Memphis Rental Property #18

Last updated: 2026

NOTE: All figures and statements in this article were accurate as of the time of initial publication in 2021. Check out the Annual Updates section at the bottom of the post to see how the property has performed since then.

It’s been nearly six months since I closed on Memphis Property #17, which was the first property I acquired since I bought 16 properties in under a year in an all-out effort to create enough monthly income to leave my office job. (Which I did!) If you’ve followed my monthly portfolio updates, you might recall that I actually closed on this property in November, so why has it taken me three months to post about it?

Well, this property was a little different. First of all, it’s my first duplex — two rental units under one roof. And second, it’s the first property I’ve purchased that required rehab work prior to placing a tenant. When I closed on the property, one side was occupied, but the other side was vacant and needed a lot of work. I wanted to get the rehab done, and a tenant placed, so I could tell the complete story of this property, including the final numbers.

There were definitely some twists and turns on this deal. But it turned out great, and it’s now the best cash-flowing property in my entire portfolio, with an impressive cap rate of almost 15%. I think this property illustrates that small multi-family properties can be powerful cash flow generators, and also the potential value of buying properties that need some work.

Let’s get into the details!

Doubling Down on Memphis

Many of my coaching clients ask me if I’m considering branching out into a second market, or if I’ll keep buying in Memphis. For now, the answer is that I’m continuing to build my portfolio in Memphis.

There are a couple of big reasons for this. First and foremost, Memphis continues to be a great cash flow market. The recent research that I did for my review ofthe 12 Best Cash Flow Markets reinforced that Memphis was a market that still ticks all of the boxes for me. Here are some of the details on the markets I reviewed, if you’re curious:

But there are some other reasons in play here, too:

In Memphis, I now have a strong property manager I trust. The value of this cannot be overstated (which is why I developed a free PM Vetting Tool to help people find the right PM in any market.) Even if there are aspects of another market that compare favorably to Memphis, those advantages could be washed away if I can’t find an equally strong PM.

I’m busy. My roster of coaching clients has been growing, and I’m now spending a good chunk of my time with them, guiding them through the process of buying rental properties. That’s where I want my focus to be for the next 6-12 months, so I can improve and automate aspects of my coaching process. Therefore, now isn’t the time to dive into a new market, which would require time and attention that would split my focus.

I’m lazy. I know the Memphis market, and I have my team in place, so for better or worse, it’s just easier. (I know this is not a great reason, but it’s a reality nonetheless.)

I haven’t closed the door to diversifying into a second market in the future, but for now, I’m doubling down on Memphis.

Property #18: The Deal

There aren’t many multi-family properties in the Memphis market. But there are a few small pockets within certain neighborhoods where duplexes were built, mainly in the 1970’s, and my new property is in one of those pockets.

I was in contract on a different duplex earlier in the year, but that deal fell through after the inspection turned up some troubling problems. Still, I remained interested in buying a duplex. This one was an off-market deal that my local broker presented; it looked like a great opportunity, so I jumped at it.

The property has two 2-bedroom/2-bath units, and was asking $78,500. One side was occupied for $780/month (which is about market rent) and the other side was vacant — and a total mess. The previous owner appeared to be overseas, and to me, it seemed like they were giving up on the investment after a series of maintenance and tenant issues. I offered $74,900 for the property, which was accepted.

The inspection photos of the vacant unit were pretty scary:

I figured the rehab would cost ~$10K, and my PM agreed. Even with that cost, the potential ROI on the property would be outstanding once I placed a second quality tenant in the vacant unit.

I hit a snag with my funding, which I was planning to get through Kiavi, as I did on Property #17. The appraisal took a few weeks to get scheduled, and then it had been ANOTHER few weeks and the appraisal company had still not filed their report. I felt like the seller was getting impatient, and I didn’t want the deal to fall through — so just to get it done, I decided to close on the property in cash. (I normally wouldn’t have this much cash available, but I had recently taken a penalty-free withdrawal from my retirement accounts, an option that was part of the CARES Act passed through Congress earlier in 2020.) I figured I could always go back and do a re-finance to pull cash back out of the property later.

Property #18: The Rehab

After I closed, I had my PM go through the property and provide a Scope of Work, an itemized list of the work they would need to do to bring the property up to rent-ready standard. In addition to what they recommended, I also had them add new cabinets and countertops to the project — they looked old and dingy, and I wanted to start fresh. I also had them remove a broken dishwasher, and replace it with shelving, because I never want to own appliances in my rentals if I can avoid it.

The final rehab cost of ~$9K was pretty close to my earlier estimate of $10K. Click here to view the full Scope of Work in a new tab.

As you can see, the big pieces of work were:

New cabinets and countertops in the kitchen

New LVP flooring in the kitchen

Replace both toilets

Various miscellaneous items

Full interior paint

Full interior cleaning, and yard cleaning

The work took about a month to complete, and everything went as planned. My PM coordinated all of the work, so I had a single point of contact during the rehab. The construction manager provided me with updates along the way, including photos. After the work was done, my PM listed the vacant unit for rent at $765/month, and it went quickly. All told, it was less than eight weeks between my closing on the property and the new tenant moving in — pretty impressive, I think. (And yet more evidence for just how valuable a capable, professional property manager can be!)

Here’s how it all looked when it was done — what an improvement!

Property #18: The Financials

As I mentioned earlier, the financials on this property ended up being VERY strong. I plugged the numbers into the RIA Property Analyzer, assuming a post-rehab of value of $85K, which is just the $75K purchase price plus the cost of the rehab. (Note that if the post-rehab value is assumed to be higher, then the implied Cap Rate would go down, but the Cash-on-Cash returns would remain the same.) Here’s what the numbers look like:

Purchase Price: $74,900

Monthly Rent: $1,545

Monthly Cash Flow: $1,058

Cap Rate: 14.95%

Cash on Cash Returns: 14.76%

Total Returns w/ 2% Appreciation: 16.73%

(Want to use this tool yourself? You can!)

OR

Using the multi-year model in the RIA Property Analyzer, we can visualize some of the main long-term trends:

Cash flow increases over time. Even without a fixed-cost mortgage, and assuming both rent and expenses increase at 2% per year, cash flow still increases over time because rent starts out so much higher than expenses.

Cash Flow Year 1: $12,704

Cash Flow Year 10: $15,182

Cash Flow Year 25: $20,433

Total returns increase over time. Because I paid in cash, I don’t make any returns in the form of Mortgage Paydown; instead, my returns are nearly all in the form of Cash Flow.

Total Returns Year 1: $14,404

Total Returns Year 10: $17,214

Total Returns Year 25: $23,167

Total returns on cash increases over time. This is a consequence of the first two points – I will make greater total returns over time on the same initial investment of cash.

Total Returns on Cash Year 1: 16.7%

Total Returns on Cash Year 10: 20.0%

Total Returns on Cash Year 25: 26.9%

Naturally, I’m extremely happy with the returns on this property! But now I’m faced with another question: after a few more months of “seasoning”, I’ll be eligible to do a cash-out refi and pull some of my equity out of this property.

Should I Do a Cash-out Refi?

The first step of a cash-out refi would be a lender ordering an appraisal on the property. They would use that appraised value as the basis of the loan — for example, if the property appraised for $100K, the lender would be willing to finance up to a certain percentage of that amount, usually 75%. (This is often referred to as loan-to-value ratio, or LTV.)

Immediately you can see that this question will hinge a lot on what that appraised value actually is. The higher the appraised value, the more cash I’d be eligible to pull out of the property and re-invest. (There’s even a chance I could pull ALL my money back out of the property, which mathematically means that my cash-on-cash returns on the property would be infinite. Hard to beat that!)

By this point, astute readers may have noticed something about this story: if I go forward with the cash-out refi, then in essence this property is a BRRRR. Here’s a quick review of what that commonly-used acronym stands for:

Buy: a property in need of a rehab, usually paying in cash or with short-term financing

Rehab: fix the place up

Rent: place a tenant

Refinance: use the new appraised value to pull as much cash as possible out of the property

Repeat: take the cash and start the process over

While I often say I am not a BRRRR investor, that’s basically what I’ve done with this property if I proceed with the refinance. But I’m not certain yet if I WILL pull the cash out. The math around that decision is worthy of its own article, which I plan to publish in the coming months, along with my final decision on whether or not to do the refi, so stay tuned. (UPDATE: I DID eventually do a cash-out refi, which you can read all about here!)

Finally, to sum up Property #18 and its financials, here’s the full “deal sheet”:

Looking for YOUR Next Property?

If you need help finding, analyzing, and purchasing YOUR next property — or your first one! — schedule a free coaching consultation with me. There are no obligations or commitments of any kind, so go ahead and take the first step!

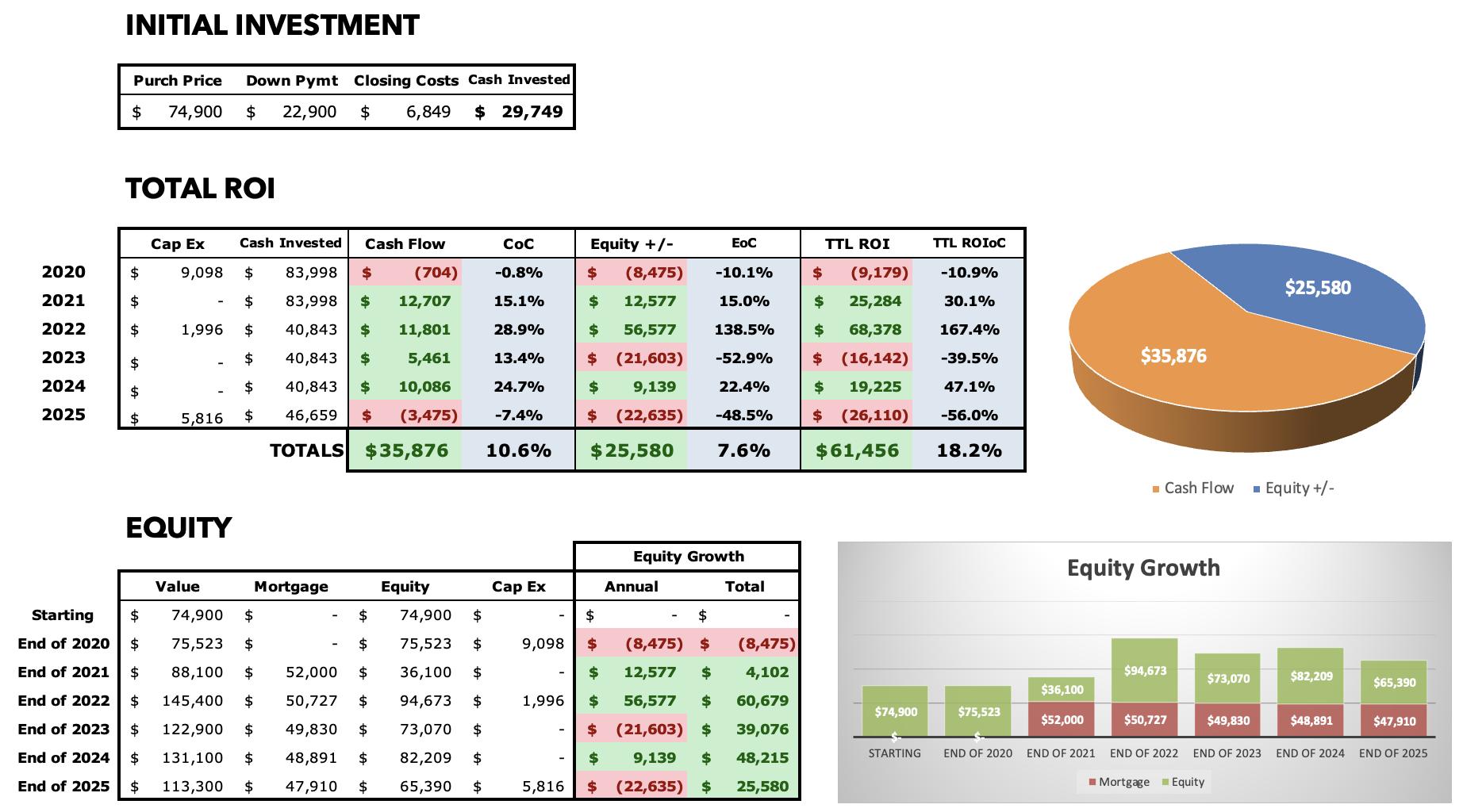

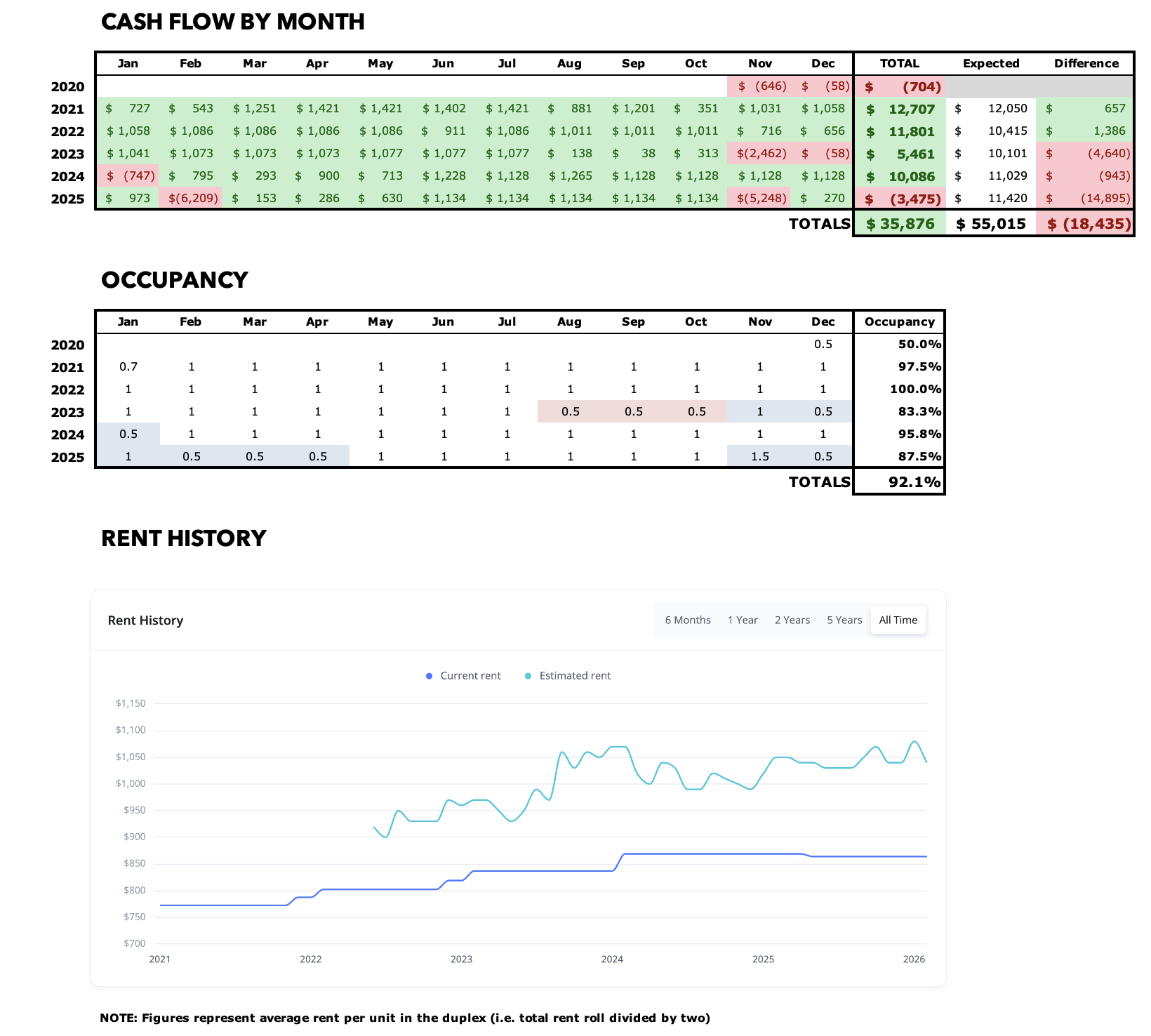

Annual Updates

For all Property Spotlights, I come back at the end of each year to provide a brief narrative of what happened at the property that year. I also update my annual and cumulative figures for the property, including cash flow, equity growth, and occupancy.

2021

Coming into 2021, I had completed the initial rehab on the one side of the duplex that needed it, and as of late January, a new tenant was in place. The property became the cash cow that I expected it would, even after I did a cash-out refi (my first BRRRR) in August. According to my pro forma model, it’s now expected to generate about $1K per month in cash flow, or nearly 25% of my $40K invested each year, easily the highest rate of return in my portfolio. And 2021 did not disappoint: the duplex generated $12.7K, exceeding my target by over $650.

2022

The duplex was fully stabilized in 2022: the rehab and the cashout refi were complete, and it was fully occupied all year. I had only a few maintenance visits totaling $605; this combined with full occupancy allowed me to beat my cash flow target by nearly $1400. The tenants have both renewed with small increases at the end of the year, so 2023 should look much the same (fingers crossed). On the CapEx side, I replaced an HVAC condenser for $2K this year. Finally, there was a huge increase in the Zestimate on this property, which now more accurately reflects the true resale value of the duplex — and you see a huge jump in equity as a result.

2023

Well, crossing my fingers apparently didn’t work: I had to do an eviction/turn at the end of this year on one side of the duplex, which hurt my cash flow results. I still cash flowed positively, though, which is one of the nice things about duplexes — one side can make up for the other side during vacancies. A new tenant is in place as of February 2024, so I hope to keep this full for the rest of the year.

The only maintenance costs I had were associated with the turn.

Strangely, the Zestimate dropped quite a bit this year after a huge increase last year; who knows, maybe they have trouble valuing duplexes.

2024

The duplex was occupied all year with no issues. A plumbing leak from an upstairs bathroom cost nearly $1K all in to repair; that, combined with some other minor maintenance and some residual turn costs in January, left me short of my cash flow target. But the property still cleared over $10K in cash flow for the year, so…not complaining.

2025

This was the most eventful year ever at this duplex, and not in a good way. I had to turn BOTH sides of the duplex, leading to over $13K in turn costs and another $6K in CapEx to replace countertops & doors in one turn, plus the electric meter box (which serves both units). One side of the duplex had never been turned before, so an expensive “first turn” with some CapEx was not surprising; however, the other side had been turned twice before, and STILL cost me $6K due to the tenant’s poor upkeep of the property. Disappointing. All this led to my first negative annual cash flow at this property, missing my target by a whopping $15K.

Stable occupancy has also showing up as a bit of a persistent challenge; 4 turns in 5 full years is a lot. Plus, I was not able to raise rents at all when I placed new tenants this year.

Zillow’s valuation for this property continues to gyrate wildly; in fact, I’m quite sure this property is worth ~$145K, much higher than the current valuation indicates. But I promised to simply use Zestimates for this purpose, and not introduce my own bias, so I’ll stick with that.

About the Author

Hi, I’m Eric! I used cash-flowing rental properties to leave my corporate career at age 39. I started Rental Income Advisors in 2020 to help other people achieve their own goals through real estate investing.

My blog focuses on learning & education for new investors, and I make numerous tools & resources available for free, including my industry-leading Rental Property Analyzer.

I also now serve as a coach to dozens of private clients starting their own journeys investing in rental properties, and have helped my clients buy millions of dollars (and counting) in real estate. To chat with me about coaching, schedule a free initial consultation.