Review of a Rent-to-Retirement Pro Forma: What the Numbers REALLY Show

If you’ve ever shopped for turnkey properties, you’ve probably looked at pro formas published by turnkey providers. (A “pro forma” in this context is just a set of financial projections for the property.) On paper, these always tend to look like really solid investments: positive cash flow, a respectable cap rate, and returns that would be attractive to just about any investor — especially someone looking to buy their first out-of-state rental.

But there can be assumptions hidden in the pro forma that significantly impact the returns, and might make the deal look better than it actually is. That’s why I always tell my private coaching clients that they MUST run their own numbers, even if a pro forma has been provided to them.

Here’s a great example of this: I often examine deals from various providers to keep my finger on the pulse of the market, particularly in areas where I invest or work with clients the most. I opened an email from Rent to Retirement the other day, and saw a deal for a new construction property (aka build-to-rent) in Memphis, my primary investment market where I own 25 rental properties. So I decided to take a closer look, and see if I would run the numbers the same way they did. (Spoiler alert: there were some differences, to say the least!)

In this article, I’m going to walk through this actual deal from Rent to Retirement and break down exactly how the pro forma is put together, line by line, in the hopes of answering a key question:

Do these numbers actually hold up in the real world?

To answer that question, I’m going to walk through:

The original pro forma (as presented)

Each key assumption

What I believe is realistic, based on my own experience and that of my investor clients

How the returns change when adjusted

If you’re evaluating turnkey rentals, this is exactly the kind of analysis you need to be doing before closing on a deal to be sure that your ROI expectations are realistic. Because no matter who you’re buying from, you should know how to spot the common ways that turnkey pro formas can be “massaged” in order to make the returns looks as attractive as possible.

The Original Pro Forma

First, a bit of context: Rent to Retirement operates as a turnkey investment platform, partnering with local builders, operators, and property managers to deliver fully packaged rental property deals to investors. While this model offers convenience and access to multiple markets, it also means the entity presenting the deal is not always the one executing it on the ground.

Still, this “turnkey broker” model is quite common, and Rent to Retirement is among the best-known in the space. They also publish abundant educational content on their website and on their podcast, as well as in their paid academy. For the most part, they have earned a good reputation and are well-regarded in the industry. So this is not a critique of them specifically; rather, it’s an example of how ALL turnkey pro formas need to be carefully scrutinized to be sure you understand and agree with the underlying assumptions.

The deal we’ll be looking at is a 2025 new build — a 4-bed, 2-bath model that is very similar to many new construction homes I’ve seen in the Memphis market over the past five years. They’re really nice homes (in fact, I really wanted to buy one of them myself several years ago, but ended up getting this turnkey property instead.)

The original pro forma was published here, but note this link may not be active once the property is sold. Here is what the house looks like — it’s kind of a stunner, I have to say:

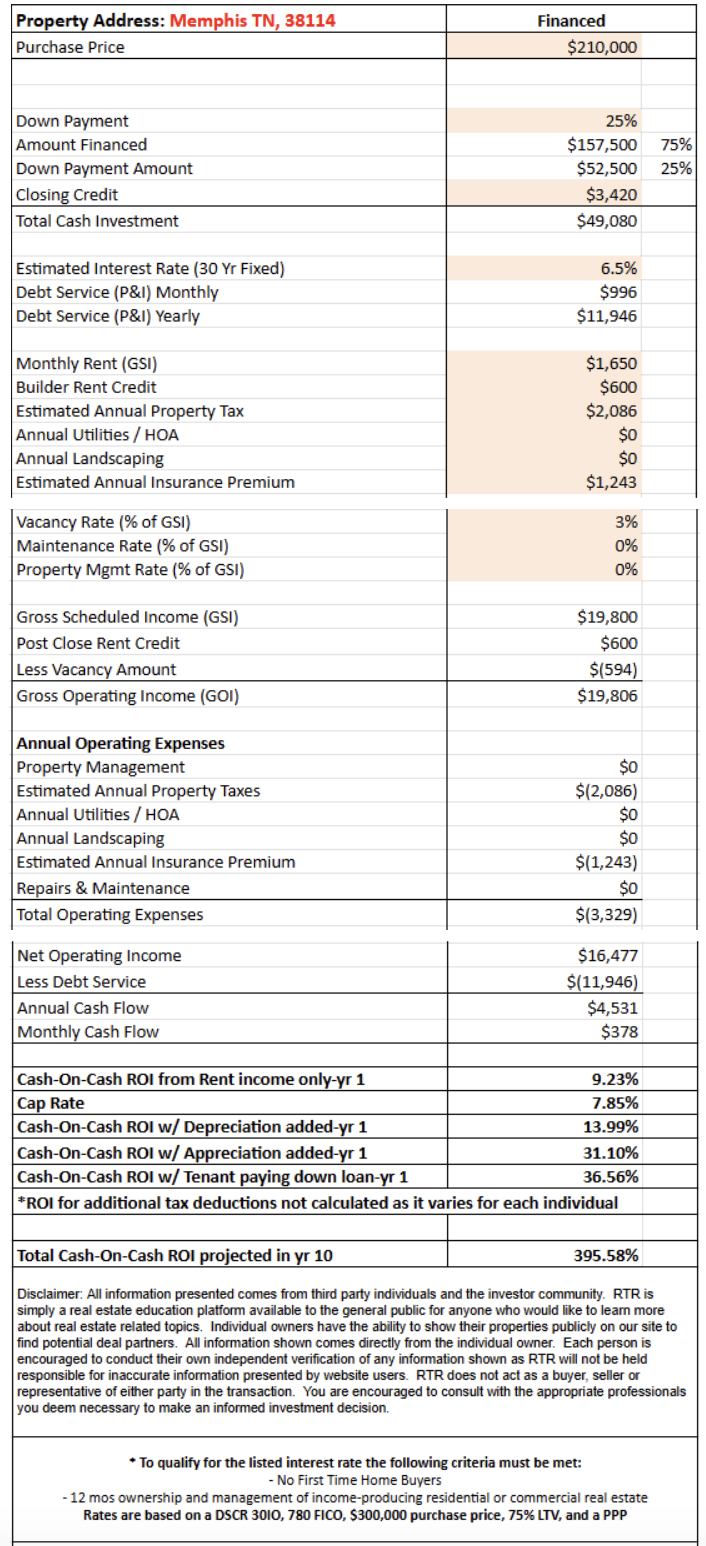

The published pro forma has the following highlights:

$210,000 purchase price

75% LTV at 6.5%

$1,650 monthly rent

9.2% Cash-on-Cash

Here are the rest of the details:

Common Ways Rental Pro Formas Overstate Returns

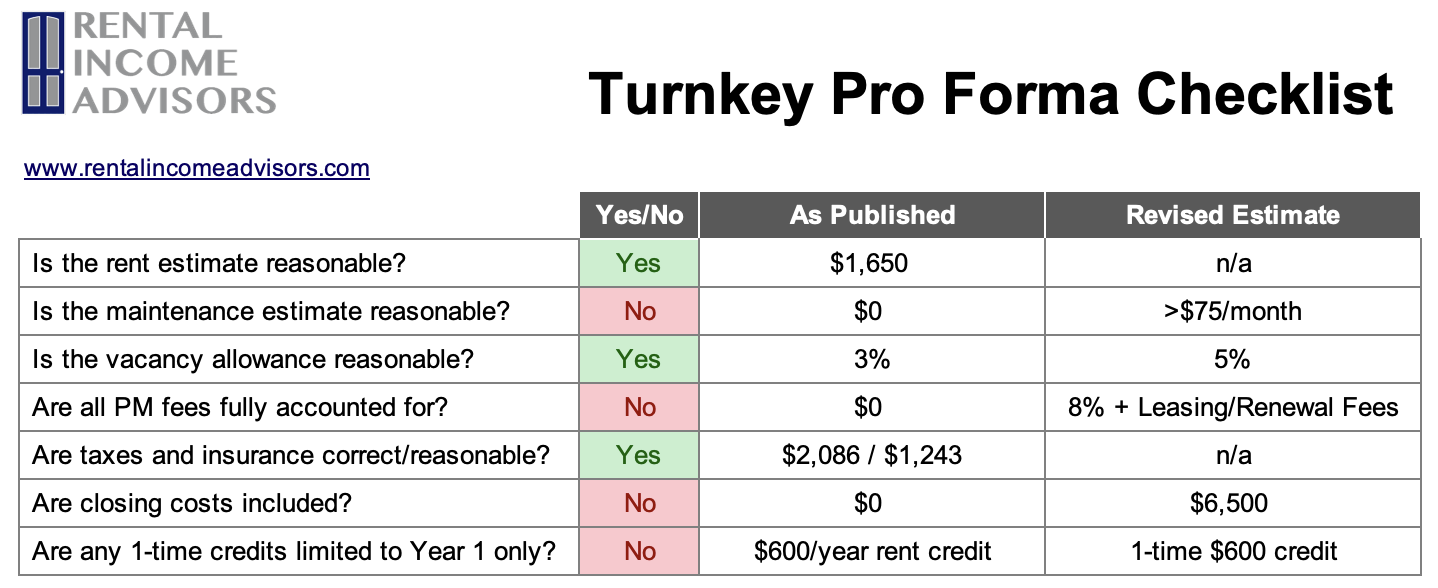

I’ve analyzed thousand of rental deals over the years, and there are several common ways that published pro formas can be “tweaked” in order to produce more favorable returns:

Overestimating rent

Underestimated maintenance

Unrealistic (or missing) vacancy

Failure to account for PM fees

Taxes/insurance not fully loaded

Omitting closing costs

Annualizing credits or benefits that apply only to Year 1

Let’s take a look at each of these areas in detail and see how the Rent to Retirement pro forma holds up. At the end, I’ll compare the published ROI numbers, including cash-on-cash returns, to the ones I would calculate for the same property.

1. Rent Assumptions

The rent here is listed at $1,650/mo. While I don’t have the exact address, I know it’s possible for a new construction 4 bed/2 bath to fetch that amount in this zip code. Also, they advertise that a tenant is already in place, so I think it’s fair to assume that the pro forma is built with the actual rent of that tenant (though of course I would confirm this if I were looking to buy this house!)

So far, so good, then — the rent estimate seems accurate and reasonable. But this is a big area that you want to double-check for reasonableness on all pro formas by doing your own rent estimate, checking algorithmic estimators (i.e. RentCast), etc. — even $100 of difference in rent can make a huge difference in your ROI numbers.

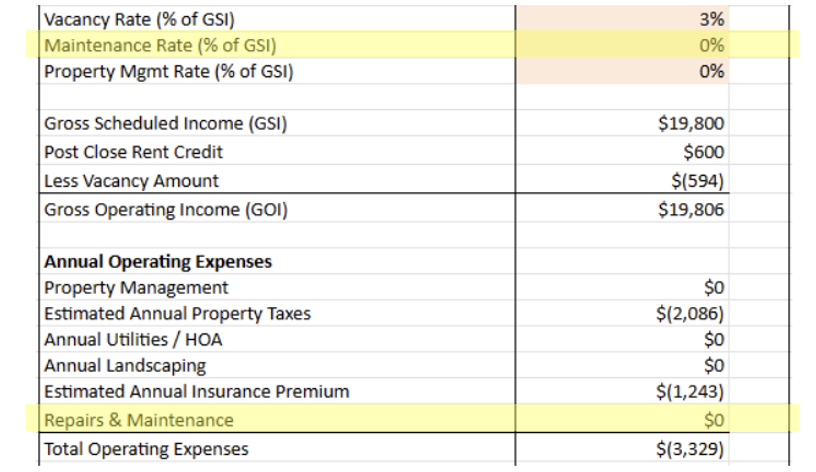

2. Maintenance Estimates

If you look closely at the Rent to Retirement pro forma, it shows that they are not building in any ongoing maintenance & repair costs:

It’s true that turnkey properties should have lower maintenance & repair costs than a typical property — in fact, I’ve shown previously that this is true in my own portfolio.

It’s also true that some builders and turnkey providers will provide a warranty that guarantees $0 maintenance costs to the owner in the first year. This is great to have, of course — but it only applies for the first year, not the life of the investment. (This is a specific example of a trick that we’ll cover in #7: annualizing one-time benefits.)

By building a pro forma that assumes $0 in maintenance costs, they are significantly underestimating what it will cost an investor to maintain the property over time. Even brand new properties will require maintenance. For reference, I currently spend $125/mo. per property on maintenance & repairs. While it’s reasonable to assume lower-than-average costs on a property like this, I think anything less than $75/mo. is overly optimistic.

Caveat: you might counter by saying, “Well, this is a pro forma for Year 1, so strictly speaking, it’s correct to exclude maintenance costs.” This is true, but amounts to winning on a technicality. Remember that the entire point of a pro forma is to estimate the financial potential of an investment property over time. So even if I were receiving these Year 1 incentives as part of a deal, I would personally NOT build them into my numbers. (And in fact, it’s reasonable to wonder if these “Year 1” incentives are offered precisely so that more attractive pro formas can be built and marketed.)

3. Vacancy Allowance

Some percentage of the time, you won’t collect rent on a property — either because the house is vacant, or because the tenant in place isn’t paying. Most pro formas use a vacancy allowance of 4-5%, but Rent to Retirement uses a slightly lower assumption of 3%.

Personally, I always use 5% in my estimates, despite the fact that the vacancy I’ve measured in my own portfolio is closer to 3%. (You can see my actual vacancy figures, and more, on my portfolio reports page.)

So I’m going to adjust this up to 5% in my revised estimate, because that’s what I always use in my models — though I’d still judge RTR’s estimate to be reasonable based on my portfolio’s vacancy rate over the years.

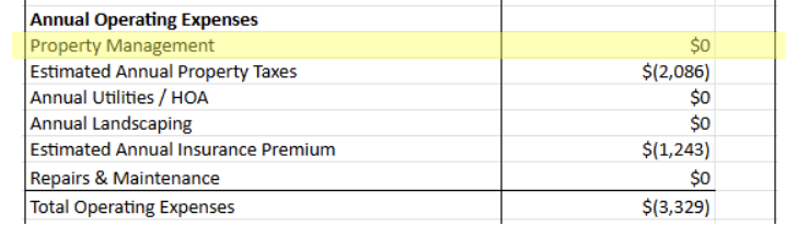

4. Property Management Fees

Here again, we see $0 of property management fees built into this pro forma:

As part of this deal, they are offering a promotion wherein the buyer would pay $0 in PM fees for the first year. But like we saw with maintenance costs, we can’t annualize this Year-1 benefit as if it applies for the life of the investment — because it won’t. Typical PM fees in Memphis are 8% of rent collected, so I’ll build that in to my numbers.

But there’s another category of fee that is almost ALWAYS ignored in rental pro formas: leasing and renewal fees. Leasing fees are charged whenever a new tenant is placed, and renewal fees are charged when a tenant renews onto a new lease. In Memphis, most PM’s leasing fees are 50% of one month’s rent ($825 in this case) and renewal fees are a flat $250. The investor will almost always pay one of these two fees every year, depending on the tenant. So I’ll build in $450 of average annual liability into my revised estimate, which assumes that tenants will stay an average of about 3 years.

5. Property Taxes and Insurance

You always want to be sure that property taxes are correct, and the insurance estimate is reasonable for the market. In this case, they are. While I don’t have the address to double-check, both the propery tax and insurance estimates used here are perfectly reasonable for this property.

(One trick to watch out for: in many markets, property taxes can jump significantly after a property is rehabbed and sold at a much higher valuation. If this is a factor in your market, you want to build in a property tax estimate that reflects what the tax burden is likely to be AFTER they increase. Some turnkey providers will use the “old” tax amounts in their pro formas, instead of estimating the likely new amounts.)

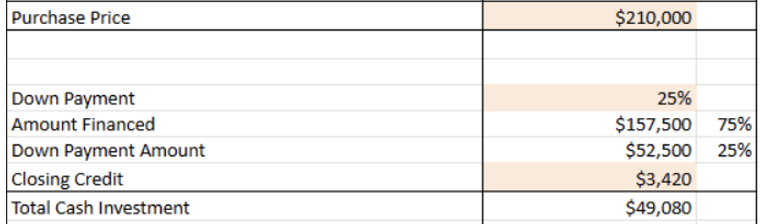

6. Closing Costs

Some pro formas will calculate your cash invested into a deal by simply by multiplying the purchase price by the down payment percentage (less any credits.) That’s exactly what we see in the Rent to Retirement pro forma:

It’s perfectly fine for that credit to be subtracted from your dollars invested. But they’re leaving out closing costs, which typically amount to ~$6K-$7K on a deal like this. Approximately 70% of those fees are related to the loan; the rest are government fees, title fees, etc.

While those loan costs can vary between lenders, I’ve seen hundreds of deals in Memphis, and $6K-$7K is a very good estimate — so I’m going to build that into my numbers.

7. Annualizing One-Time Credits

This is one of the toughest things to catch in a published pro forma. We’ve already seen a few examples of it: both the “$0 PM fees for Year 1” and the “$0 in maintenance for Year 1” were included in the published pro forma, which could potentially cause an inexperienced investor to think those incentives are a permanent part of the ROI picture for the investment, when of course they’re not.

But there’s actually another example of this in the Rent to Retirement pro forma, and it has to do with the $600 “builder rent credit:”

In this case, the $600 credit is used in the calculation of Gross Operating Income, from which all the downstream ROI calculations flow. It is added to the rent income (19,800 = $1,650 × 12 months), fully negating the vacancy allowance.

Again, while this is strictly correct for the purposes of calculating Year 1 returns, and while they do take some care to specify “yr 1” at the bottom of the pro forma, I still think it has the potential to confuse some investors. Plus, it would be more appropriate to add this $600 credit to the $3,420 closing credit already discussed above, rather than adding it to income. (But adding it to income has a greater positive impact on the ROI numbers, so they might be more inclined to put it there.)

Following the same logic as with the other Year 1 incentives, I will back this out of my own pro forma numbers.

Here’s the summary of these 7 “areas of inquiry” into this pro forma — some looked great, while others needed important adjustments:

Comparing the Final Numbers

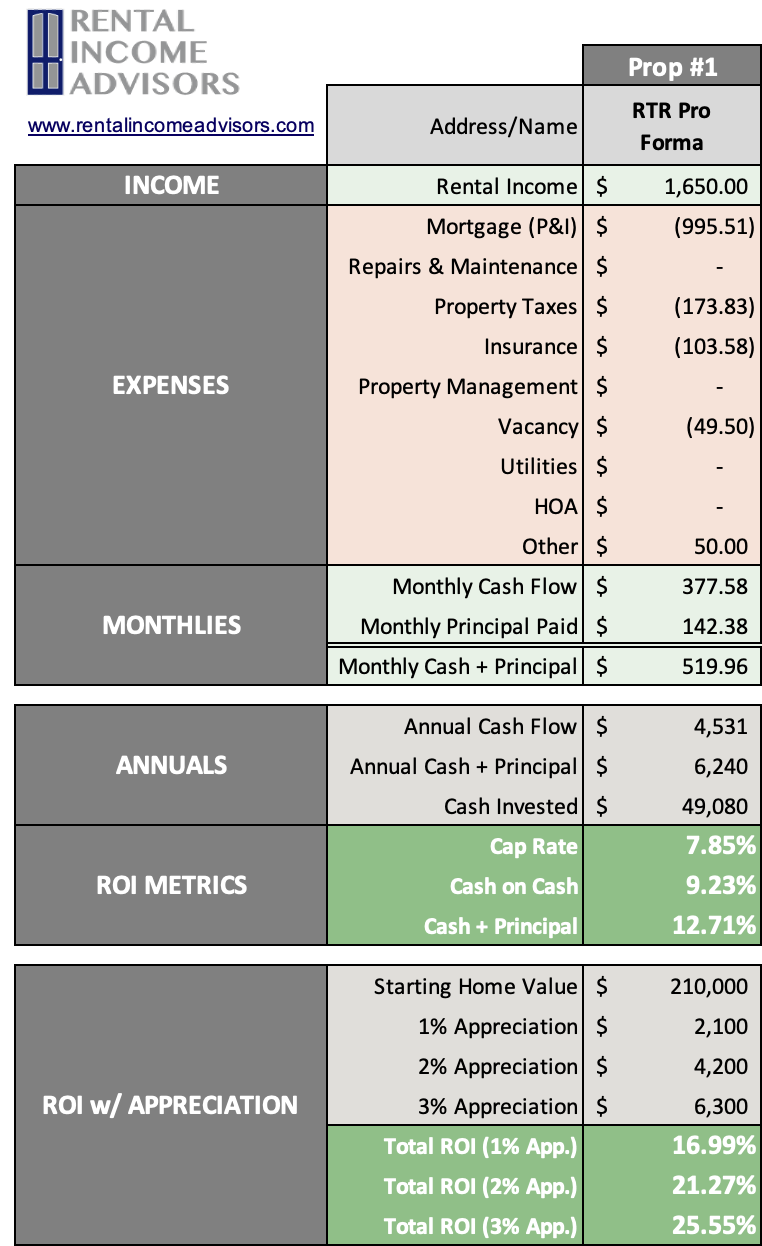

I replicated the Rent to Retirement inputs in my Analyzer, and was able to re-create the same ROI metrics ($378 in monthly cash flow, 7.85% cap rate, 9.23% cash-on-cash) that were published in the original Rent to Retirement pro forma:

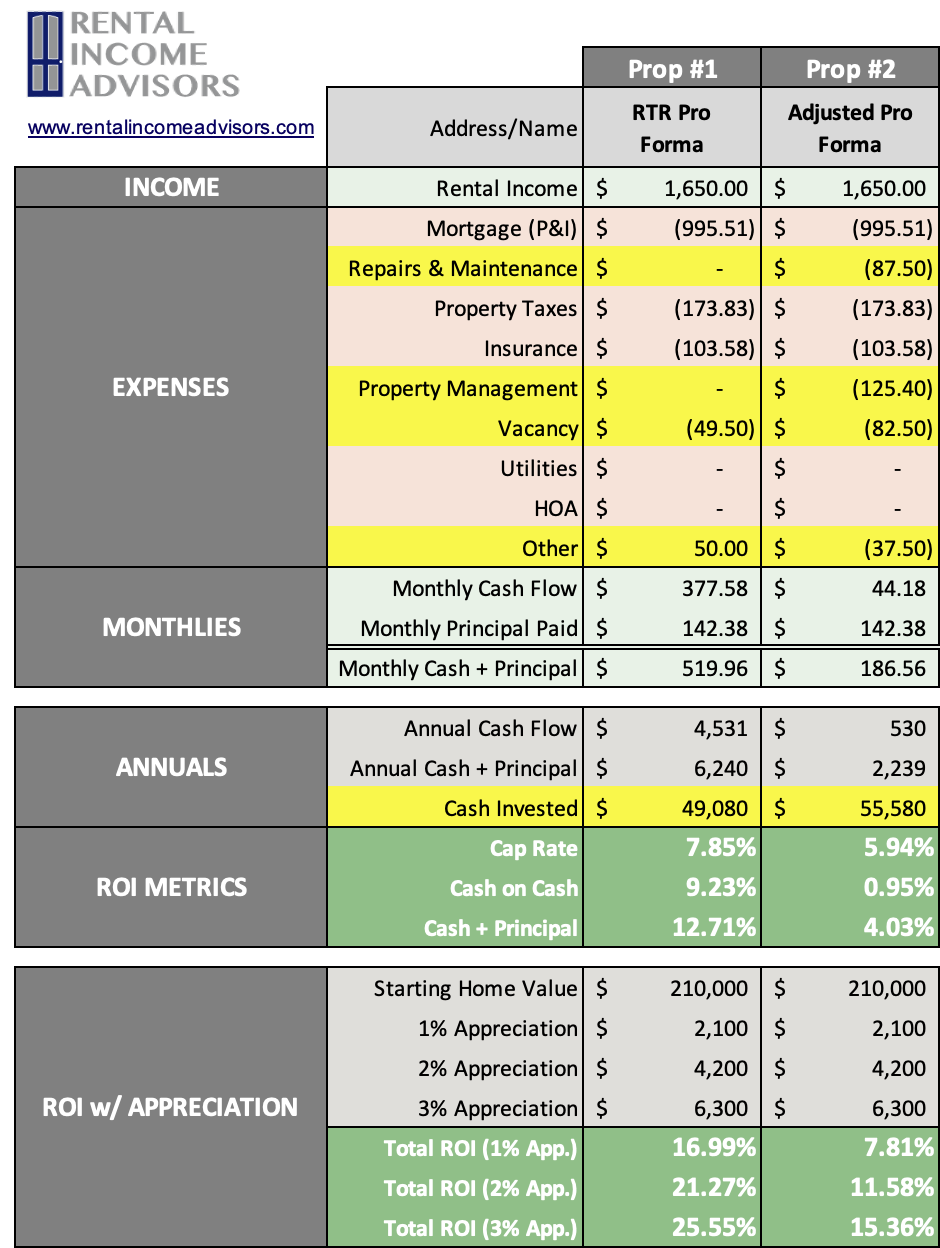

However, when I make all the adjustments I described above, the numbers look quite a bit different. I’ve highlighted in yellow the rows where there are changes to make it clear where the numbers differ:

In the end, my numbers tell a very different story than the original pro forma. With these changes to the underlying assumptions, I would expect very minimal cash flow ($44 per month, and less than 1% cash-on-cash). Instead of being a solid cash flow play, in reality this property is basically cash flow neutral.

Now, this could still be a great long-term investment, and we always expect somewhat lower rates of return with high-quality build-to-rent properties. So for the right investor, this could still be a great deal.

But if you’re looking at a turnkey deal like this, you should go in “eyes wide open” with realistic expectations about your cash returns — and that means taking a very close look at the assumptions in the published pro forma to be sure you agree with them.

Need help analyzing YOUR next deal?

If you’re evaluating deals like this and want a second set of eyes before making a decision, this is exactly what I help investors do — as well as helping them with market selection, buy box criteria, and more. Learn more about how my private coaching works here.

Conclusion

Turnkey and build-to-rent can be great investing models for new remote landlords, especially those who prefer a low-risk, hassle-free investment style.

However, when any provider publishes a pro forma modeling the returns of that property, smart investors should scrutinize it carefully to be sure they agree with the underlying assumptions — because those assumptions can significantly shape the outcome and the ROI numbers.

Specifically, you should ask yourself these seven questions when evaluating a published pro forma for a rental property:

Is the rent estimate reasonable?

Is the maintenance estimate reasonable?

Is the vacancy allowance reasonable?

Are all PM fees fully accounted for?

Are taxes and insurance correct/reasonable?

Are closing costs included?

Are 1-time credits limited to Year 1 only (not annualized)?

About the Author

Hi, I’m Eric! I used cash-flowing rental properties to leave my corporate career at age 39. I started Rental Income Advisors in 2020 to help other people achieve their own goals through real estate investing.

My blog focuses on learning & education for new investors, and I make numerous tools & resources available for free, including my industry-leading Rental Property Analyzer.

I also now serve as a coach to dozens of private clients starting their own journeys investing in rental properties, and have helped my clients buy millions of dollars (and counting) in real estate. To chat with me about coaching, schedule a free initial consultation.