How to Analyze a Rental Property: Estimating Expenses

Last updated: 2026

Note: This is the second part of a two-part series. Here is Part 1.

In Part 1 of this series, we discussed the various methods you can use to arrive at the expected rental income on a target property you’re analyzing. In Part 2, I’ll step through how to properly estimate all your expenses, and then pull it all together in the RIA Property Analyzer to determine if your target property is a good deal that meets your investment goals.

If you haven’t done so already, you can download the RIA Property Analyzer for free, and follow along with this example as we go.

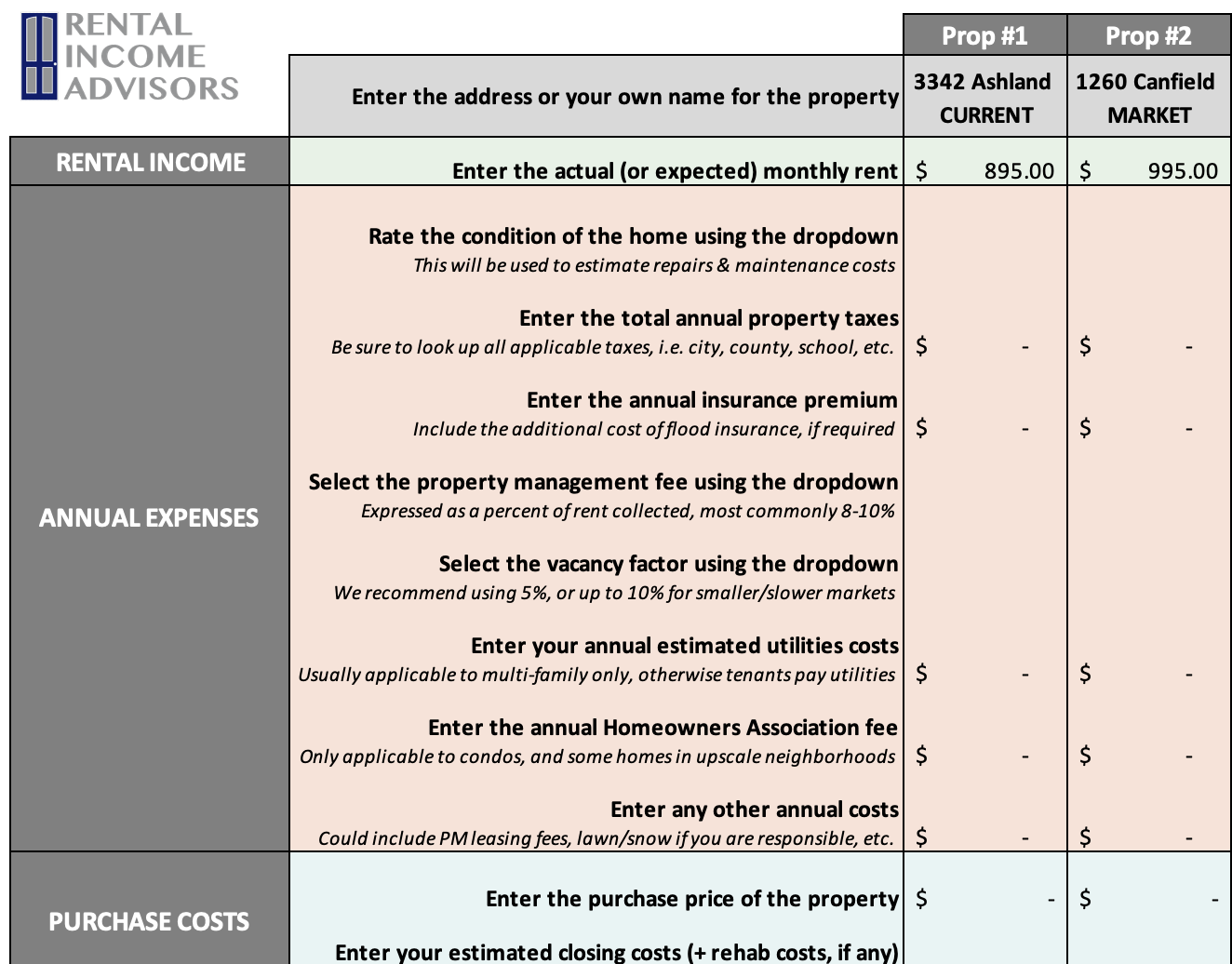

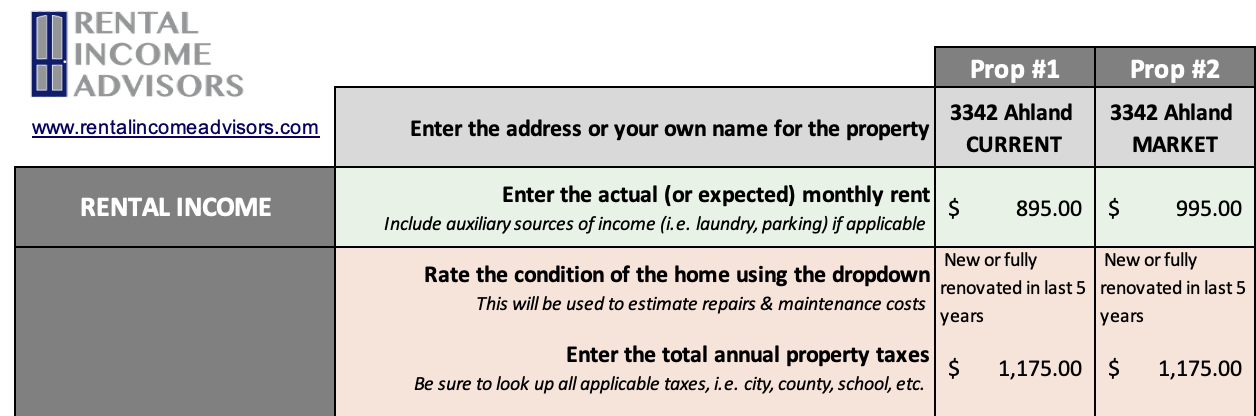

First a quick recap of Part 1: we were analyzing this property, which was tenant-occupied at $895. However, using various methods, we determined that the market rent might actually be somewhat higher at around $995.

When we left off, I had set up the RIA Property Analyzer with two columns, one to analyze the property assuming the current rent of $895, and another to run the numbers with the higher market rent of $995 – here’s what it looked like:

Now we’ll dive into the expense side of the equation, handling them in this order:

Repairs & Maintenance

Property Taxes

Insurance

Property Management

Vacancy

Utilities

HOA

Other Costs

Purchase Costs

Mortgage

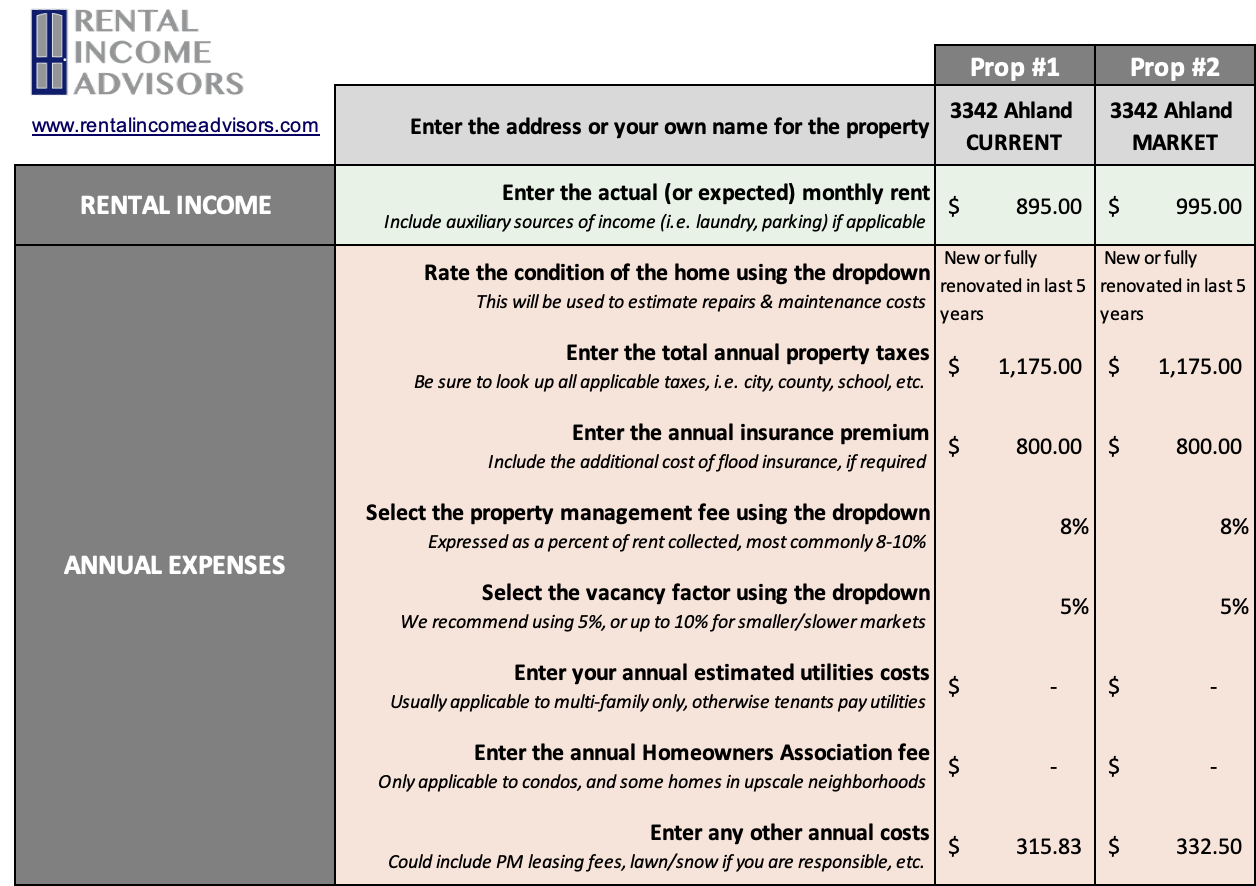

1 Repairs & Maintenance

The toilet won’t flush. The air conditioning goes out. The lock on the front door breaks. There are any number of things that will need to be fixed in your rental property, so you’ll need to budget for those costs.

Investors usually establish this budget either as a percentage of rent collected (say, 10%) or as an annual percentage of the price of the home (say, 1%). I use the latter method. But it’s also reasonable to expect newer or more recently renovated homes to incur lower maintenance costs than ones that are older and need lots of work. To account for that, I built a sliding scale calculation into the RIA Property Analyzer based on the condition of the home, as follows:

New or fully renovated recently = 0.5% of home price per year

Good condition, but not recently renovated = 1.0% of home price per year

OK, but needs some updating = 1.5% of home price per year

Needs a lot of work = 2.0% of home price per year

You can assess the condition of a home based on the pictures and the language used in the listing. The second option (“good condition”) is a reasonable estimate for most rental homes, or if the condition of the home is difficult to ascertain from the listing. But if both the interior and exterior look sparkling, and the listing mentions that it has been recently renovated, you can select the first option. If the home looks pretty old and not updated on the inside, or if the listing mentions things like “needs some TLC” or “sold as is”, then the third (or even the fourth) option is probably best.

However, if you intend to do some work on the property immediately after you buy it, you should select the condition the property will be in AFTER that work is completed, and input the expected cost of your rehab into the “purchase costs” line item – more on this later.

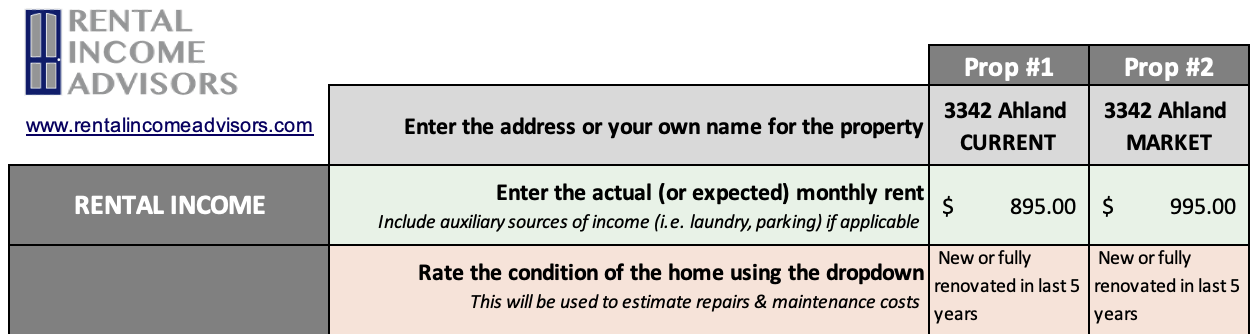

Repairs & Maintenance for my target property

The photos available in the listing show a newly renovated kitchen and bathroom, new vinyl plank flooring throughout, and fresh neutral paint. The exterior looks to be in good shape as well. In short, it looks like a recently renovated, rent-ready property.

I assume these pictures were taken before the current tenant moved in, which appears to be less than a year ago, though it’s possible they’re somewhat older. Still, they look great, so for now I think it’s fair to call this “new or recently renovated”.

So I'll go ahead and enter that into the RIA Property Analyzer, as shown. (Note that for each expense, I’ll enter it in both columns so that I have full financial estimates for both rent scenarios.)

2 Property Taxes

Property taxes are assessed and collected by local government to fund schools and other functions. How much you pay in property taxes can make a meaningful difference to your returns. (Curious which markets tend to have high vs. low property taxes? This post will help.)

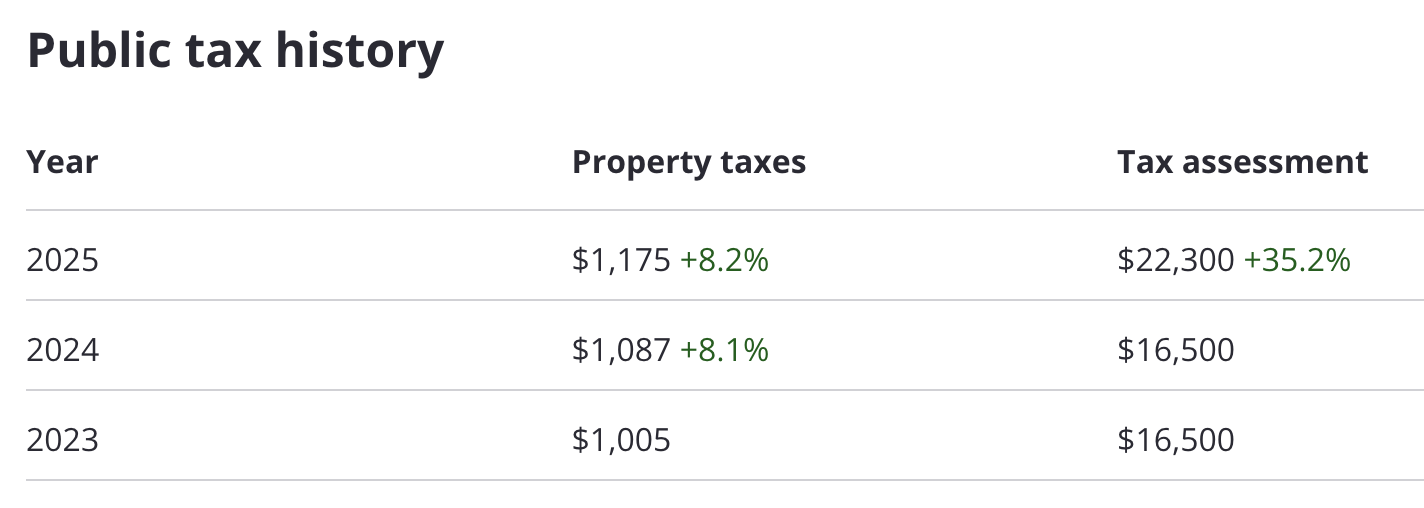

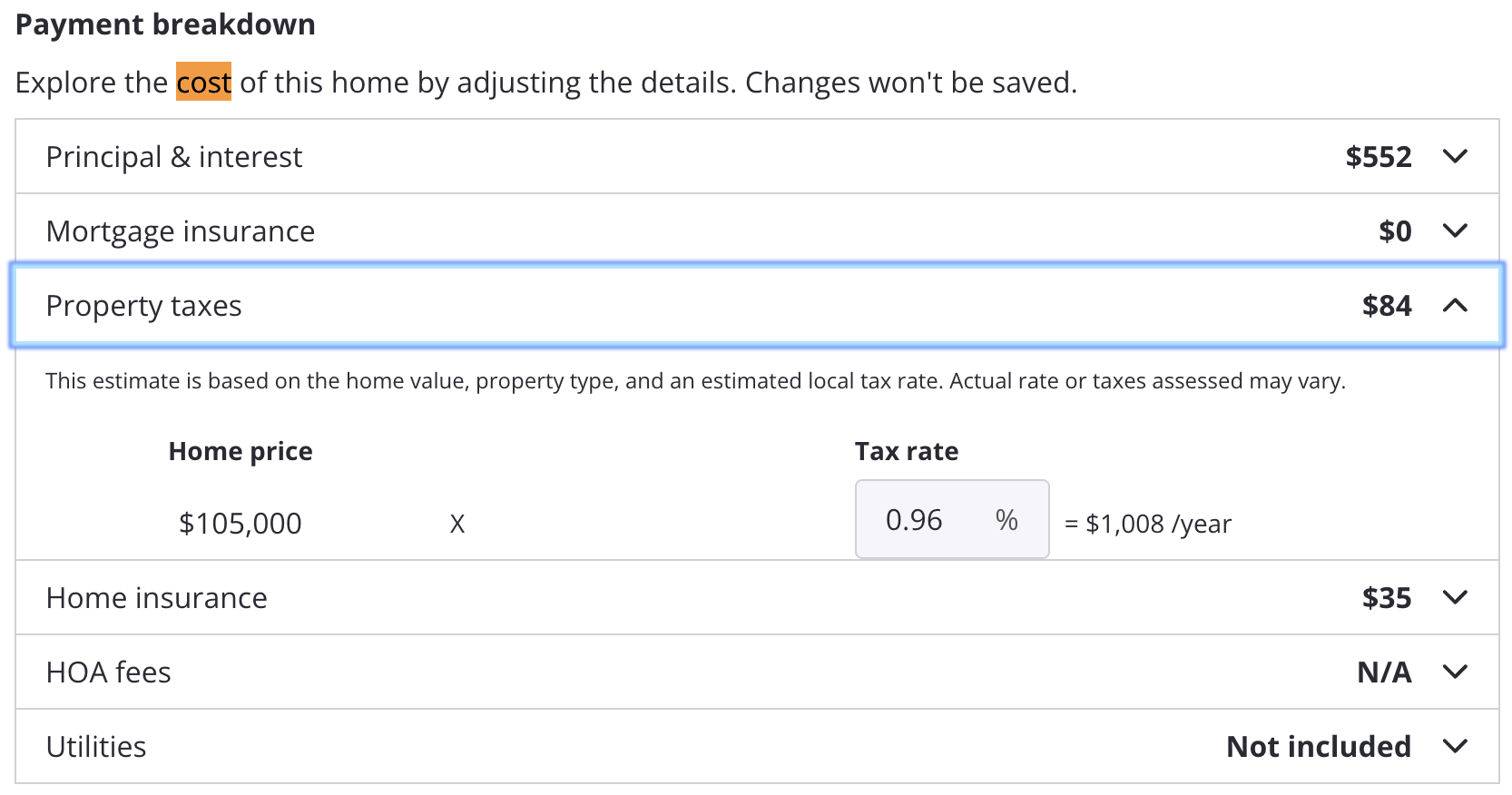

There are a few “quick” ways to estimate your property taxes. For example, there is a property tax history included in the Zillow listing, which is based on public data they’re able to pull in. Zillow also calculates taxes in the “Payment breakdown” section by multiplying the purchase price by the average local tax rates. (There are other online calculators that use the same method of “prevailing local tax rates” to estimate property taxes.)

But as you can see, these varying methods don’t always agree:

What number are you supposed to use — $1,008 or $1,175? If you’re not sure, look up the EXACT property taxes on the websites of the local tax jurisdictions, usually the city and/or county. Just be sure you understand those jurisdictions and how the taxes are billed/collected – in Memphis, for example, there are both city and county taxes and they are collected separately, so it would be easy to look up city taxes and overlook county taxes.

Do your due diligence — property taxes is a big line item, so it’s worth the time to understand exactly what you’ll owe.

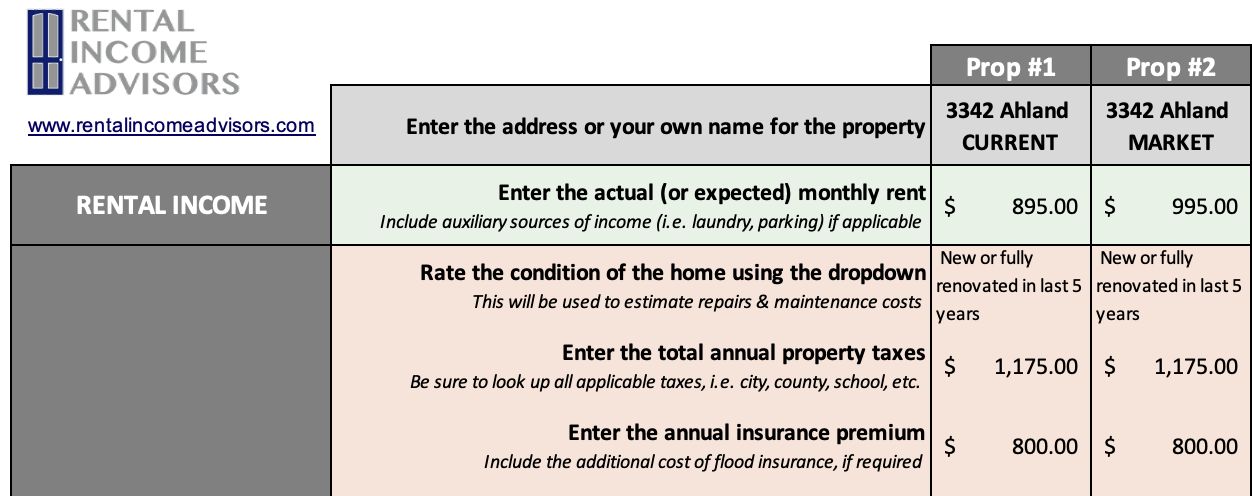

Property Taxes for my target property

In some markets, Zillow successfully shows the true property tax values, but this isn’t true everywhere. In Memphis as of the time of writing, they DO ingest these values correctly, so in our case, the $1,175 value is the right one, and reflects the total property tax burden for the property across both the city of Memphis and Shelby County.

So that’s the figure I plugged into the Analyzer:

3 Insurance

You should always carry insurance on your property – and if you’re getting a mortgage, your lender will require it. (For more on insurance strategies for rental investors, check out this article.)

But how much will it cost? Well, there are two basic ways you can arrive at an estimate:

The BEST Way

Find an insurance provider and request a quote

The FASTER Way

Use an (informed) ballpark estimate

Because insurance rates don’t vary wildly, and it’s not usually an expense that’s going to make or break your investment, this is one instance where it’s probably sufficient to use a ballpark estimate. Zillow provides an estimate in the “Monthly cost” section, but much like the tax info found there, it can be unreliable. (For example, on my target property Zillow suggests $420/year for insurance, which is much too low.)

Insurance rates generally scale with the square footage of the home, and will also depend on the deductible you select. But in typical rental markets, you can get a ballpark estimate from a local expert (PM or other investor), and use this across the board in your financial pro formas. This will be close enough for your modeling, and you can always refine it once you get an actual quote from an insurance provider later in the process.

Insurance for my target property

Because I already carry insurance on my portfolio of properties in Memphis, I can make a somewhat better ballpark estimate. My current insurance premiums range from $700/year to $1,100/year (bigger, more expensive homes cost more to insure.)

Because my target property is a smaller home, I’m confident I can insure it for $800 or less, so that’s the estimate I’ll use in the RIA Property Analyzer, as you can see here.

4 Property Management

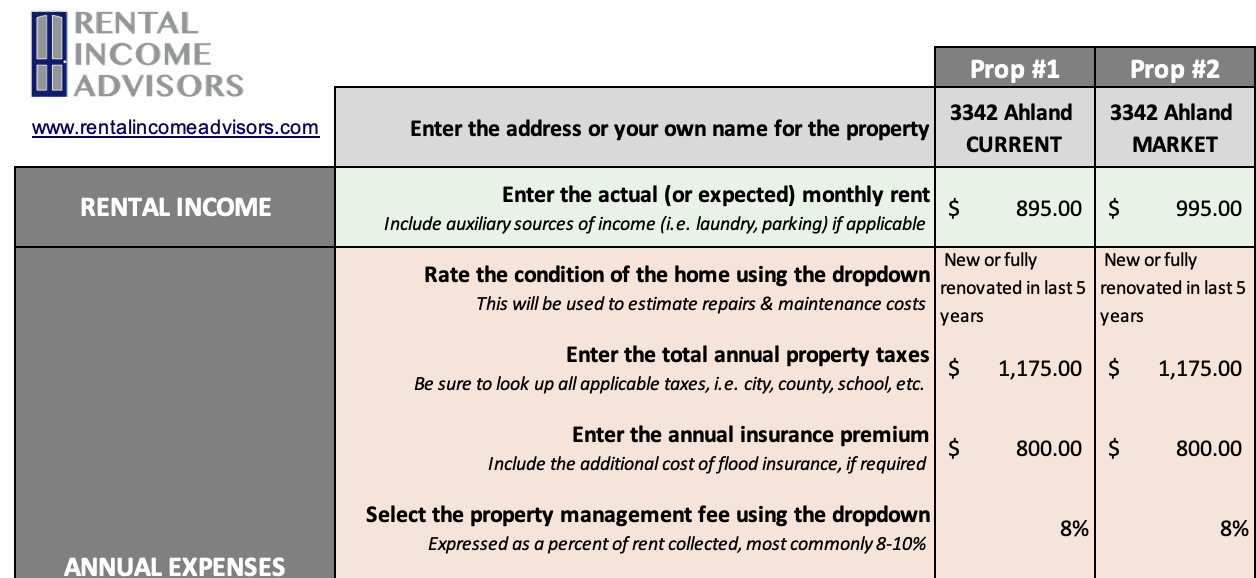

Your property manager’s primary fee will be a percentage of rent collected, typically in the range of 8-10%. If you’re self-managing your property, you can skip this item of course – but given everything a property manager does for you, I always recommend hiring one.

To determine what the property management rates are in your market, you can directly contact a few of them to ask — they may even publish this information on their website. Or if you’re in a hurry, you can just use 10% as a conservative estimate.

My Memphis property manager charges 8%, so I’ve entered that into our trusty Analyzer.

5 Vacancy

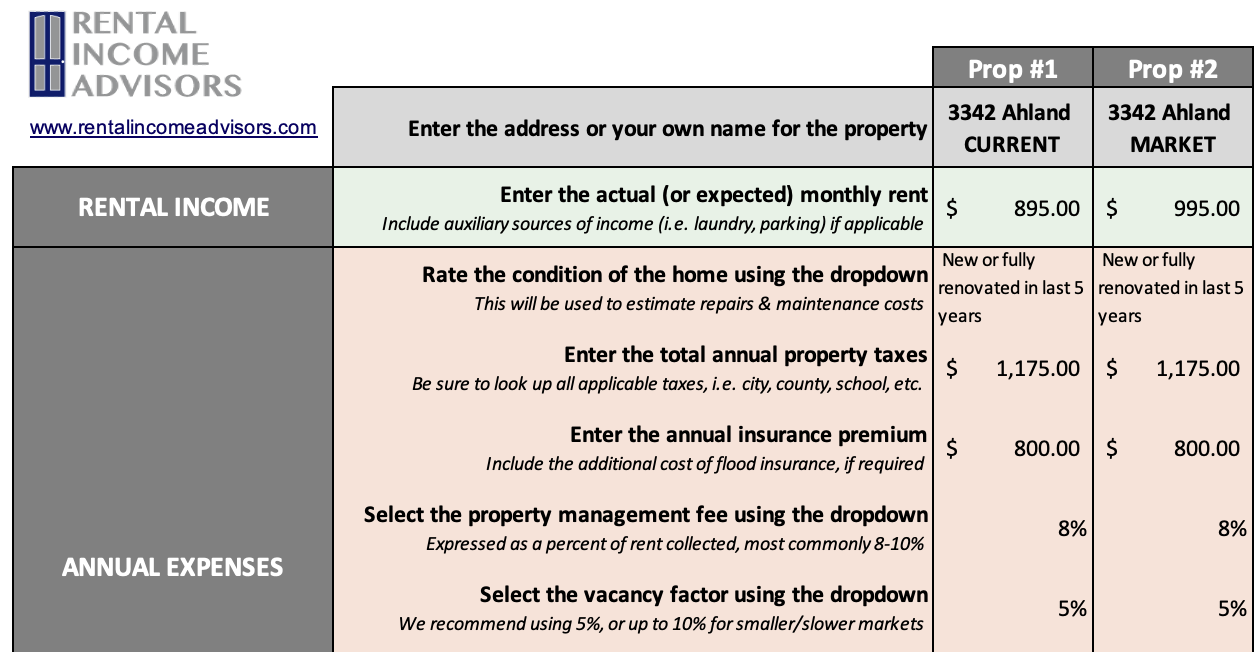

At some point, your property will be vacant for a while in between tenants. During those times you won’t collect rent, so you need to factor this into your projections.

If your property changes tenants every 2 years, and is vacant for a month on each turnover, that’s a 96% occupancy rate (or a 4% vacancy rate). While the vacancy rate in my portfolio has been only 3% over a number of years, I always recommend using 5% vacancy for the purposes of financial modeling — but you can use a higher amount if you want to be even more conservative in your estimates.

Here’s my 5% vacancy entered into the Analyzer – we’re making fast progress now!

6 Utilities

For single-family homes, tenants typically pay all the utility costs. However, if you’re buying a small multi-family (like a duplex, triplex, or quadplex) you may be responsible for some or all utilities. The previous owner should supply records that will allow you to make an estimate of those costs.

The tenant pays utilities at my target property, so I don’t need to account for any costs in the Analyzer.

7 HOA

A monthly Homeowner’s Association (HOA) fee is to be expected with condos and (sometimes) townhouses, but they are quite rare with single family homes unless you’re buying in more upscale neighborhoods.

There is no HOA on my target property, so again I don’t need to enter anything.

8 Other Costs

The RIA Property Analyzer has one more line for expenses, which can be used to capture any other miscellaneous expenses you anticipate. What might those be? Well, as with Utilities, multi-family properties may come with other expenses such as lawn care, snow removal, heating oil, etc. Again, the previous owner should supply full records to you on these costs – and if they apply, enter them here. But none of those costs will apply to my target property, where the tenant is responsible for those items.

The other cost that can be accounted for here is the property manager leasing and renewal fees. Most PM’s will charge a leasing fee for placing a new tenant, usually equivalent to a percentage (50%, 75%, or 100%) of a month’s rent, and a flat renewal fee of a few hundred dollars.

My PM charges 50% of the monthly rent to place a new tenant, and a $250 renewal fee. For my target property, then, I’ll budget one leasing fee every 3 years, plus renewal fees in the other years, and take an average of those three numbers. I’ve entered those numbers into the RIA Property Analyzer, based on the two different rent scenarios I’m modeling.

This completes the Annual Expenses section, woohoo!

But wait…what about CapEx?

CapEx, or capital expenditures, refers to the larger expenses associated with the replacement of a home’s major systems, such as the roof, HVAC, flooring, or appliances. Some investors will budget CapEx into their monthly numbers, so they can “save up” for when those large expenses occur. But there’s a problem with this: capital expenditures are not true expenses.

Instead, they are better understood as a change in the cost basis of the home, as well as (presumably) its current value. In that way, CapEx actually impacts the appreciation that you’ll ultimately realize on the property, not the monthly “profit” — and for that reason, I don’t include it in my calculation of Cap Rate or monthly cash flow. Some investors would handle this differently, but the IRS is on my side: CapEx IS treated differently for tax purposes, and can’t be fully deducted as an expense in the year it occurs — it has to be depreciated over time. Further, CapEx DOES increase the cost basis of the home, which reduces your future capital gains taxes if and when you sell the property.

That said, you should always maintain enough funds in the bank to cover an emergency capital expenditure — it may not technically be a true expense, but you still need actual cash to pay for it!

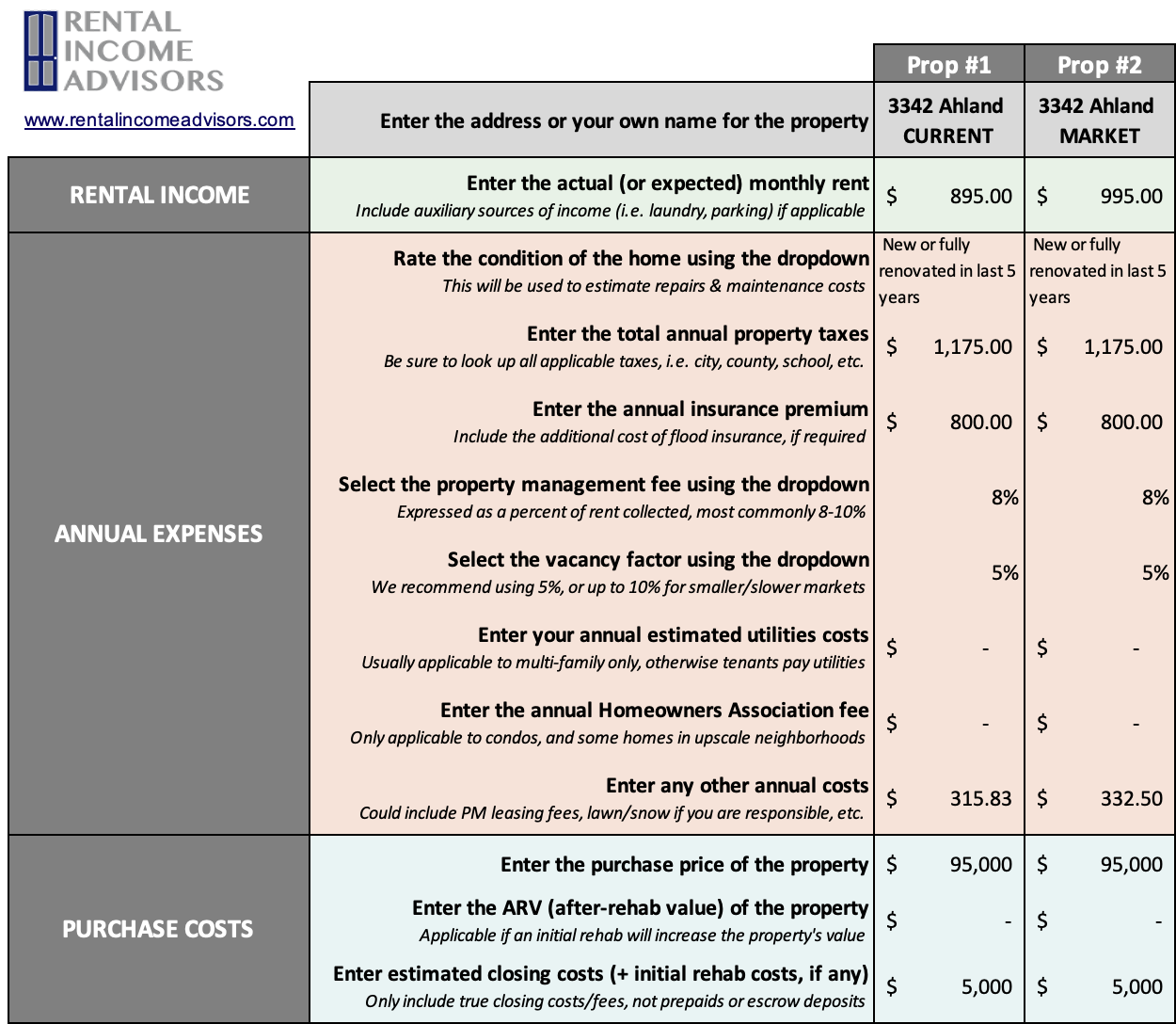

9 Purchase Costs

For all the calculations to work properly in the Analyzer, you’ll need to enter the purchase price of the property, plus closing costs and rehab costs (if any).

For the purchase price of a target property, I always start with the asking price to be conservative — though a comparative analysis of recent sales might point to a lower valuation, and that can be important as you consider an offer. If I can ultimately get the property for less, then that’s icing on the cake. This property is asking $105,000, but it has been listed a while without much interest, and comps points lower, so my assumption will be I can get it below the current asking price: $95,000.

Closing costs are typically 1-2% of the purchase price for cash purchases, and up to 5% if you’re getting a mortgage. Your lender can provide you a good faith estimate on your closing costs, but at this stage you can just use a ballpark estimate.

Finally, if you plan to do any immediate rehab work on the property, you should add the cost of that work to your closing costs and enter it here.

I’m going to use ~5% in closing costs on this property, since I’m assuming a mortgage. There won’t be any rehab because the property is already occupied and in good shape.

Here’s what the Analyzer looks like now with those numbers entered:

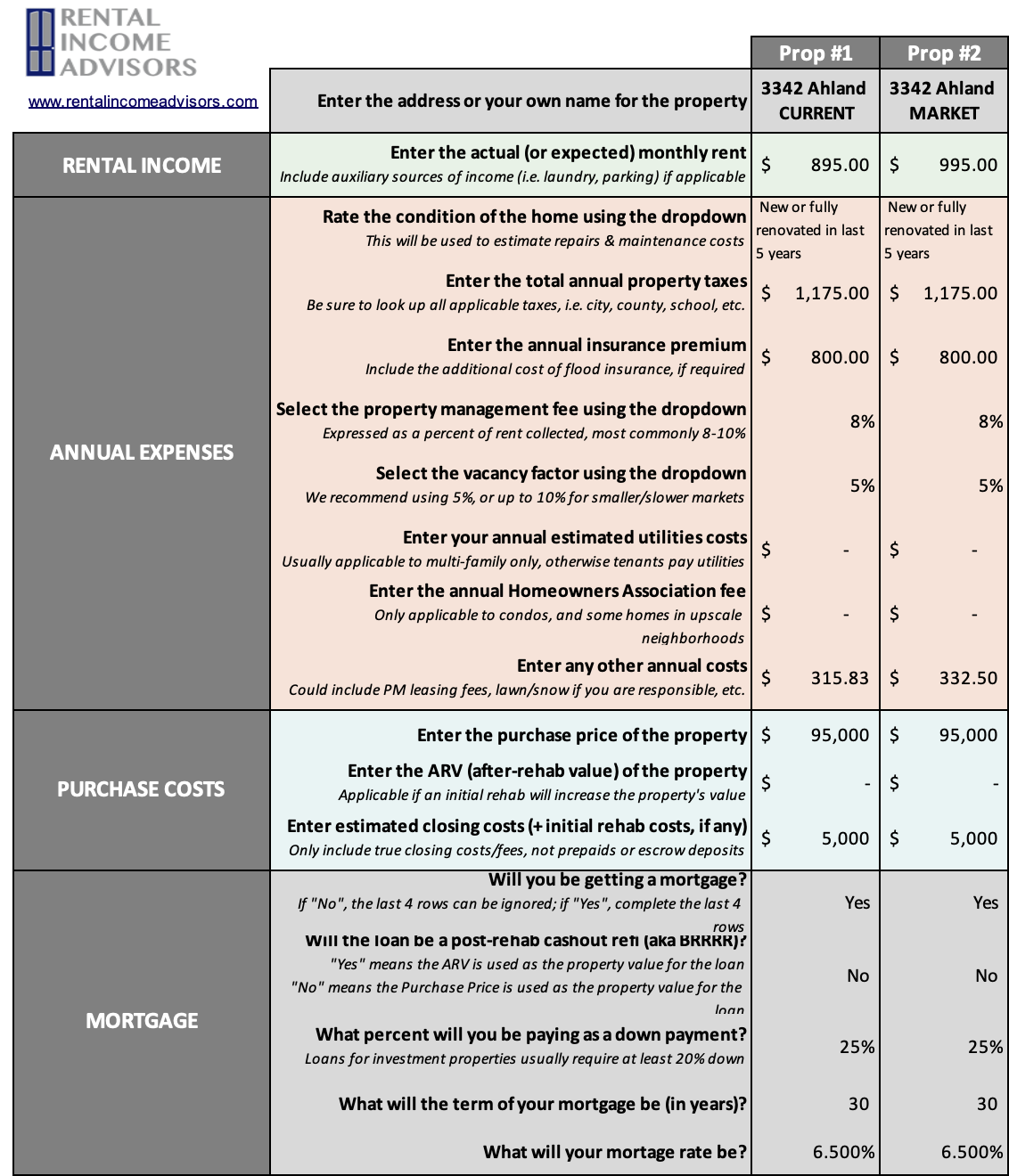

10 Mortgage

Finally, you need to consider your mortgage costs, if applicable. The RIA Property Analyzer has a built-in mortgage calculator, so all you need to enter is the percentage down payment, the term of the mortgage (in years), and the interest rate, and the tool will automatically calculate your monthly principal and interest payments.

For my target property, I’ll assume 25% down for a 30-year fixed rate mortgage, at a rate of 6.5%.

This means that we have now finished entering all our inputs into the Analyzer! Time to move over to the Results tab and find out how this target property measures up.

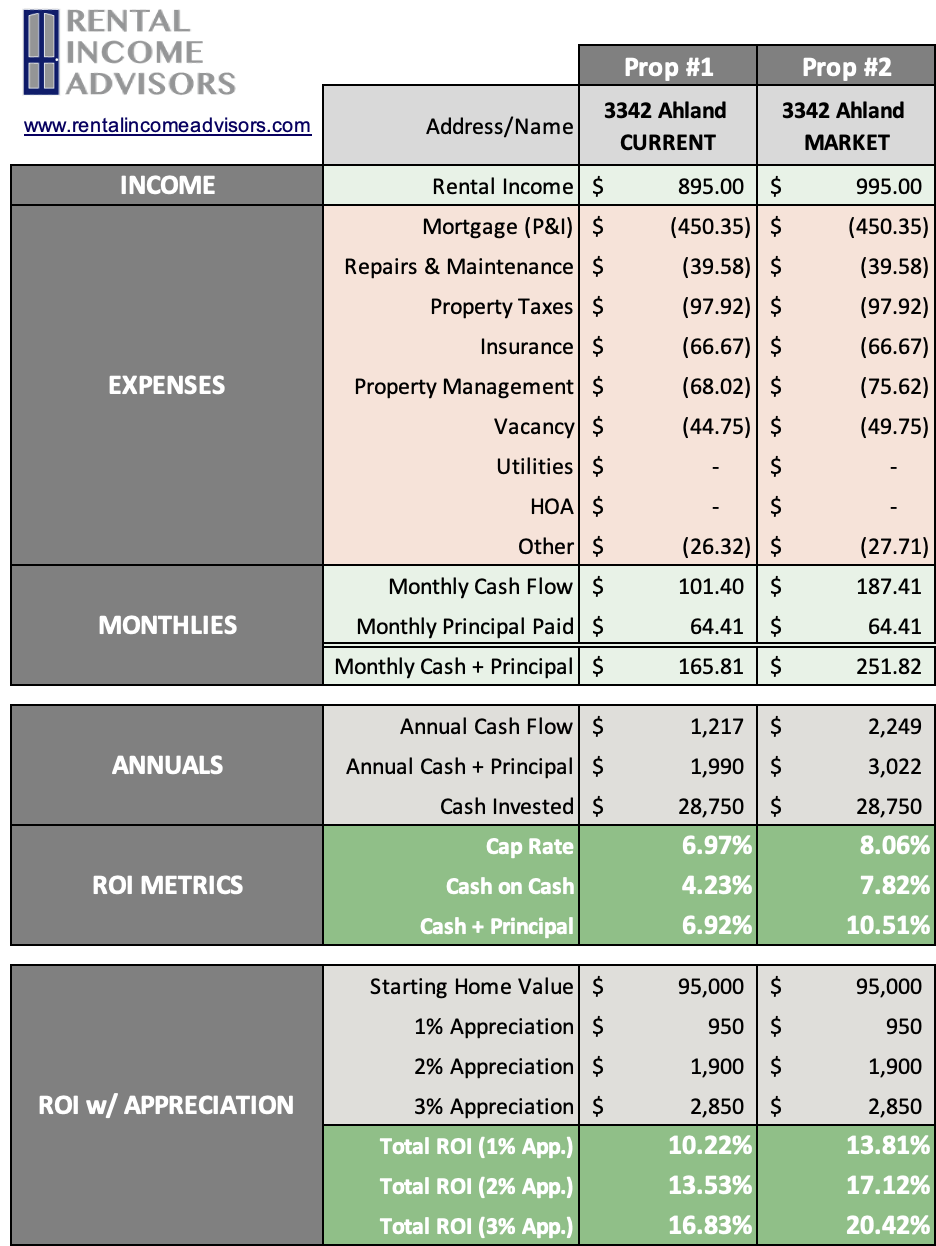

Analyzing the Results

Using the inputs we’ve provided, the tool has calculated all the financial metrics for the property, including monthly cash flow, Cap Rate, and Cash on Cash returns. Here’s a summary of those results assuming the market rent of $995:

Monthly Cash Flow = $187.41

Monthly Principal Paid = $64.41 (this will gradually increase over the life of the loan – bonus!)

Annual Cash Flow = $2,249

Cap Rate = 8.06%

Cash on Cash = 7.87%

Total Return w/ loan paydown = 10.51%

Total ROI with 3% Appreciation = 20.42%

(BTW, if you need to brush up on what these metrics mean and how they’re calculated, this post will help you.)

So, drumroll please…this property has some very solid numbers! At market rent, it meets all of my investing benchmarks for cash flow, cap rate, and cash-on-cash — so if I were looking for properties to acquire, I would feel confident in this one, knowing that my financial assumptions are well-informed and conservative. I would move this tenant toward market rate when they renew their lease, or place a new tenant at market rent if and when the current tenant vacates.

Conclusion

“Running the Numbers” the right way is one of the most important skills in your toolkit as a rental property investor. The single best way to maximize your returns is to compare target properties, project their financial returns accurately, and select the best ones.

Using the RIA Property Analyzer, along with the guidance in these two posts, should help you to do just that! Again, the tool can be downloaded for free here. Happy investing!

About the Author

Hi, I’m Eric! I used cash-flowing rental properties to leave my corporate career at age 39. I started Rental Income Advisors in 2020 to help other people achieve their own goals through real estate investing.

My blog focuses on learning & education for new investors, and I make numerous tools & resources available for free, including my industry-leading Rental Property Analyzer.

I also now serve as a coach to dozens of private clients starting their own journeys investing in rental properties, and have helped my clients buy millions of dollars (and counting) in real estate. To chat with me about coaching, schedule a free initial consultation.