Memphis Rental Property #24

Last updated: 2026

NOTE: All figures and statements in this article were accurate as of the time of initial publication in 2022. Check out the Annual Updates section at the bottom of the post to see how the property has performed since then.

This property was purchased in December 2022, but unlike several other properties I bought that month, it was not part of my 1031 exchange. Instead, this was purchased with my own funds leftover from the sale of a different NYC rental condo last summer. In fact, I bought two essentially identical properties — Property #25 is a carbon copy of this one, which closed a few months later.

These properties are different from anything I’ve ever purchased in Memphis, in several respects:

They’re condos. I wrote an entire article about why condos generally don’t make good rental properties.

They have only 2 bedrooms. Everything else in my portfolio is at least 3-bedroom, with the exception of the 2BR units in my duplex.

I used private financing, and my loans have a 5-year balloon. All my other loans are conventional mortgages or asset-based rental loans, and again I wrote an entire article about the dangers of more creative financing options, especially those with balloon payments.

So what in the world am I thinking? And why am I ignoring all of my own advice?

Let’s find out and get into the details of these deals!

Property #24: The Deal

This property was offered from a turnkey provider that I’ve worked with many times in the past. He had an interesting idea: he was going to essentially take over a multi-structure condo with ~60 units, and over time flip all the units, sell them to his investors, and manage the property on their behalf — serving as both property manager and de facto head of the condo HOA.

The condo was a mix of 1, 2, and 3-bedroom units, all relatively small. Each building houses several units on one level, kind of like little duplexes. The complex was built in 1950, but most units were in desperate need of a refresh, including new roofs, new windows, and more.

He also arranged for in-house financing for these units. Buyers could get up to 65% of the purchase financed, with a 5% interest rate (much lower than was available with regular mortgages, whose rates were nearly 7% at that time.) The loan would follow a regular 30-year amortization schedule, but it had a large initiation fee, and had a 5-year balloon — in other words, after five years, the remaining loan balance would be due in full.

I thought this was a very creative model, but there are some obvious risks here. The turnkey provider will essentially control everything in the condo, and there would not be a normally-functioning condo board as a check on him. He could pretty much make any decision he wanted to, including imposing assessments or an increase in the monthly HOA fee — which are some of the biggest risks of condos as rental properties. Still, he has a vested interest in ensuring the satisfaction of the condo owners, whom he sold the units to with a promise to manage them profitably as investments. Plus, his local network would allow him to contract regular maintenance work at a low cost, which would benefit owners. In the end, it’s a matter of trust: I trust that he will make sound fiscal decisions in the management of the complex, and in the use of HOA funds.

And while the financing is a bit more aggressive than I’m used to due to the 5-year balloon, it also gave me an opportunity to get several more loans with very factorable interest rates at a time when I had exhausted my access to conventional mortgages. Plus, the properties were quite cheap and the loans small, so I felt comfortable that at the end of the 5-year period, I could either re-finance into new non-conforming rental loans if that was favorable, or simply pay off the loans to juice the cash flow of these properties (using cash on hand, or by re-financing another rental with significant equity in it.)

Let’s take a look at what these little condos look like inside. My units are 2-bed/1-bath, and the interior finishes are very similar to my other turnkey homes. As a bonus to the normal turnkey property rehab work, the windows were replaced as well:

In the end, what attracted me most to the unusual deals? It was the numbers! These should be very strong cash flow properties despite the $70 monthly HOA fees, largely due to the strong price-to-rent ratio. The purchase price on this condo was $70,000, and it rented quickly and easily for $850/month. In fact, there was a tenant in place before I closed on the property.

Since this was a turnkey-condition property with no due diligence or rehab, let’s jump right into the full set of numbers.

Property #24: The Financials

I financed 65% of this $70,000 purchase with the in-house financing at 5%. So my down payment was $24,500, and I incurred $7,360 in closing costs, more than typical due to the higher fees associated with this loan. I used the RIA Property Analyzer to run the final numbers on this property – here are the key metrics that the analyzer calculated for me:

Purchase Price: $70,000

Monthly Rent: $850

Monthly Cash Flow: $273

Cap Rate: 8.87%

Cash on Cash Returns: 10.29%

Total Returns w/ 2% Appreciation: 16.75%

(Want to use this calculator yourself? You can!)

OR

These days, getting more than 10% cash-on-cash returns is very difficult, largely thanks the larger interest payments on loans. So I was pretty excited to realize that these little condos could generate such strong cash returns, despite the hit of a $70 HOA fee each month.

This is due to very strong price-to-rent ratio, but there are a few other factors in play as well. First, the property taxes on these condos are very low compared to single family homes. And second, they are relatively inexpensive to insure, which is typical of condos.

Using the multi-year model in the RIA Property Analyzer, we can visualize some of the main long-term trends (assuming an inflation rate of 2%):

Cash flow increases over time. This is because rent and expenses are expected to rise with inflation, but one major expense (my mortgage) is fixed. (This assumes a 30-year mortgage — of course I’ll have to pay it off or re-finance after 5 years, as discussed above.)

Cash Flow Year 1: $3,280

Cash Flow Year 10: $4,491

Cash Flow Year 25: $7,058

Mortgage paydown accelerates over time. This is because of the way banks amortize loans – each month, a little bit more of your fixed payment is principal, and a little bit less is interest. One downside of the 5-year loan is that I don’t capture the biggest benefits of this trend, which accrue at the end of the 30-year amortization.

Mortgage Paydown Year 1: $671

Mortgage Paydown Year 10: $1,052

Mortgage Paydown Year 25: $2,223

Total returns on cash increases over time. This is a consequence of the first two points – I will make greater total returns over time on the same initial investment of cash.

Total Returns on Cash Year 1: 16.8%

Total Returns on Cash Year 10: 22.6%

Total Returns on Cash Year 25: 36.2%

Overall, I’m intrigued by this property, and very curious to see how it does over time. This one (and its twin, Property #25) are quite different from any of my other Memphis holdings — who would have thought I would buy condos?! — but of course I’m very pleased with the ROI numbers. I’ll be interested to see how the condo development fares over the coming years, and my turnkey provider continues to flip and sell units. It should become a more desirable place to live in general, which should be good for both rental rates and home values.

The only question on these is how I will proceed when the 5-year loan period expires. My choices at that point will be to re-finance the loans (into a standard rental property loans), or simply pay off the balance. Of course, I could also sell the properties at that time, but I don’t anticipate wanting to offload them unless they perform much worse than I anticipate they will.

Property #24: The Deal Sheet

Finally, to sum up Property #24 and its financials, here’s the full “deal sheet”:

Looking for YOUR Next Property?

If you need help finding, analyzing, and purchasing YOUR next property — or your first one! — schedule a free initial consultation with me. I’ve helped dozens of private coaching clients invest with confidence and build cash-flowing rental portfolios of their own.

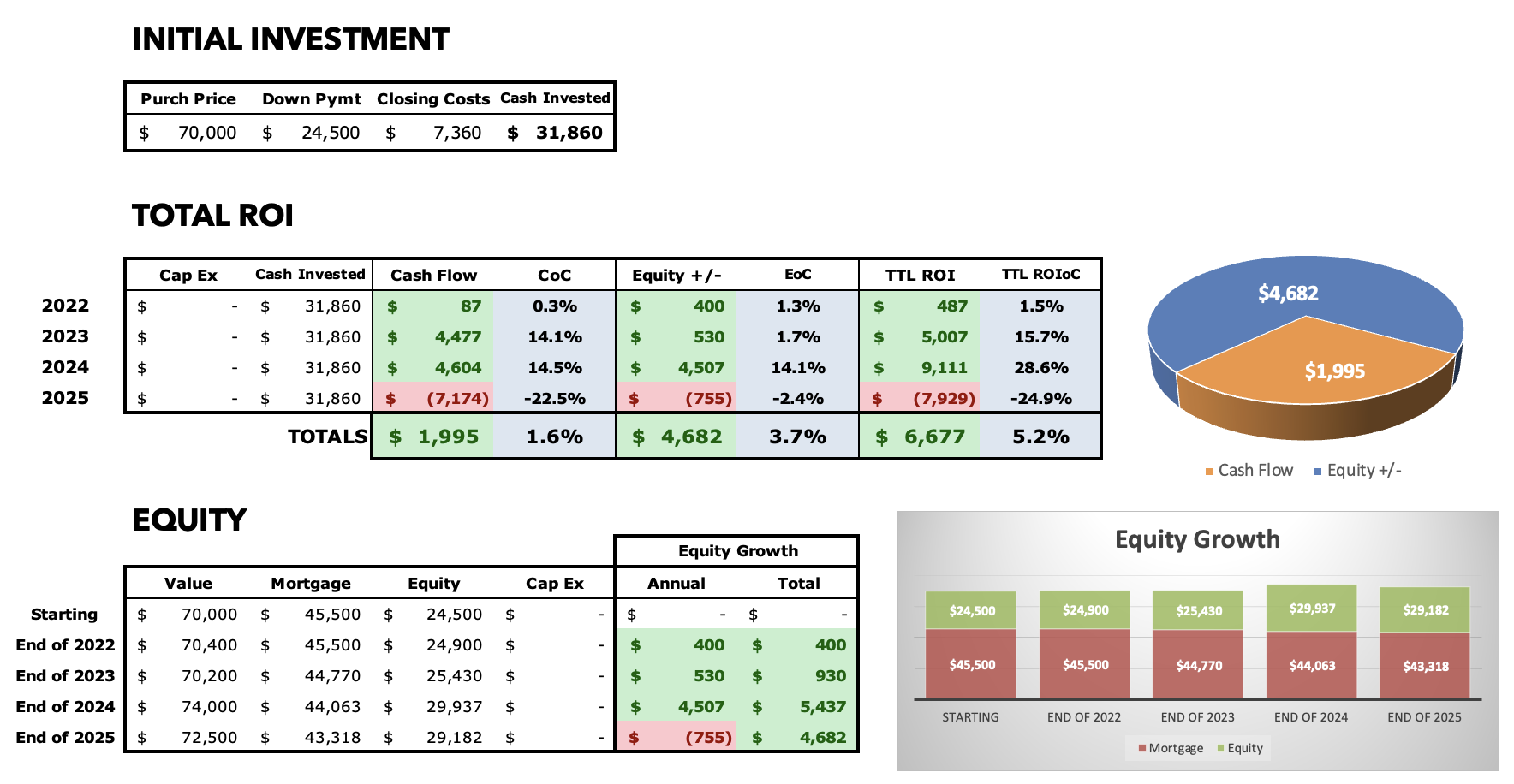

Annual Updates

For all Property Spotlights, I come back at the end of each year to provide a brief narrative of what happened at the property that year. I also update my annual and cumulative figures for the property, including cash flow, equity growth, and occupancy.

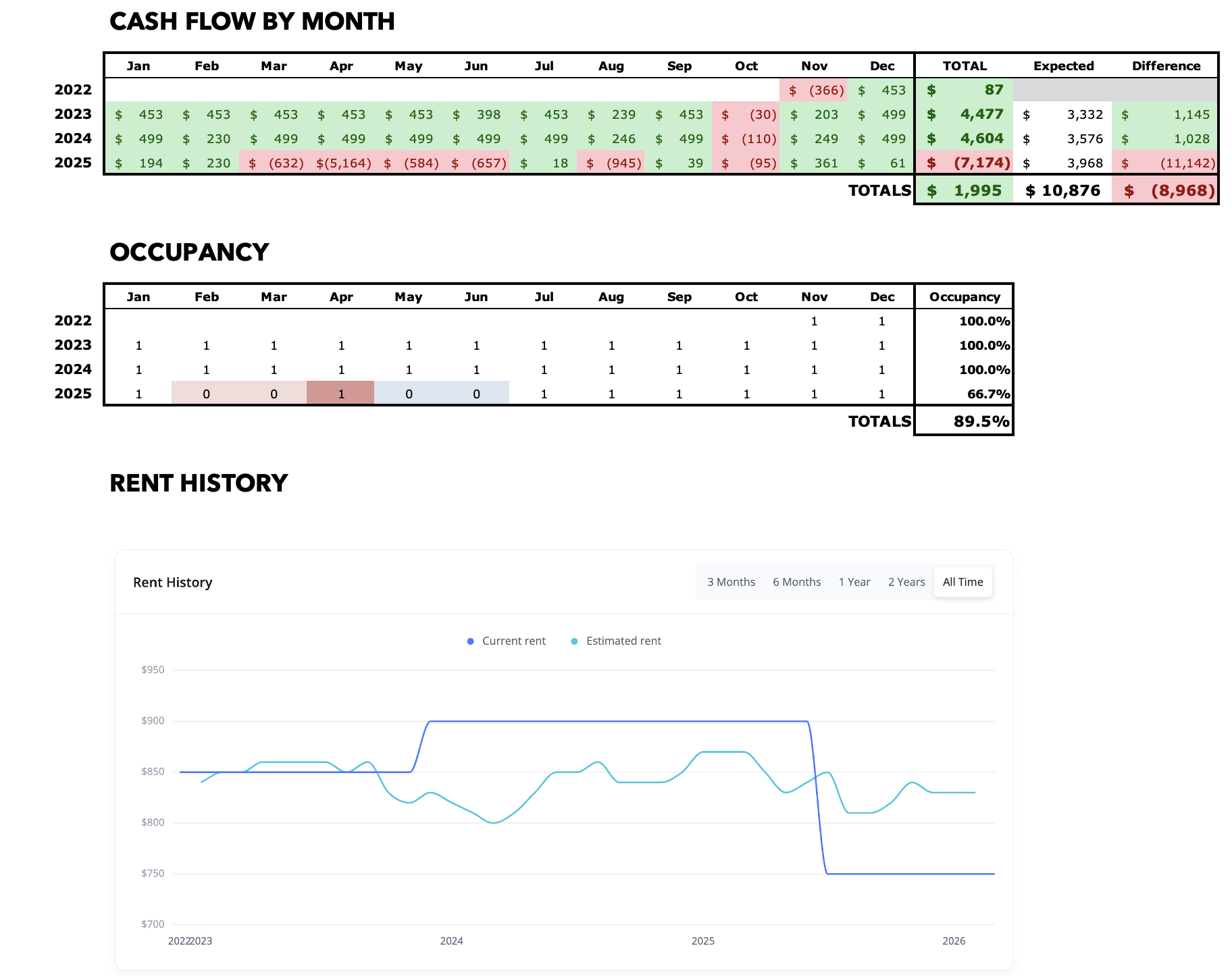

2023

So far, my experiment with these two little condos is going quite well. At this unit, 2023 was a strong year. The tenant is stable, and renewed for another year with a $50 increase. I had no maintenance costs at all, which allowed to easily exceed my pro forma cash flow. So far so good!

2024

This unit had another great year. The tenant renewed again, with no increase — $900/mo. is already market rent, so I didn’t want to raise them any higher. For the second straight year, there was $0 in maintenance, so I exceeded my cash flow target once again.

2025

The smooth sailing at this property ended this year…in fact, it basically crashed into the reefs. First, my tenant defaulted on their payments shortly after renewing their least at the end of 2024, which led to a 5-month eviction/turn. The turn costs were $5K+, not at all cheap considering this is a very small unit and was bought turnkey.

Then, the every-four-years Memphis property tax reassessment led to a tripling of my property taxes. A number of my other properties also had noticeable increase, but this one (and its twin sister, Property #25) were the worst impacted. This reduces the future cash flow potential of this property, and also pushes valuations down.

In the final blow, I wasn’t able to re-rent the property anywhere near what the previous tenant was paying. I ended up renting it for $750/mo. on a 2-year lease, which was super-disappointing. The combination of these factors means I’m expecting less than $1K of annual cash flow from this unit going forward. If I can achieve higher rents in future years, that will help a lot. But my investing thesis that these condo units would be small, simple, cash flow machines has run into the reality that they are condos…which I always said you shouldn’t buy as rentals. Perhaps I should have listened to my own advice.

About the Author

Hi, I’m Eric! I used cash-flowing rental properties to leave my corporate career at age 39. I started Rental Income Advisors in 2020 to help other people achieve their own goals through real estate investing.

My blog focuses on learning & education for new investors, and I make numerous tools & resources available for free, including my industry-leading Rental Property Analyzer.

I also now serve as a coach to dozens of private clients starting their own journeys investing in rental properties, and have helped my clients buy millions of dollars (and counting) in real estate. To chat with me about coaching, schedule a free initial consultation.