June/July RIA Roundup: The Commercial Crash

Lead Story: The Commercial Crash

If you read any financial news, or watch any CNBC, you might have already heard alarm bells being rung regarding the coming crash of commercial real estate, which could have ripple effects across the broader economy. So what’s all the fuss about — is this just garden variety fear-mongering, or is there actually something to be worried about?

Before we get too deep, let’s answer the question in your mind that you’re afraid to raise your hand and ask: what exactly is commercial real estate? There are six primary sectors that comprise commercial real estate:

Office: office buildings, usually bucketed into A, B, and C class depending on desirability

Retail: malls, strip centers, and other structures that typically house stores, restaurants, and various service providers

Industrial: factories, warehouses, distribution centers, and the like

Multifamily: residential buildings of 5 or more units

Hotel: these are, um….hotels

Special Purpose: everything else, such as self-storage facilities, concert halls and arenas, amusement parks, parking garages, and more.

So why is everyone concerned about commercial real estate? Well, there are two main challenges in play: first, the decline in demand for office space due to the rise in work-from-home, which affects only the office sector; and second, the increase in interest rates on commercial loans, which affects all commercial real estate. Let’s examine each problem in turn.

When the pandemic hit, companies (or at least the kind of companies who lease office space) scrambled to figure out how to run their businesses with workers at home. It turned out it was more feasible than anyone would have guessed, and workers generally liked it much better. Companies saw dollar signs, since they could potentially pay workers less who lived in lower cost of living areas, and they could offload a lot of their office space.

If that sounds like bad news for office real estate, you’re right. The national vacancy rate for office space reached nearly 13% this year, an all-time high.

That 13% compares to a low of 9.5% before the pandemic, which doesn’t seem catastrophic. But the concern is that many companies will continue to downsize when their leases are up for renewal — and those lease renewal cycles can be very long, so office landlords could be facing these headwinds for years to come. This reduced demand will also make it difficult for landlords to increase rents over time.

Does this pose any systemic risk to the broader economy? Probably not. We have a useful recent corollary: the retail sector faced a similar reckoning in the last decade as e-commerce captured an ever-larger share of consumer spending. In response, the value of commercial retail assets fell, but there was no “crash” that most people noticed, and the dust has largely settled: malls closed or re-purposed their space, values have stabilized at a lower level, and the business of retail spins on.

Office is likely to follow a similar path, with the notable exception that — unlike retail — demand is likely to significantly recover for office space. Key swipe data suggests a gradual return of workers to offices, though still far below pre-pandemic levels. Also, many companies are moving aggressively on their “return to office” plans. It turns out that after a few years, companies began to realize that staying remote forever just wasn’t feasible, particularly for mentorship & training, and for high-collaboration projects and teams. (This could be good for apparel retailers, since workers will have to buy real pants again!)

Repurposing office space is another solution that will no doubt play a role as we move forward. Converting office buildings into residential buildings is a tried-and-true practice in places like New York City – in fact, I live in one such building in the downtown Manhattan, which was built as office space in 1930 and converted into condos in 2007. The largest office-to-residential conversion in history, at 1 Wall Street, was recently completed a few blocks away, with an even larger one now underway at 25 Water Street. Office buildings that don’t survive this reckoning may ultimately find their highest and best use as residential buildings.

Let’s examine the second concern in the commercial real estate space, which is higher interest rates. This is a potentially larger issue, since it is not unique to the office sector, and impacts ALL commercial real estate. In my article on financing rental property purchases, I discussed the downsides of commercial loans, namely the lack of fixed rates and/or balloon payments. This means that, unlike homeowners, office landlords can’t just hunker down with their 3% loans; rather, their mortgages either have adjustable rates or need to be restructured periodically, usually every 5 years before balloon payments are due (sometimes call “maturity dates” on commercial loans.)

The trouble, of course, is that their new interest rates will be much higher, and will therefore increase their costs. This could make their businesses much less profitable, in just the same way that higher mortgage rates have reduced the cash-on-cash returns that rental property investors can expect.

But commercial loan-holders have some tools available to them that rental property investors don’t. Lenders are much more likely to negotiate with commercial landlords, and allow things like loan modifications or extensions – remember, the lenders want to avoid default too, especially if the value of the underlying asset has eroded. In many cases, lenders and landlords are able to come to a mutually agreeable compromise on their new lending terms, in order to partially shield the businesses from higher borrowing costs and stay afloat. (In fact, quite a bit of this loan restructuring happened in the retail space in the last decade, as discussed above.)

So what about all these maturing commercial loans – will THEY bring down the broader economy? Most analysts don’t think so, for a few key reasons:

Commercial loans are safer (stricter underwriting standards) than they were before the financial crisis of 2008

Commercial loans aren’t big enough to have broad impacts on the economy

The ability for lenders and landlords to cooperatively engineer solutions to avoid default

So while it’s true that commercial real estate, especially office buildings, are facing significant challenges, the chances that commercial real estate will trigger a 2008-style financial meltdown appear quite remote.

Portfolio Updates

Things have been relatively quiet in my portfolio of late, other than the one tenant current under eviction proceedings (as I discussed in last month’s Roundup). Luckily, I’ll be reimbursed for the lost rent here by my PM, who felt this was an appropriate accommodation given that they had just placed the tenant a few months prior.

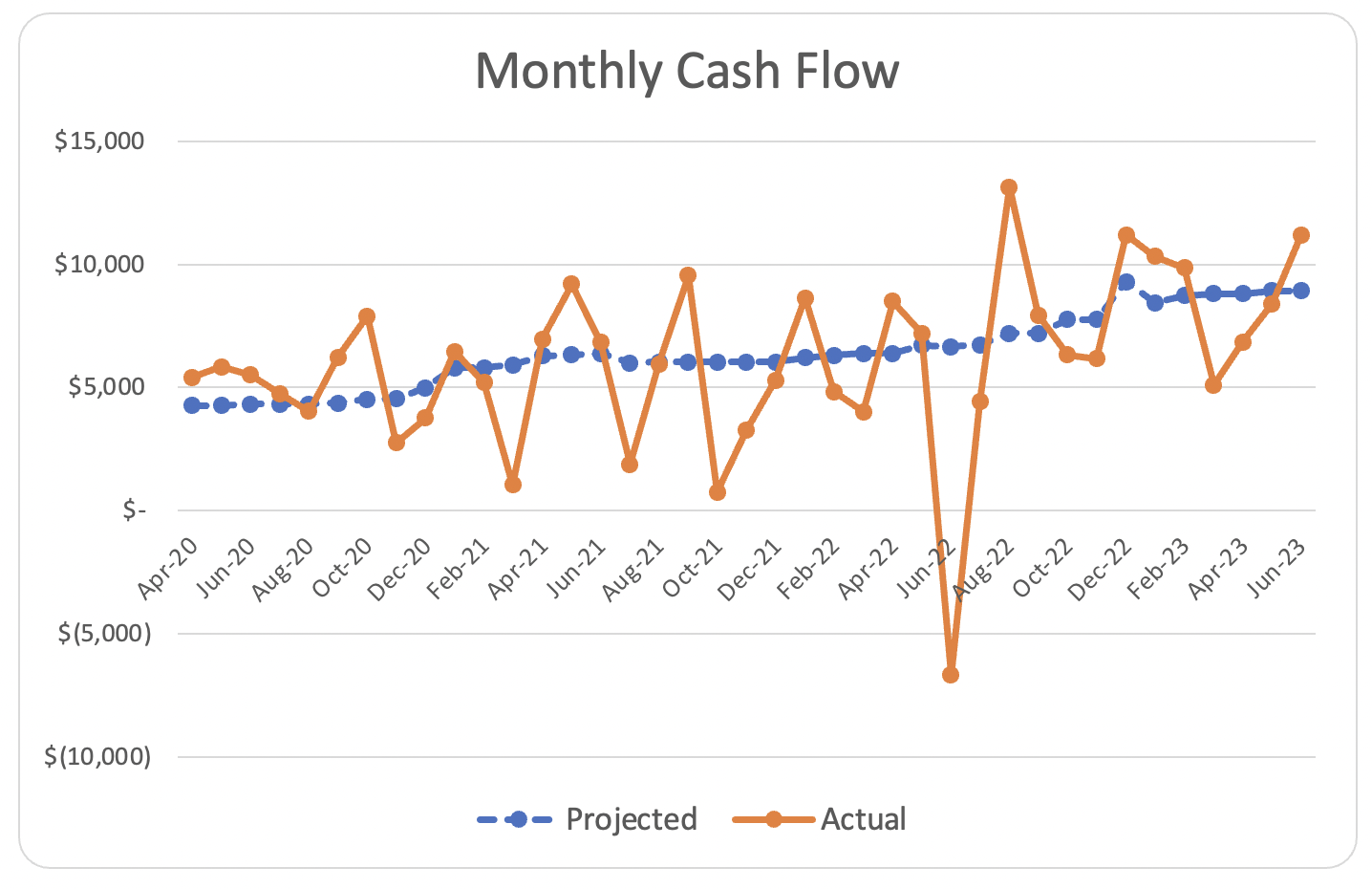

Other than that, the portfolio continues to cruise along. I published the details in the May and June monthly portfolio reports, but the TLDR is that my cash flow for those two months exceeded my pro forma by ~$2,000, and I’m now less than $1K short of my projected cash flow for the year:

In Other News…

Domestic News, Business, & Real Estate

Debt ceiling “crisis” averted. The phony crisis around the debt ceiling was resolved with a last-minute compromise, with both sides claiming victory in the negotiations. (And btw, the $5B in vaccine research funding that I referenced in last month’s Roundup did, in fact, survive.) Perhaps it’s time to consider legislation to abolish the debt ceiling, so that we don’t have to weather yet another future round of economic hostage-taking.

Investors in real estate syndications may be at significant risk. Because of the exposure to commercial real estate discussed above, investors going the “passive route” who invested in syndications may have some big exposure to losses in the next few years. This is one of the reasons I strongly prefer to stay in full control of my properties and investments, rather than handing my money over to someone else.

Inflation continues to drop. The inflation rate continued to cool throughout May and June, and now stands at just 3%. In response, the Fed halted its campaign of interest rate increases — for now.

SEC files suit against two crypto giants. The SEC, seemingly newly emboldened, bared its teeth again recently when it filed suit against Binance and Coinbase, accusing both of selling unregistered securities. Someone explain this to me again — what is cryptocurrency FOR, exactly? (Joking, please do NOT explain it.)

AI may be the next bubble. The crypto bubble has burst, but the investment bubble in AI companies is inflating. Basically you just have to start a company, say you’re doing AI, and start raking in the cash from credulous investors.

Canada is on fire. And I don’t just mean Ryan Gosling in the Barbie movie. (You knew he was hot, but did you know he’s Canadian?!) Rather, the country is literally on fire, and the wildfire smoke has been creating hazardous air quality conditions all over the North American continent for over a month, sometimes stretching as far south as the Mid-Atlantic states.

President Biden’s son to plead guilty. Hunter Biden pleaded guilty to misdemeanor federal tax charges for failing to pay the taxes he owed on time, and reached a deal to resolve an unrelated gun charge.

I-95 bridge reopens ahead of schedule. After a truck fire collapsed a bridge on the critical north-south artery, some said traffic and commerce would be disrupted for months until the bridge could rebuilt. Instead, it reopened in just 12 days, using a creative temporary solution. The permanent bridge will be rebuilt over the next few months, without major disruptions to traffic flow. Maybe we can still build things after all?

DeSantis campaign uses AI images to smear Trump. DeSantis campaign adds used fake images to make it appear that Trump had hugged and kissed Anthony Fauci. This is weird on every possible level, but perhaps weirdest on account of the fact that there are so, so many actually true things that Trump did that the DeSantis campaign could have used to make him look bad.

Kids’ test scores drop. Students in American schools have struggled to keep up, with test scores in reading and math dropping sharply last year. The move to remote learning during the pandemic may have hurt students more than most people thought at the time.

Covid hospitalizations and deaths also drop. CDC tracking indicates that Covid-19 hospitalizations and deaths are at the lowest point since the pandemic began, further reinforcing the ongoing shift to a less virulent endemic phase for the Covid-19 virus.

Supreme Court bans race-conscious college admissions. Undoing over four decades of its own precedent, the high court struck down the right of colleges and universities to consider race as one factor among many in admissions. In places where this move had already been implemented, such as in Michigan, where the practice had been banned in state schools since 2006, Black enrollment fell by nearly half. But California has also banned race-conscious admissions in its state schools for decades, and they still have a very diverse enrollment. They achieve this by focusing on what is perhaps the only dividing line in American bigger than race — wealth. (Scott Galloway makes this point remarkably well in one of his recent essays — I know I keep saying it, but this guy is essential reading.)

Samuel Alito is the latest Supreme Court justice embroiled in an ethics scandal. The justice, like his colleague Clarence Thomas, apparently had no problems accepting private jet travel and lavish free trips from Republican megadonors, and then failing to disclose them. Alito took the highly unusual step of preempting the published report with his own op-ed in the Wall Street Journal, lamely arguing that he was not required to disclose the gift because the private jet trip was equivalent to saying in someone’s guest bedroom (lol), and that the seat would have been empty anyway had he not filled it. Sure sure sure, nothing to see here.

International News, Science & Technology

Russian military in disarray. The Wagner group of mercenaries, who do a good deal of the fighting on behalf of, and alongside, Russian troops, claimed that Russia attacked them, launched a counteroffensive and a march on Moscow, and then abruptly called if off. Then the leader of the Wagner group went to Belarus after apparently negotiating some kind of deal so that Putin wouldn’t assassinate him, but the latest reports are that he has returned to Russia, or perhaps never left in the first place. Only two things are clear in all this: first, the war is not going well for Russia; and two, Putin is 100% gonna assassinate that guy.

Protests in France. Major protests wracked the country for nearly a week in response to the police shooting of a teenager. (See? The French, they’re just like us!)

Apple unveils its VR headset. This technology has been hyped for many years, but has consistently failed to live up to the hype. Apple is hoping to change that with its new headset. Apple always seems to make uncool things cool, so we’ll see if that trend continues next year when its version of “put this giant thing on your face to escape the real world” goes on sale.

Meta debuts Threads. In a direct challenge to Twitter, which is struggling failing under Elon Musk’s uneven disastrous leadership, Meta unveiled Threads. It lacks many of the key features that makes Twitter Twitter, but 30M people signed up in the first day anyway, and it now has over 100M users. Musk and Zuckerberg are yet to have their much-hyped (and totally ridiculous) cage match, but in their respective CEO roles, a clear winner has already emerged.

The world has its hottest day ever. A combination of long-term warming with short-term impacts like El Nino caused the world to have its hottest day on record on July 3rd. But the record didn’t last long — July 4th was even hotter. In all likelihood, the record will be broken several more times later this summer. Obviously, this is…not great.

Four children survive 40 days in the Colombian jungle. In a truly unbelievable survival story, four indigenous children (aged 13, 9, 4, and 1) were stranded in the jungle after a light plane crash. The accident killed their mother, but they survived 40 days on their own before finally being located and rescued by a huge search effort that had been mobilized. Think about how long you would survive in the jungle, especially if you had to care for a 4-year-old and a toddler, and it’s impossible not to gain respect for the skills and knowledge of indigenous peoples.

Arts & Culture, Sports, and All the Rest

Billy Joel to end his residency at Madison Square Garden. The legendary singer/songwriter and New York icon, now 74, will end his historic run of monthly sold-out concerts at his hometown arena.

PGA Tour and LIV Golf merge (maybe). The announced merger aimed to end the acrimonious legal battle between the PGA and the upstart league backed by Saudi oil money — but many questions remain unanswered, and the deal is likely to face strong anti-trust scrutiny from the Justice Department.

US Womens Open held at Pebble Beach. For the first time, a womens professional event is being contested at the iconic West Coast course.

Lionel Messi coming to Miami. The world’s biggest soccer star, fresh off his triumphant performance at the World Cup, will join Major League Soccer in an echo of David Beckham’s move to MLS a few decades ago.

Cormac McCarthy dies. The reclusive author, considered by many to be America’s greatest living novelist, died at age 89. His celebrated canon includes books like “No Country for Old Men” and “All the Pretty Horses”, among many others.

Pat Sajak to leave Wheel of Fortune. In announcing his retirement, the bland, ageless host didn’t say what we all know: that this will give him more time to focus on his true passion, which is posting super weird stuff on social media. He will pass the baton to Ryan Seacrest, equally bland and ageless, who is apparently required to host literally everything.

Final Thoughts: Luck

First, a little housekeeping: this is a combined June/July issue because I’m spending most of those two months traveling — first, a few weeks of fun in Las Vegas in June, and then most of July traveling in Europe with my family. If you’re thinking “nice work if you can get it”, you’d be right. I’ve been very lucky.

Except not recently in poker.

Let me explain. Since I left my W2 job more than 4 years ago, I’ve been able to devote more time to hobbies I enjoy, such as golf, piano playing, travel, and (self-evidently) writing. I’m also a fan of poker, and have spent more time studying the game in the last few years than ever before, trying to improve my play and results.

On the Vegas trip I mentioned, I played a few events in the World Series of Poker (WSOP). The “Main Event” at this series was one of the first to be broadcast on TV a few decades ago; this is how many people became familiar with the game, and it’s what started the so-called “poker boom” that continues to this day. The WSOP is an amazing spectacle, with tens of thousands of poker enthusiasts descending on Las Vegas from all over the world over the course of six weeks each summer.

Poker is a game that is both fascinating and maddening. It involves math, probability, and psychology (yours and your opponents’); it requires social awareness, discipline, patience, and courage. But it also involves a significant amount of luck. In most competitive arenas (think tennis, gymnastics, chess, Rubik’s cube solving, etc.) the best players win almost all the time, and nobody else stands much of a chance. In poker, though, the best players lose all the time. They have an edge in the long run, but on any given day, chance plays a huge role, and anybody can win. This is one of the reasons poker is such an enticing game: everyone can chase the dream of a big tournament victory, whether you’re a poker pro or just a casual fan who plays few events each year.

But this same dynamic is what makes it maddening for good players: even doing everything right, you will lose most of the time. Likewise, improving your play does not guarantee an improvement in your short-term results. You can play better and perform worse, and that state of affairs can persist for a surprisingly long time due to the significant role luck plays in any individual tournament.

The WSOP draws a diverse crowd from dozens of countries, young and old, men and women, pros and recs. But listening to the conversations at the tables and around the WSOP, there are two things nearly every poker player agrees on:

They are unusually unlucky. Ask a hundred poker players to place themselves on a scale from least lucky at poker to most lucky at poker, and I’d be shocked if even a single one rated themselves luckier-than-average.

Their wins are due to skill, but bad luck is to blame when they lose. When poker players have success, they tend to focus on the things they did well, and gloss over the moments of good luck they had along the way. But they never forget the moments of bad luck, and can’t wait to tell you all about them.

This doesn’t tell us much about the nature of luck, but it tells us a lot about how we PERCEIVE luck – and I don’t just mean in poker. We all have strong “bad luck bias”: moments of bad luck feel terribly unjust, so they leave an indelible mark and we remember them vividly; meanwhile, we tend to quickly forget moments of good luck – or, more insidiously, we fail to recognize them as good luck at all, and instead chalk them up to our virtue, merit, or skill. (In social science circles, this is known as self-attribution bias – but “bad luck bias” is a bit punchier, isn’t it?)

The hard truth is that luck matters more than most of us are comfortable admitting. Math suggests strongly that luck plays a huge rule in achieving outsize success in business or investing; most of the business titans whose names we know were probably just lucky. When it comes to investing, the period of years over which you invest (which is largely based on the year you were born) is much more important to your results than your skill in stock-picking or your investment strategy. Research has also consistently shown that the vast majority of managed funds and hedge funds fail to perform better than the overall market, and the small percentage of managers who do beat the market consistently over a period of 5 or 10 years can be explained by luck alone.

Outside of investing, most people significantly underestimate the importance of luck (especially good luck) in their lives. Our tendency to ascribe good luck to our merit – to believe we earned it, deserved it, or caused it – is a common human bias, but it’s also wrapped up in the very mythology of our country, baked into ideas like the “self-made man” and the American Dream. But luck and the circumstances of your birth determine quite a lot about the most important aspects about your life:

Income and wealth

Health and aging

Educational attainment

Success in relationships

Avoiding accidents and tragedy

For example, the specific neighborhood in which you’re born makes a remarkable difference all by itself. Studies repeatedly show that zip code is a significant predictor of economic success, as well as of health. It’s hard to square these facts with the gospel of the American Dream, which preaches that any of us can lift ourselves up and remake our circumstances if we only have the pluck, skill, and determination to do so. When we look closely, though, the data tell a consistent story: this just isn’t how the world works.

It's not how poker works either. As any poker player will tell you, it’s simply impossible to overcome bad luck in the short term, no matter how well you play.

Personal example: after several years of moderate success and profitability, I have played in 21 tournaments in 2023 and cashed zero times. (In a poker tournament, ~15% of the field “cashes”, or earns a payout in excess of the tournament buy-in; the other 85% makes nothing, and loses their buy-in.) In the several years prior, I cashed in ~30% of tournaments, so there’s no doubt this is a notable stretch of back luck — or “run bad” to use the common poker parlance.

After failing 21 consecutive times at something, it’s easy to cast yourself in the role of Sisyphus, trying again and again in an effort predestined to be futile, or even Job, being mercilessly tested by the angry poker gods. But deep down, I know this is just a form of “bad luck bias” warping my perception of reality: even if you play well, you should expect to fail frequently, and have very bad stretches of results, in a game where luck is so important to the outcome.

And that’s where this conversation dovetails with rental property investing, where luck also plays a significant role, at least in the short term. Just like poker, there can be “high variance” with rental properties, and even with the right strategy and the most thorough due diligence, not all of this is controllable. You can do everything right, and still get hit by bad luck with a storm, a fire, a tree falling on the roof, a tenant issue, and eviction, or any number of other things.

The best way to conquer this variance, as I frequently tell my coaching clients, is to “take more swings”, by purchasing more properties, and by holding them for a long time. This makes it more likely that you’ll achieve your financial targets in the long run, because large data sets tend to revert to the mean, diluting short-term swings in either direction. After coaching over 50 clients on buying rental properties, I’ve found that one of the biggest risks to new investors is a sort of “bad luck bias” in reverse, whereby they have troubles right out of the gates, and rather than simply ascribing this to bad luck, conclude incorrectly that they did something wrong — or even worse, that the investing model itself doesn’t work.

Following my own advice, I’ll be taking more swings at poker tournaments in the future as well. My luck has to change eventually. (Right?)

But the larger point is that I’ve already been extraordinarily lucky. You simply can’t be a healthy, happily married, financially independent 43-year-old financial blogger without having gotten very lucky in a hundred different ways.

And chances are, if you’re reading this, you’re also luckier than you think.

Happy investing,

Eric

About the Author

Hi, I’m Eric! I used cash-flowing rental properties to leave my corporate career at age 39. I started Rental Income Advisors in 2020 to help other people achieve their own goals through real estate investing.

My blog focuses on learning & education for new investors, and I make numerous tools & resources available for free, including my industry-leading Rental Property Analyzer.

I also now serve as a coach to dozens of private clients starting their own journeys investing in rental properties, and have helped my clients buy millions of dollars (and counting) in real estate. To chat with me about coaching, schedule a free initial consultation.

Free Rental Property Analyzer

You probably know that a well-designed rental property calculator is the most important tool a real estate investor has. It allows you to quickly calculate key metrics and understand your cash returns on a target property. You can also answer questions like:

How much do your cash-on-cash returns improve if you use a mortgage vs. paying in cash?

What will your average monthly cash flow be?

How will your returns change in future years?

Those questions can be easily answered with side-by-side comparisons in the RIA Property Analyzer. I guarantee this is the best free rental property calculator out there today, and many of my readers have told me the same. It’s both powerful and very simple and intuitive to use. Check it out!