Memphis Rental Property #20

Last updated: 2026

NOTE: All figures and statements in this article were accurate as of the time of initial publication in 2022. Check out the Annual Updates section at the bottom of the post to see how the property has performed since then.

Last month, I closed on my 20th rental property in Memphis, and my first one in over a year and a half. This is the first of four new properties that I have purchased as part of a 1031 exchange, in which I sold my last remaining rental condo in New York City. (The 1031 exchange allows me to trade that property for other(s), without being subject to capital gains tax or depreciation recapture tax. I will write in more detail about each of the new properties, and the 1031 exchange, in upcoming articles.)

I used a mortgage to buy three out of the four new properties, but this one I purchased outright with cash. This has to do with the specific financials of my 1031 exchange: in order to get the maximum tax benefit, I have to exhaust all the proceeds of the sale of my condo, and in order to do that, I had to use less overall leverage than I would have otherwise used.

Let’s get into the details of this deal!

Property #20: The Deal

This house was listed publicly on the MLS, so I found it on Zillow. It’s a small but functional 3 bed, 1 bath home in a C+/B- area, not far from several of my other properties. It’s part of a small neighborhood that was built in 1999 with about 50 largely identical starter homes. It’s rare to find a small 3/1 like this that was built so recently, which is one of the things I liked about the property.

It looked to be in decent condition based on the photos, and was being offered vacant with an asking price of $92,000. I estimated the market rent at ~$1,100. (In addition to looking at current comp properties being offered for rent, I also used algorithmic rent estimators, of which RentCast is the best.) Based on this strong rent-to-price ratio, and on recent sales comps in the area, I felt the asking price was on the low side. So I decided to submit a strong cash offer at $99,000, seven thousand above the asking price.

My offer was accepted, so I moved into the due diligence phase.

Property #20: Due Diligence

Because the property was vacant, I didn’t have any tenant due diligence to worry about. But I still wanted to learn everything I could about the house itself. So I asked for the home’s maintenance history, and the scopes of work for any rehabs performed on the property. The seller responded with the following:

Floors were replaced in 2019 - Luxury Vinyl Plank Flooring

All Blinds were replaced by our hired handyman last week before the house was listed.

Handyman also changed: Bedroom Door Knobs, Programmed Garage Door Button, Fixed Globe in Garage, Spot painted House

Professional Deep Clean of Home

This all sounded like pretty good news, and the listing photos seemed to corroborate the information they provided.

From there, I ordered a home inspection. But before the inspection could even be completed, something strange happened: the seller told me they were going to put a new roof on the house. I got this email from my broker:

“We just received an update and as per the listing agent, throughout this process, the seller was looking into replacing the roof, as it was reaching the end of its life. Seller has decided to move forward with the replacement and install a brand new roof. They will be reaching out to the roofing company to see what their process is and will keep us updated. Also, The Seller has advised that she will not be completing any other repairs, updates or adjustments after the roof replacement. Please let me know how you would like to proceed. Thank you!”

This is very unusual indeed — so much so that I became suspicious. A seller will not normally incur a major expense like a roof after going into contract unless they absolutely have to. Why would they give me the free bonus of a brand new roof? My only guess was that the roof was bad enough that the seller was worried I would pull out after I saw the inspection report, or at minimum demand a new roof post-inspection. Perhaps she was just trying to avoid that situation, and also preempt any other requested repairs or negotiations after the inspection.

When I got the inspection back, it did show that the roof was pretty old — it was probably the original roof from 1999 — and there was evidence of some old leaks inside the house, though none of them appeared to be active leaks. Nothing that would have scared me away from the deal, though, so I’m still not entirely sure why the seller decided to replace the roof. Worked out well for me, of course!

The inspection did turn up a few other issues of concern, however, which I summarized this way when I asked for a further price reduction to $87,000:

The dryer vent pipe in the garage, which terminates in the attic, is improperly installed and a safety hazard. I will need to re-do this so that it safely vents outside the home. Cost: ~$2K.

The furnace and water heater are both well past their design life, and I will need to replace both right away before renting the home. Cost: ~$5K

The enormous tree in the backyard is a danger to the home, and I will need to remove it immediately. Cost: ~$5K

After a few back-and-forths, we settled on a final sales price of $93,000, and proceeded to closing.

Property #20: The Rehab

Despite the home being in pretty good shape, I did do a small rehab to bring a few things up to standard, including a fresh coat of paint, removal of some bushes in front of the home, repairing the yard fence, and some other miscellaneous work.

As for the issues I used to negotiate the price down, here’s how I handled those:

The dryer vent pipe was redundant — there was a dryer vent installed in the kitchen when the home was built, but apparently the previous owner wanted to do laundry in the garage, so they rigged up this vent pipe and vented it to the attic. Rather than vent this to the roof, I simply removed the hook-up altogether, which was a much cheaper solution.

I did replace the furnace and water heater, but the cost of this was only ~$3,500, less than I had budgeted.

As for the big tree, upon closer inspection with my property manager, we decided only to remove one of the large limbs of the tree that overhangs the house, rather than taking down the entire tree. This addressed all of the serious risk at a much lower cost (under $1,000).

If you like, you can examine the full scope of work in a new tab.

Within a few weeks of the work being completed, my property manager had signed a lease with a new tenant paying $1,095 per month, achieving the rent potential I had targeted. The new tenant will move in at the end of November.

Here are a few of the completion photos showing what the house looked like for the new tenant:

Property #20: The Financials

This was a cash purchase, so I invested the full $93K into the deal, plus my closing costs ($1,674 — very low because there was no loan) and my rehab costs ($7,248), for a total of $101,922 invested. I used the RIA Property Analyzer to run the final numbers on this property – here are the key metrics that the analyzer calculated for me:

Purchase Price: $93,000

Monthly Rent: $1,095

Monthly Cash Flow: $723

Cap Rate: 9.34%

Cash on Cash Returns: 8.52%

Total Returns w/ 2% Appreciation: 10.34%

(Want to use this calculator yourself? You can!)

OR

Using the multi-year model in the RIA Property Analyzer, we can visualize some of the main long-term trends assuming a long-term inflation rate of 2%. Some of these trends are noticeably different from other Property Spotlights due to the fact that there is no mortgage on this property:

Cash flow increases over time. Both rent and expenses are projected to increase with inflation, but the gap between the two still grows each year:

Cash Flow Year 1: $8,684

Cash Flow Year 10: $10,378

Cash Flow Year 25: $13,967

Without leverage, total returns are lower, but the vast majority of the returns are in the form of cash flow. The only other form of returns are appreciation, which are a much smaller portion:

Appreciation Year 1: $1,860

Appreciation Year 10: $2,223

Appreciation Year 25: $2,992

Total returns on cash increases over time. This is a consequence of the first two points – I will make greater total returns over time on the same initial investment of cash. But total returns on equity remains flat.

Total Returns on Cash Year 1: 10.3%

Total Returns on Cash Year 10: 12.4%

Total Returns on Cash Year 25: 16.6%

Overall, I’m really pleased with this property. It has a strong price to rent ratio, it’s in great shape (including a new roof, furnace, and water heater), and I think it’s attractive to renters. If mortgage rates come back down in the future, it will be very tempting to do a refinance and pull some cash out — but if not, the strong monthly cash flow here is also very nice.

After all, my goal with the 1031 exchange was to redeploy the equity in my NYC condo (which did not cash flow) into properties that would cash flow strongly and add to the monthly expected profits in my rental portfolio — and the $700/month cash flow here certainly meets that goal. (And there are three more new properties still to come as part of that 1031 exchange…)

Property #20: The Deal Sheet

Finally, to sum up Property #20 and its financials, here’s the full “deal sheet”:

Looking for YOUR Next Property?

If you need help finding, analyzing, and purchasing YOUR next property — or your first one! — schedule a free initial consultation with me. I’ve helped dozens of private coaching clients invest with confidence and build cash-flowing rental portfolios of their own.

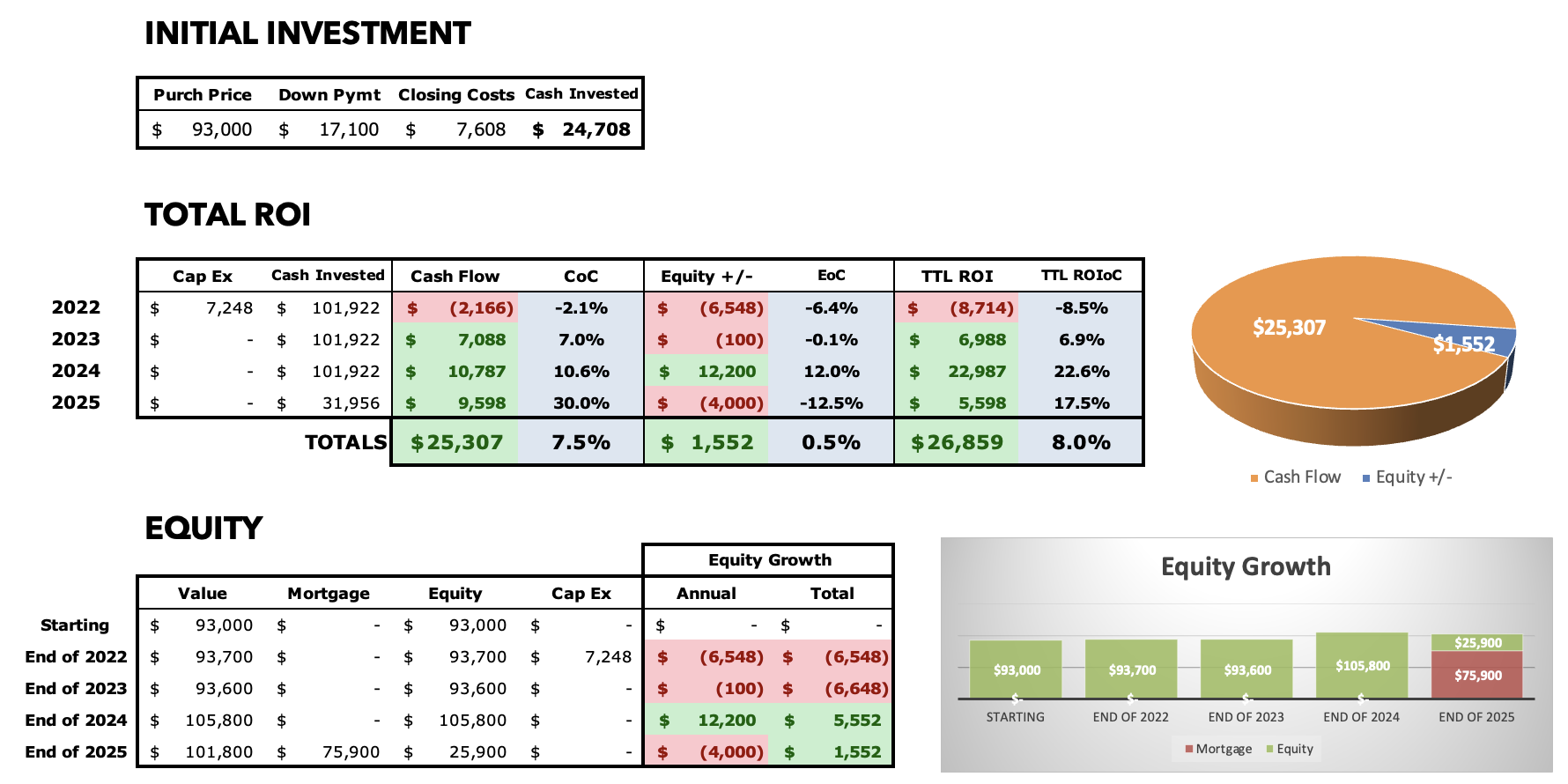

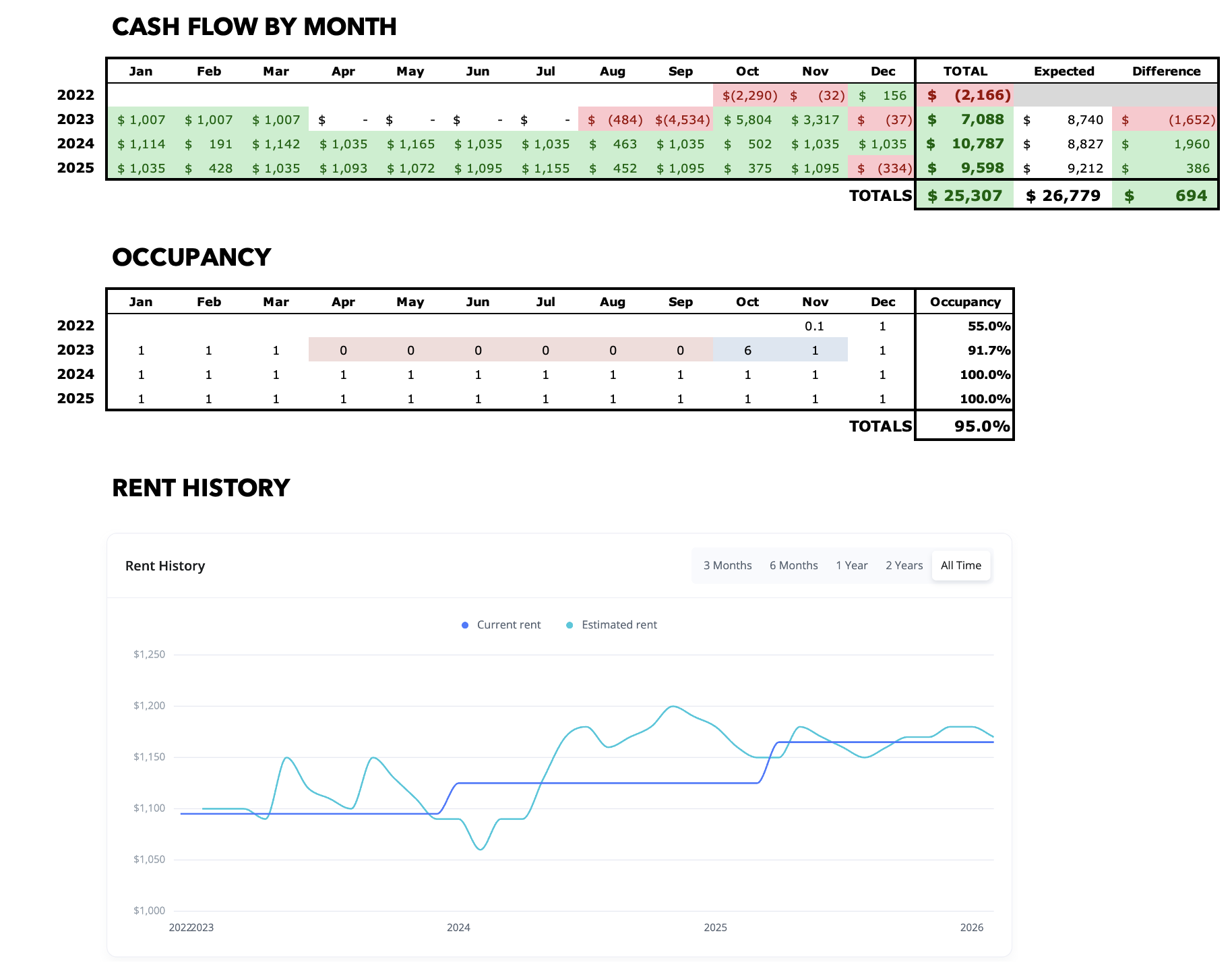

Annual Updates

For all Property Spotlights, I come back at the end of each year to provide a brief narrative of what happened at the property that year. I also update my annual and cumulative figures for the property, including cash flow, equity growth, and occupancy.

2023

It was a rocky and unusual first year at this property. Just a few months after my new tenant was placed, they stopped paying rent and entered eviction proceedings. They then declared bankruptcy, which significantly slows down evictions. In the end, the eviction took the better part of the year: rent payment stopped as of April, we didn’t get possession of the house until September, and it was December before the new tenant moved in.

The saving grace was that, due to the horrendous tenant placement, my PM agreed to reimburse me for lost rent during the vacancy, and reimburse some of the costs of the rent-ready work. This salvaged the year for this property. A brand new tenant is in place for 2024 paying $1,125/mo., so hoping for a much smoother year…

2024

Fortunately, it WAS a much smoother year here. My new tenant pays (mostly) on time, and there was $0 of maintenance or CapEx all year, causing me to exceed my cash flow target by nearly $2K. The tenant’s renewal is up at the end of March 2025, when I plan for a small increase.

2025

My tenant signed on for another year with a small increase to $1,165/mo. This is quite close to market rent. For the second straight year, there was $0 of maintenance or CapEx, leading to strong cash flow of over $9K.

I did elect to take out a loan against this property toward the end of 2025, cashing out $75,900. This leaves me with just over $30K invested into the property between my down payment, closing costs, and CapEx. Naturally, my nominal cash flow will be much lower in future years, but I still expect over $3K in annual cash flow going forward.

About the Author

Hi, I’m Eric! I used cash-flowing rental properties to leave my corporate career at age 39. I started Rental Income Advisors in 2020 to help other people achieve their own goals through real estate investing.

My blog focuses on learning & education for new investors, and I make numerous tools & resources available for free, including my industry-leading Rental Property Analyzer.

I also now serve as a coach to dozens of private clients starting their own journeys investing in rental properties, and have helped my clients buy millions of dollars (and counting) in real estate. To chat with me about coaching, schedule a free initial consultation.