Memphis Rental Property #19

Last updated: 2026

NOTE: All figures and statements in this article were accurate as of the time of initial publication in 2021. Check out the Annual Updates section at the bottom of the post to see how the property has performed since then.

About a month ago, I closed on my most recent rental property, my 19th property in Memphis and my 20th door. (Milestone achieved!)

This property has a lot in common with Memphis Property #17: both are 3-bed/1 bath single family homes in the same C neighborhood; both were occupied at the time of closing; and both had recent turnkey renovations. However, this property’s turnkey rehab was about 5 years ago, whereas I bought Property #17 directly from a turnkey provider.

This will probably be my last new property for a while, until I’m able to free up some more cash — either by selling one of my New York City condos, or doing a cash-out refi on Memphis Property #18. (2024 update: I’ve now done both of those things!)

This one was a pretty straightforward deal. Let’s get into the details!

Property #19: The Deal

This house was listed publicly on the MLS, so it came to me via a Zillow alert. I have been looking to expand my holdings in C neighborhoods, so this particular neighborhood has been a prime target for me. The house was pretty typical for the area: a modest 3-bed/1-bath, built of brick in 1948 and containing about 1100 square feet.

I liked that the property had a turnkey rehab about 5 years ago — this ensured that the roof and HVAC were young and in reasonably good shape. The property also had a rent-ready rehab a few months prior, in preparation for the tenant who was currently in place. So overall, I thought the home was likely to be in pretty good shape — and the photos supported that:

The house was listed at $76,900 (a bit high for the neighborhood) with the tenant paying $775/month. I quickly submitted an offer at $67K, but learned that the seller accepted a different offer. Still, my agent told the seller to keep my offer on the back burner in case the first contract fell through.

As it turned out, the first offer DID fall through! So the seller came back to me and countered at $74K. I countered back at $69,500, which the seller accepted on the condition that the price not be further negotiated after inspection. Given my assumption that the home was in reasonably good shape, I agreed to those terms.

Property #19: Due Diligence

When buying an occupied property, it’s critical to examine both the existing lease (the terms of which you must inherit), and the tenant’s payment history, often called the “tenant ledger”. The lease was from a reputable PM in town, and looked fine. The tenant ledger looked great — the tenant had only been in place ~4 months, but to that point they had always paid on time. (Check out the tenant ledger yourself for a perfect example of the kind of clean payment history you’re looking for when inheriting a tenant.)

I also asked for the home’s maintenance history, and the scopes of work for both the turnkey rehab and the more recent rent-ready rehab. All of this was provided to me quickly: the rehab scopes were as expected, and the maintenance history surfaced no red flags.

From there, I ordered a home inspection, which also turned up no serious concerns. (If you like, you can check out the home inspection report as well.) Normally I would go back and ask for a small seller concession to deal with a few issues that the inspection turned up, such as the windows being painted shut — but because the issues were small and I’d already agreed not to renegotiate the price, I was fine to move forward at the contract price of $69,500.

Property #19: The Financials

I used the RIA Property Analyzer to run the numbers on this property – here are the key metrics:

Purchase Price: $69,500

Monthly Rent: $775

Monthly Cash Flow: $194

Cap Rate: 8.82%

Cash on Cash Returns: 10.42%

Total Returns w/ 2% Appreciation: 19.35%

(Want to use this calculator yourself? You can!)

OR

Using the multi-year model in the RIA Property Analyzer, we can visualize some of the main long-term trends:

Cash flow increases over time. This is because rent and expenses are expected to rise with inflation, but one major expense (my mortgage) is fixed.

Cash Flow Year 1: $2,332

Cash Flow Year 10: $3,528

Cash Flow Year 25: $6,063

Mortgage paydown accelerates over time. This is because of the way banks amortize loans – each month, a little bit more of your fixed payment is principal, and a little bit less is interest.

Mortgage Paydown Year 1: $625

Mortgage Paydown Year 10: $1,084

Mortgage Paydown Year 25: $2,709

Total returns on cash increases over time. This is a consequence of the first two points – I will make greater total returns over time on the same initial investment of cash.

Total Returns on Cash Year 1: 19.4%

Total Returns on Cash Year 10: 28.0%

Total Returns on Cash Year 25: 49.2%

Overall, I’m quite happy with the returns on this property. I was able to get over 10% cash-on-cash returns despite my higher loan costs, and I think I got a solid house at a fair price in one of my target neighborhoods, with a tenant who pays the rent on time.

About My Loan Costs

Just as I did with Memphis Property #17, I used a nonconforming loan from Lending Home as my source of financing for this property. I have unfortunately exhausted my “golden tickets” — aka conventional mortgages — so I have to resort to other forms of financing.

As I explained in my article on rental property funding options, I view nonconforming loans as my next-best option after conventional mortgages because I can still get a 30-year fixed rate, while avoiding the risks of other forms of funding that often have adjustable rates, balloon payments, and other pitfalls. To me, despite the higher rates that I pay for these nonconforming loans — 6.125% in this case — they still offer strong long-term returns with the greatest peace of mind.

But those higher rates DO make a meaningful difference to my cash flow and my rate of return. Let’s see how the same deal would look changing just one parameter — lowering my interest rate from 6.125% to 4.0% (a typical rate on a conventional investment loan today):

As you can see, the lower interest rate reduces my monthly mortgage payment from $316 to $248, and as a result, my monthly cash flow increases from $194 to $262, and my cash-on-cash returns jump from 10.4% all the way to 14.1%. This is no surprise, but it’s a big difference.

Less expected is that the lower interest rate also INCREASES my monthly principal paid, from $50 to $75. The lower your interest rate, the higher the proportion of your payment goes to principal.

These benefits compound in the Cash + Principal calculation, where the rate of return is now 18%, compared the 13% that I can expect with my higher interest loan. These higher returns are what any of my coaching clients, who nearly always use conventional loans, could expect to get on this same deal.

Property #19: The Deal Sheet

Finally, to sum up Property #19 and its financials, here’s the full “deal sheet”:

Looking for YOUR Next Property?

If you need help finding, analyzing, and purchasing YOUR next property — or your first one! — schedule a free coaching consultation with me. There are no obligations or commitments of any kind, so go ahead and take the first step!

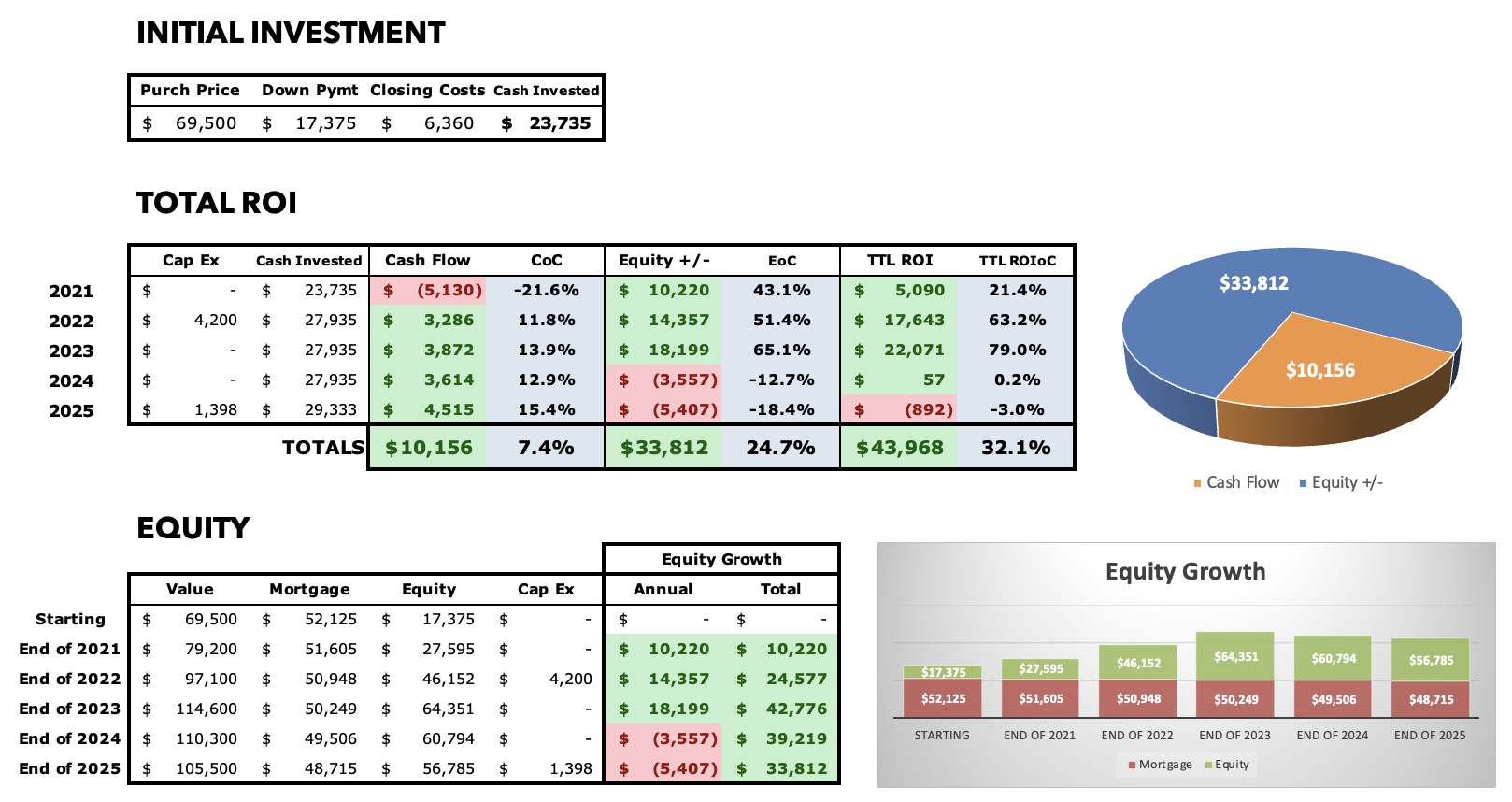

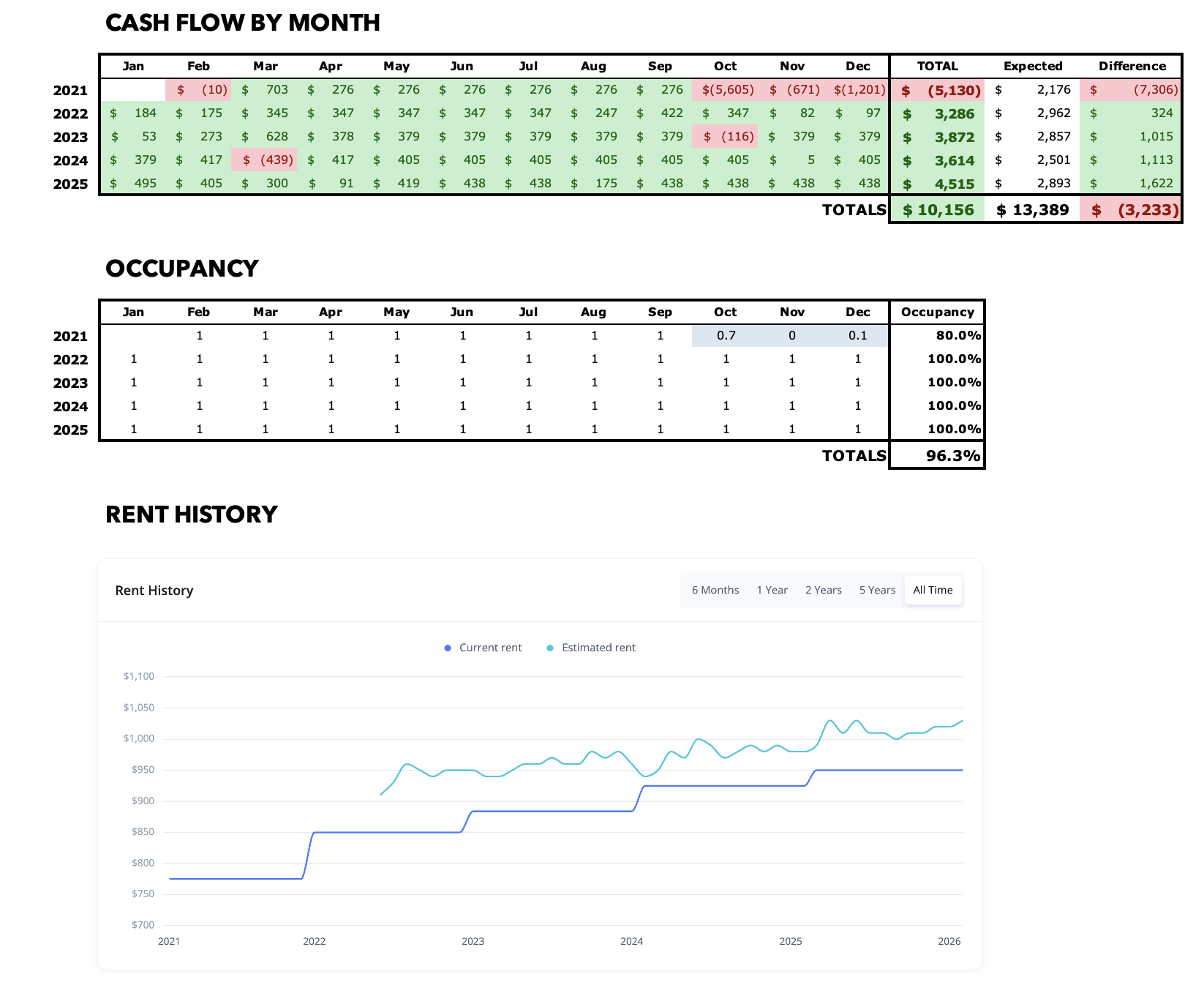

Annual Updates

For all Property Spotlights, I come back at the end of each year to provide a brief narrative of what happened at the property that year. I also update my annual and cumulative figures for the property, including cash flow, equity growth, and occupancy.

2021

I bought this house in the beginning of 2021 with a tenant in place. Unfortunately, that tenant had to vacate unexpectedly at the end of September, so I had a turn right out of the gates with this one — and it was a “first turn”, and ended up costing over $5K. Doh! Then in November, I had a big CapEx surprise in the form of a $4,200 sewer replacement. Altogether not a great year. The only good news is that I have a new tenant in place going in to 2022, when I hope the property will stabilize and produce some cash flow.

2022

A much better year! I exceeded my cash flow target by over $350, avoiding any large maintenance issues. The tenant has turned out well, and renewed at the end of the year with a small increase. In 2023, I’m hoping I can get into the green for lifetime cash flow on this house.

2023

Another solid year at this house. The tenant continues to be great, with their next renewal in early 2024 (planning a modest increase if they decide to renew.) A few small maintenance issues, including a $500 job to add a sewer cleanout, but still exceeded by cash flow target by over $1K, and got into the green for the lifetime of the property, as hoped.

2024

Third consecutive year with strong results at this house. The tenant pays on time and takes good care of the house; they renewed for a third year, now paying $925/mo. Repair costs were in line, and included $700 for a tree that fell during a spring storm (no damage, just cleanup.) Still exceeded cash flow target by another $1K, just like in 2023.

2025

Another smooth year resulting in strong cash flow of over $4,500. The tenant has never had a late payment, and renewed at $950/mo.

Operations were stable here, with only $700 of maintenance expenditures. I did have to install a new water heater, a $1,400 CapEx item.

About the Author

Hi, I’m Eric! I used cash-flowing rental properties to leave my corporate career at age 39. I started Rental Income Advisors in 2020 to help other people achieve their own goals through real estate investing.

My blog focuses on learning & education for new investors, and I make numerous tools & resources available for free, including my industry-leading Rental Property Analyzer.

I also now serve as a coach to dozens of private clients starting their own journeys investing in rental properties, and have helped my clients buy millions of dollars (and counting) in real estate. To chat with me about coaching, schedule a free initial consultation.