent on time each month. There were ~$1.5K in maintenance & repairs this year spread across numerous small issues. But there was also more CapEx: I spent $1.8K to replace the furnace, and another $650 for a new dishwasher.

Still, cash flow great to $2,300, the best year so far at this house. And like nearly everywhere at this time, home valuations were rising steeply during the pandemic housing boom.

2022

Finally a smooth year here. The tenant renewed in March at $1,242/mo., and maintenance & repairs were minimal at ~$600 total. And no CapEx! Cash flow grew to over $5,200.

2023

More of the same this year: the tenant renewed again at $1,295/mo., and I again spent only $600 on repairs. Cash flow jumped to over $6,200, while home valuations finally leveled off after several years of steep gains.

2024

The tenant did not renew at the beginning of the year, so I had to turn the property. The rent-ready work cost ~$5K, and I spent another $4K on CapEx for new kitchen countertops, exterior paint, and a new dishwasher (again! — the latch was broken and it was deemed too difficult/costly to repair vs. just buying a new one.)

Once again, though, the house rented easily, this time at $1,395/mo., or $100 higher than the previous tenant was paying. Because of this higher rent, I was able to produce a small positive cash flow of ~$,1400 for the year.

2025

Unfortunately, the new tenant vacated after only one year. This is very disappointing, as frequent turns are a cash flow killer (even when I’m entitled to retain the security deposit, which I do in many cases.) The turn cost $4.5K, much more than I would have hoped given the tenant was only there for a year — but they didn’t maintain the house that carefully, and full interior paint was needed again.

I attempted to rent this at $1,495, but failing to get much traction at that price, we lowered it aggressively to $1,345 and it rented quickly. This is a bit down from the previous tenant’s rent, but it’s always best to cut aggressively and get it rented rather than reducing the price bit by bit and wasting time. The overall story was similar here to 2024, and so was the cash flow at ~$1,400.

About the Author

Hi, I’m Eric! I used cash-flowing rental properties to leave my corporate career at age 39. I started Rental Income Advisors in 2020 to help other people achieve their own goals through real estate investing.

My blog focuses on learning & education for new investors, and I make numerous tools & resources available for free, including my industry-leading Rental Property Analyzer.

I have also served as a coach to over 100 private clients starting their own journeys investing in rental properties, and have helped my clients buy millions of dollars (and counting) in real estate. To chat with me about coaching, schedule a free initial consultation.